Most merchants never think about their MCC. That's a mistake. Four digits assigned at onboarding determine your interchange fees, your chargeback monitoring exposure, your reserve requirements, and whether you're classified as high-risk at all — often before you've processed a single transaction.

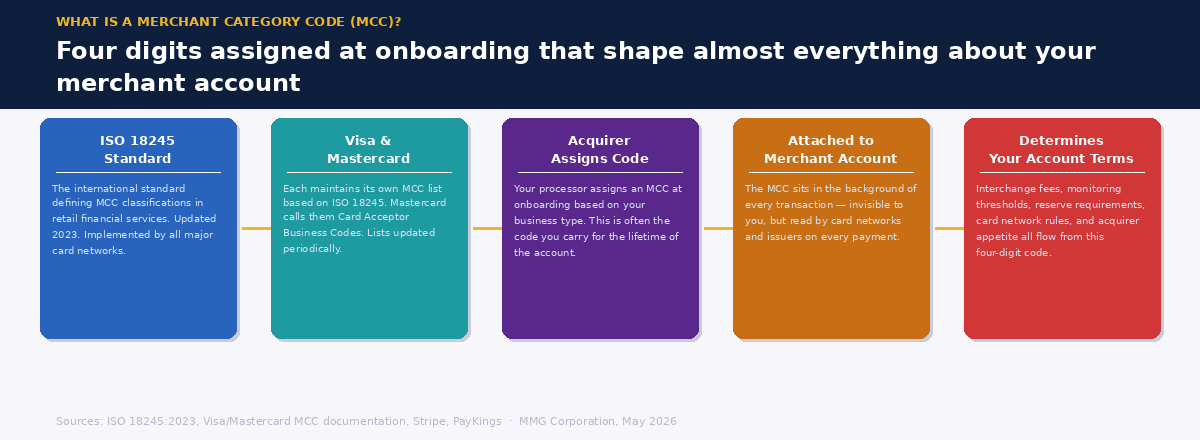

A Merchant Category Code is a four-digit number assigned to every business that accepts card payments. It tells the card networks — Visa, Mastercard, American Express, and Discover — what kind of business you are. That classification then flows through to almost every aspect of how your payments are processed: what you pay in fees, how closely you're monitored for fraud and disputes, what rules apply to your transactions, and how easily you can get and keep a merchant account.

Merchants rarely see their MCC. It sits in the background of the payment infrastructure, assigned at onboarding by the acquirer or payment processor, and largely invisible in day-to-day operations. But it is not neutral — it is one of the most consequential pieces of data attached to a merchant account, and understanding it is the starting point for understanding why certain costs, restrictions, and requirements apply to your business and not to others.

Where MCCs Come From

The MCC system is defined by ISO 18245, the international standard for merchant category codes in retail financial services. Visa and Mastercard each maintain their own implementations of this standard — Mastercard refers to MCCs as Card Acceptor Business Codes — and both update their lists periodically. The codes are not perfectly identical between networks, but the underlying logic is consistent: one code per business type, assigned to reflect the nature of the goods or services provided.

The code itself is assigned by the acquirer or payment processor during the merchant onboarding process. In practice, this means a human being — or an automated system — at your processor makes a judgment call about which four-digit code best describes your business. For most merchants, this is a routine administrative step. For high-risk merchants, it is a decision with significant financial and operational consequences that often goes entirely unexamined.

New MCCs can be applied for through the card networks' formal processes — Visa uses TC68 — but they are generally reserved for merchant categories with at least $10 million in annual revenue, and the process is neither quick nor guaranteed. For most merchants, the code assigned at onboarding is the code they carry.

