In our previous article we covered what a Merchant Category Code is and why yours matters more than most merchants realize. This time we are going deeper on one of the most consequential connections in payments: how your MCC directly shapes the chargeback monitoring program you are subject to — and what that means when your ratios start climbing.

A Quick Recap: What Monitoring Programs Are

Visa and Mastercard do not just process payments — they actively monitor the merchants and acquirers on their networks for fraud and dispute activity. When a merchant's chargeback or fraud ratio exceeds certain thresholds, they are flagged, placed into a formal monitoring program, and — if the problem persists — fined or ultimately terminated.

These programs exist to protect the integrity of the card network. From the schemes' perspective, a merchant with consistently high chargebacks or fraud is a problem for everyone: cardholders lose trust, banks absorb costs, and the network's reputation takes a hit. The monitoring programs are the mechanism for keeping that in check.

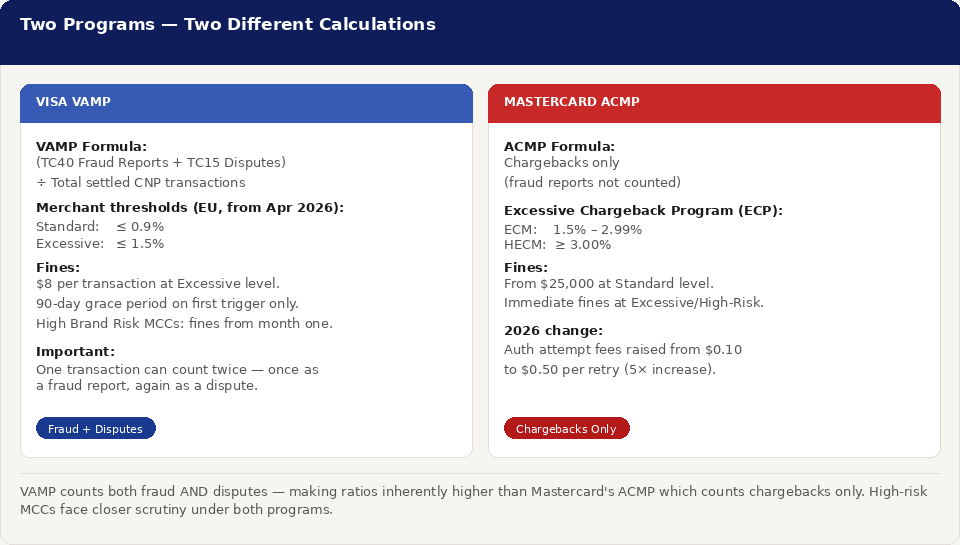

There are two programs you need to understand: Visa's VAMP (Visa Acquirer Monitoring Program), which launched in April 2025 and consolidated two older programs into one, and Mastercard's ACMP (Acquirer Chargeback Monitoring Program). They work differently, they measure different things, and — crucially — they treat different MCCs very differently.

The most important technical difference: VAMP counts both fraud transactions (TC40) and disputes (TC15), then divides by total settled card-not-present transactions. Mastercard's ACMP counts chargebacks only. This means VAMP ratios are inherently higher and harder to manage — especially for merchants dealing with friendly fraud. A single transaction can also count twice under VAMP: once when reported as fraud, and again when escalated to a formal dispute.

Why Your MCC Determines Which Rules Apply to You

Not all merchants are treated equally under these programs — and your MCC is the primary variable that determines where you stand.

Visa maintains a list of what it calls High Brand Risk MCCs — categories that carry elevated regulatory, reputational, or fraud risk. Merchants assigned these codes are subject to stricter treatment under monitoring programs from day one. There is no advisory period, no grace period before fines begin, and a lower threshold for what triggers formal action.

The categories that fall into High Brand Risk include iGaming and gambling (MCC 7995, 7801), adult entertainment (5967, 7273), nutraceuticals and CBD (5122, 5912 in some contexts), online travel agencies (4722), and certain financial services categories (6141, 6153). If you are operating in any of these verticals, you are playing by a different set of rules than a standard retailer — even before you have done anything wrong.