What Your MCC Actually Determines

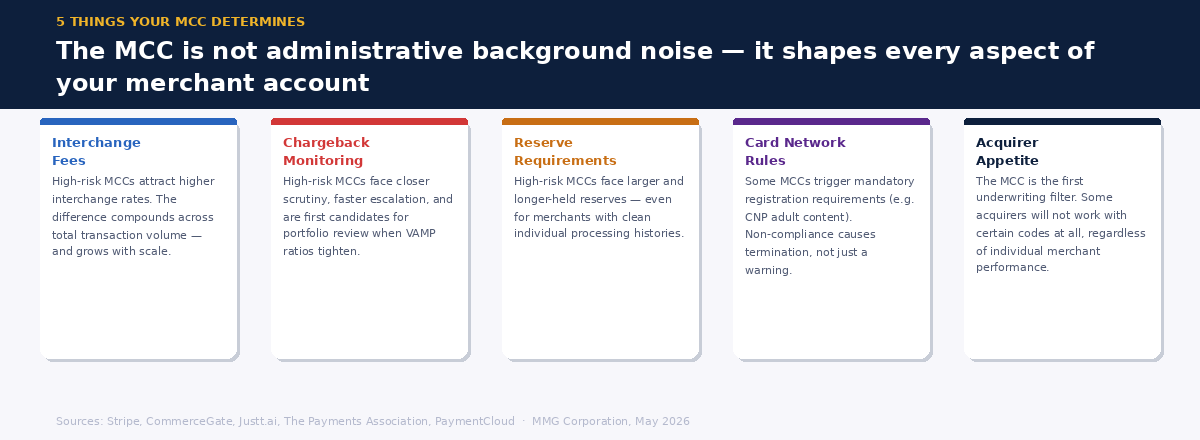

The downstream effects of an MCC are broader than most merchants realize. Five areas are directly affected.

Interchange fees. Every card transaction involves an interchange fee paid to the issuing bank. The rate applied depends on multiple factors — card type, authentication method, transaction channel — but the MCC is a primary determinant of which interchange category the transaction falls into. High-risk MCCs attract higher interchange rates because the networks price in the elevated probability of fraud and disputes. The difference between a standard and a high-risk interchange rate can be significant across a merchant's total transaction volume, and it compounds with scale.

Chargeback monitoring thresholds and escalation. Visa and Mastercard apply different monitoring frameworks to different merchant categories. A high-risk MCC means closer scrutiny, faster escalation when thresholds are approached, and in some cases a lower effective threshold before enforcement action begins. Under VAMP, the acquirer's portfolio-level ratio is what drives direct financial consequences — but the MCC shapes how the acquirer thinks about and manages individual merchants within that portfolio. High-risk MCC merchants are the first candidates for review when ratios tighten.

Reserve requirements. The rolling reserve a merchant is required to maintain — its size, duration, and structure — is shaped significantly by the MCC. High-risk MCCs face larger and longer-held reserves as standard. A merchant with a clean processing history who is assigned to a high-risk MCC category will typically face higher reserve requirements than an equivalent merchant in a standard MCC category, regardless of their individual performance record.

Card network rules and registration requirements. Some MCC categories trigger mandatory registration requirements with the card networks — for example, adult content merchants may be required to register separately with Visa before processing card-not-present transactions. Merchants who are not aware of these requirements, or whose processor has not ensured compliance, can face processing termination for non-compliance with rules they did not know applied to them.

Acquirer appetite and account availability. Some acquirers will not work with certain MCCs at all. Others will work with them under specific conditions. The MCC is the first filter in any acquirer's underwriting process — before they assess your chargeback history, your processing volumes, or your compliance posture, they look at your MCC and determine whether you fall within their acceptable merchant categories. For high-risk MCCs, this filter significantly narrows the field of available acquiring relationships.