As of April 1, 2026, Visa tightened its thresholds significantly. The Excessive merchant threshold dropped from 2.2% to 1.5% — a 32% reduction in acceptable dispute volume, applying to merchants in the US, Canada, EU, and Asia-Pacific. A merchant running at a 1.8% ratio, comfortably within limits the day before, was now in breach without any change in their actual behavior. If you have not reviewed your ratio since April, now is the time.

For acquirers, the thresholds are tighter still: Above Standard sits at 0.5% and Excessive at 0.7%. Your acquirer is therefore watching their own portfolio ratio extremely closely — because exceeding it triggers fines across their entire book. That shared pressure is part of why acquirers are increasingly proactive about flagging merchant ratio creep before it becomes a formal breach.

The Escalation Path — And How Fast It Moves

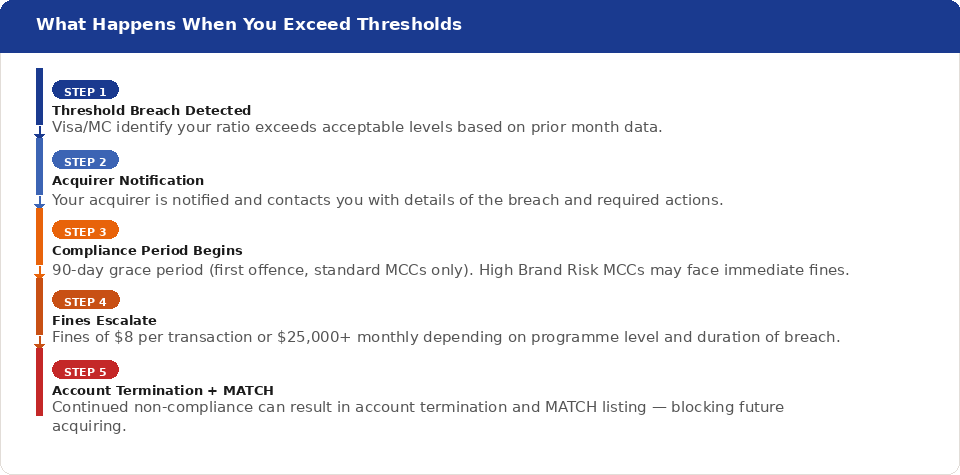

One of the most common misconceptions merchants have is that there is plenty of time to respond once they are flagged. In practice, the escalation can move faster than expected — particularly for high-risk MCCs.

For standard MCCs, VAMP provides a 90-day grace period on first trigger — but only if you have no VAMP exceedance in the previous 12 months. After that first grace period, repeat violations face immediate fines of $8 per transaction. For High Brand Risk MCCs, fines can begin in month one with no warning tier.

At the Mastercard level, the ECP program operates on two tiers. At ECM level (1.5%–2.99% chargeback ratio), fines of $25,000 or more may be applied after four months. At HECM level (3.0%+), the clock starts faster and fines scale accordingly. In 2026, Mastercard also raised its excessive authorization attempt fees from $0.10 to $0.50 per retry — a fivefold increase targeting card-testing fraud that disproportionately affects high-risk merchants.

The worst outcome is not the fines — it is MATCH listing. If your account is terminated for chargeback or fraud program violations, you may be placed on the Mastercard Alert to Control High-Risk Merchants list. This makes it significantly harder — sometimes near impossible — to open a new merchant account anywhere in the network. Avoiding MATCH is one of the strongest reasons to address ratio problems early.

5 Things to Do Right Now

The good news is that there are concrete steps you can take — both to understand your current exposure and to reduce your ratio before it becomes a problem. Some of these also directly affect how VAMP calculates your ratio, since certain dispute types are explicitly excluded from the calculation.

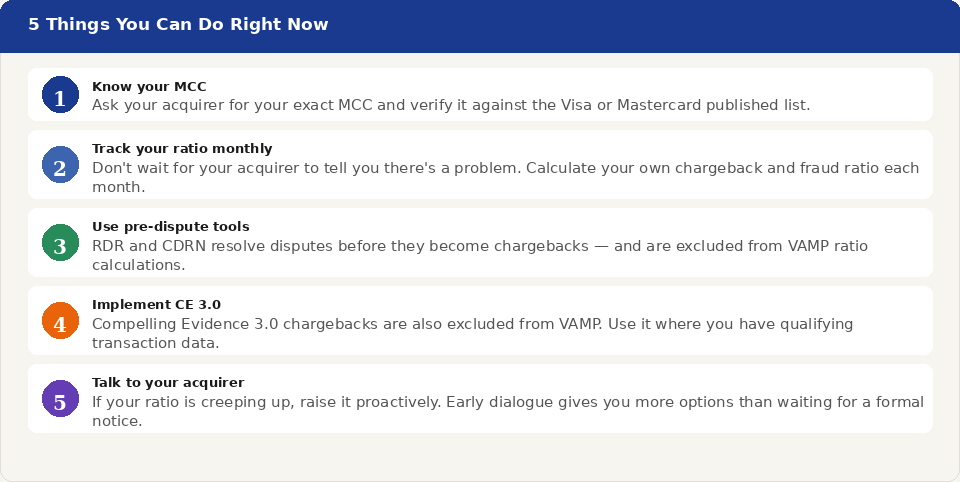

1. Know your MCC — and verify it. Ask your acquirer for your exact MCC and cross-reference it against the published Visa and Mastercard lists. If you are in a High Brand Risk category, make sure you understand exactly which rules apply to you. If your MCC seems wrong for your business, raise it immediately — misclassification in either direction has consequences.

2. Track your ratio yourself, every month. Do not wait for your acquirer to tell you there is a problem. Calculate your own VAMP ratio monthly: total TC40 fraud reports plus TC15 disputes, divided by total settled card-not-present transactions. If your ratio is trending upward, you want to know before it crosses a threshold — not after. Your acquirer's internal limits are likely stricter than Visa's, so build in a buffer.

3. Use pre-dispute tools — they are excluded from VAMP. Disputes resolved using Rapid Dispute Resolution (RDR) and Cardholder Dispute Resolution Network (CDRN) are excluded from VAMP ratio calculations. Using these tools can materially reduce the ratio Visa sees, even if the underlying dispute volume does not change. If you are not using pre-dispute tools, this is worth investigating as a priority.

4. Implement Compelling Evidence 3.0 where you can. CE 3.0 is the only compliant mechanism to remove TC40 fraud reports from the VAMP numerator after the fact. When a CE 3.0 representment succeeds, the chargeback is excluded from VAMP calculations, you keep the revenue, avoid the refund, and sidestep the $8 enforcement fee on that transaction. If you have qualifying prior transaction history, this is one of the most effective tools available.

5. Talk to your acquirer before they come to you. If your ratio is creeping toward a threshold, raise it proactively. Acquirers have far more flexibility — and far more willingness to work with you — when you surface a problem before a formal monitoring program flag. Waiting until you are enrolled in a program significantly narrows your options and can accelerate the timeline to fines.

The Bottom Line

Your MCC is not just an administrative code. It is the variable that determines which monitoring program rules apply to you, how quickly fines can begin, and how much room you have to maneuver when ratios spike. For merchants in high-risk categories — iGaming, adult, travel, nutraceuticals, online lending — the rules are tighter, the grace periods shorter, and the consequences of inaction more immediate.

Understanding this connection puts you in a fundamentally better position. Know your MCC, monitor your ratio, use the tools that reduce your VAMP exposure, and work with an acquirer who is transparent about where you stand. That is not just good compliance practice — it is the foundation of a stable, sustainable merchant account.

At MMG, we work specifically with high-risk merchants, which means we understand these dynamics in detail. If you are unsure about your current MCC, your ratio exposure, or what your monitoring program status means for your account, we are happy to talk it through.

Get in touch