High-Risk MCCs: Which Categories and Why

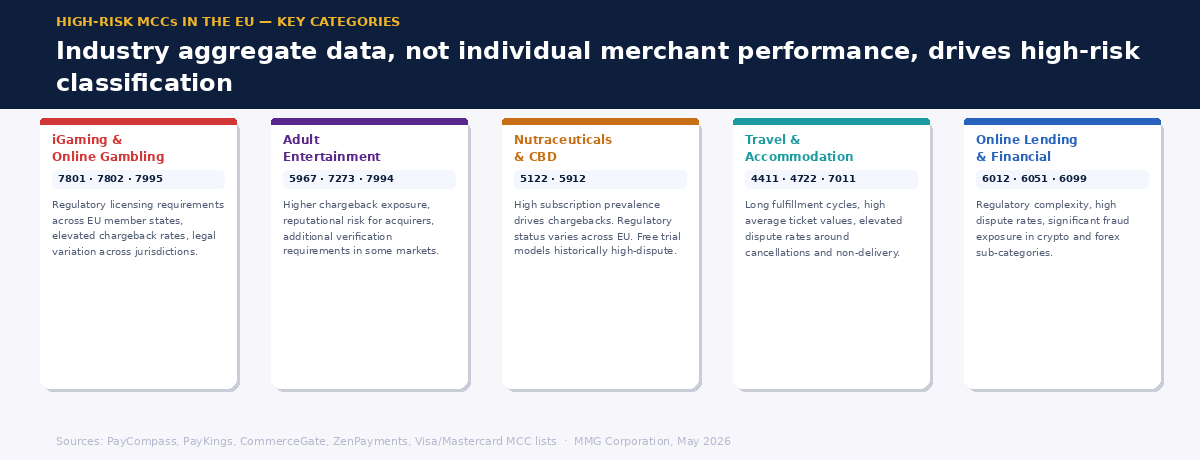

High-risk MCCs are not arbitrary — they reflect industries where aggregate data shows elevated chargeback rates, higher fraud exposure, regulatory complexity, or some combination of all three. The card networks use this aggregate industry data to set baseline expectations, which are then applied to individual merchants within those categories regardless of their individual track record.

The categories most commonly classified as high-risk across EU payment processing include:

iGaming and online gambling (MCCs 7801, 7802, 7995) — Subject to regulatory licensing requirements across EU member states, elevated chargeback rates from losing bettors, and significant variation in legality across jurisdictions.

Adult entertainment (MCCs 5967, 7273, 7994) — Higher chargeback rates, reputational risk for acquirers, and in some markets, additional verification requirements around age confirmation and consent.

Nutraceuticals, supplements, and CBD (MCCs 5122, 5912) — High subscription model prevalence drives chargeback exposure; regulatory status of products varies across EU markets; free trial models historically generated elevated dispute rates.

Travel and accommodation (MCCs 4411, 4722, 7011) — Long fulfillment cycles between booking and service delivery, high average transaction values, and elevated dispute rates around cancellations and non-delivery claims.

Online lending and financial services (MCCs 6012, 6051, 6099) — Regulatory complexity, high dispute rates, and in some sub-categories, significant fraud exposure.

Being classified in one of these MCC categories does not mean a merchant cannot process payments or build a stable acquirer relationship. It means the baseline expectations are higher, the field of potential acquirers is narrower, and the operational management required is more rigorous. That is manageable — with the right acquirer and the right setup.

Misclassification: A Risk Most Merchants Don't Know to Check For

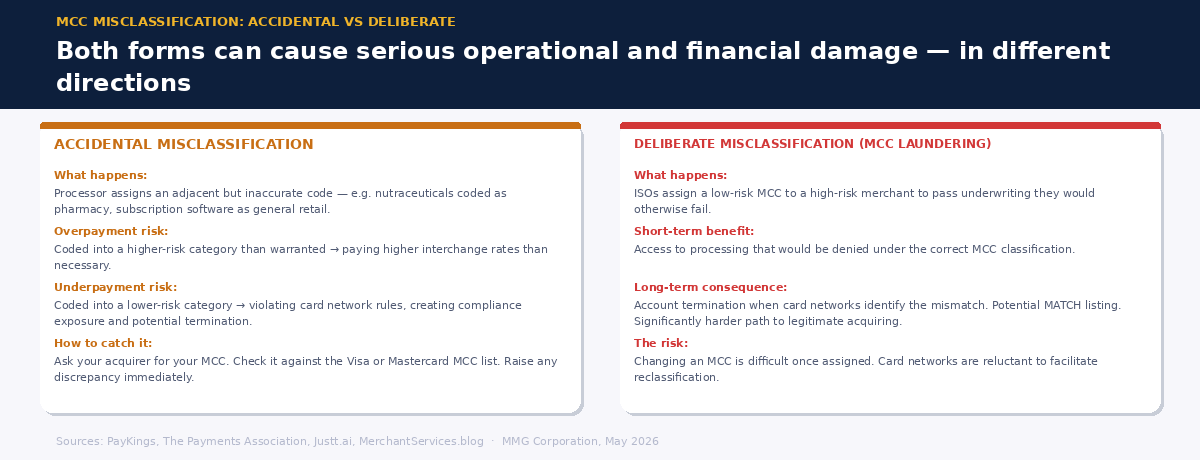

One of the least-discussed risks in payment processing is MCC misclassification — being assigned the wrong code at onboarding, either by mistake or by design.

Accidental misclassification happens when a processor assigns a code that is adjacent to the correct one but not precise. A nutraceuticals merchant might be coded as a pharmacy (MCC 5912) when a more specific code applies. A subscription software company might be coded as a generic retail merchant. The consequence is typically that the merchant pays incorrect interchange rates — either overpaying because they've been coded into a higher-risk category than their actual business warrants, or underpaying in a way that violates card network rules and creates compliance exposure.

Deliberate misclassification is a more serious problem. ISOs and payment facilitators occasionally assign low-risk MCC codes to high-risk merchants to get them through underwriting — a practice known as "MCC laundering." The short-term benefit is access to processing they would otherwise be denied. The long-term consequence is account termination when the card networks identify the mismatch, potential MATCH listing, and a significantly more difficult path to legitimate acquiring relationships afterward.

Changing an MCC once assigned is difficult. Card networks are generally reluctant to facilitate reclassifications, and the process can take months even when a genuine error is identified. The practical implication: check your MCC at onboarding, understand what it means for your account, and raise any discrepancy immediately rather than discovering it months later when the consequences have compounded.

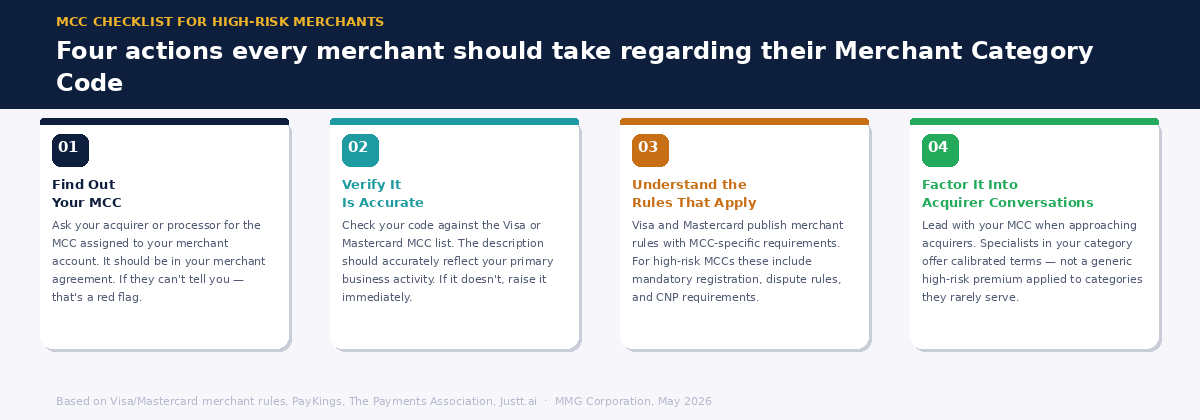

What to Do With This Information

Find out your MCC. Ask your acquirer or processor for the MCC assigned to your merchant account. This should be straightforward — it is on your merchant agreement and in your processing documentation. If your processor cannot or will not tell you your MCC, that is a significant concern in itself.

Verify it is accurate. Check the code against Visa's published MCC list or Mastercard's equivalent. The description should accurately reflect your primary business activity. If it doesn't — if you're a subscription nutraceuticals company coded as a general retailer, or a gambling platform coded as entertainment — raise it immediately with your acquirer.

Understand what rules apply to your code. Visa and Mastercard publish their merchant rules documents, which include MCC-specific requirements. For high-risk MCCs, these often include mandatory registration, specific dispute management requirements, and CNP-specific rules. Not knowing these requirements does not exempt a merchant from compliance.

Factor your MCC into acquirer conversations. When approaching a new acquirer, lead with your MCC alongside your processing history and chargeback data. Acquirers who specialize in your MCC category will have calibrated reserve and pricing structures that reflect actual industry experience — not a generic high-risk premium applied to a category they rarely serve.

The MCC is not a detail. It is the classification that shapes every financial and operational aspect of your merchant account — from the first transaction to the reserve structure to the rules your processor applies to your disputes. Merchants who understand their MCC, verify its accuracy, and use it intelligently in acquirer conversations are better positioned than those who treat it as administrative background noise.

MMGCorporation specializes in high-risk merchant acquiring across EU markets. If you want to understand how your MCC affects your processing setup — or how to find the right acquirer for your specific category — we're glad to help.