Most merchant account applications are declined not because of the business itself, but because of how the application is presented. A complete, well-organized file does not just improve approval chances — it shapes the terms you are offered.

Approaching a high-risk acquirer without the right preparation is one of the most common and costly mistakes merchants make. The underwriting process for a high-risk merchant account is not a formality — it is a genuine risk assessment, conducted by professionals who have seen every variation of the merchant file, and who make their decisions based on the quality and completeness of what you submit. The merchant who shows up with a complete, transparent, well-organized application gets better terms than the one who submits a partial file and fills in the gaps over two weeks of follow-up emails.

The good news is that the underwriting process is predictable. Acquirers are assessing the same set of factors every time: the business, its owners, its financial health, its compliance posture, and its risk management controls. Knowing what they are looking for — and preparing accordingly — is the most reliable way to get an approval quickly and negotiate terms from a position of strength rather than desperation.

What Acquirers Are Actually Assessing

Before building your documentation file, it helps to understand the underwriter's perspective. A high-risk acquirer is taking on financial exposure when they board a new merchant. If the merchant generates excessive chargebacks, produces fraud, or disappears with settlement funds in the pipeline, the acquirer bears the consequences. The underwriting process exists to quantify that risk — and to set terms (fees, reserves, monitoring intensity) that reflect it.

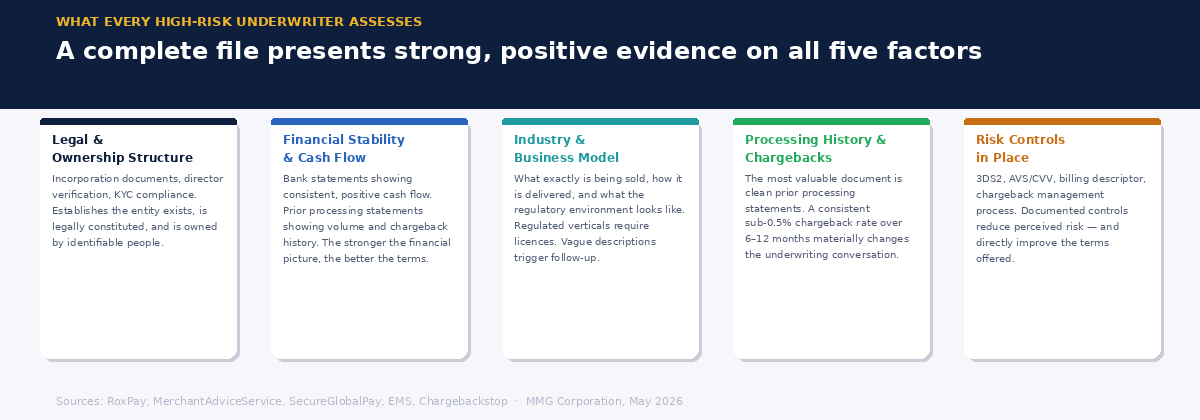

The five factors that drive every high-risk underwriting decision are: the legal and ownership structure of the business, financial stability and cash flow, the industry and business model, prior processing history and chargeback performance, and the risk controls in place. A strong file presents clear, positive evidence on all five. A weak file leaves gaps in any of them — and gaps are filled with assumptions that are almost always unfavorable.

Section 1: Business and Legal Documents

The starting point of every underwriting file is proof that the business exists, is legally constituted, and is owned by identifiable, verifiable people. For EU-based merchants, this means:

Company incorporation documents. Certificate of incorporation, articles of association, and proof of registered address. These establish that the legal entity exists and is in good standing.

Ownership and director verification. Identity documents — passport or national ID — for all directors and beneficial owners with 25% or more ownership. This is a KYC requirement under EU anti-money laundering regulations and is non-negotiable. Clear, valid, in-date documents process faster. Expired or low-quality copies cause delays.

Business licence and regulatory authorizations. For merchants in regulated verticals — iGaming, adult entertainment, financial services, pharmaceuticals — the relevant operating licence is mandatory. An unlicensed merchant in a licensed sector will not be approved regardless of how strong the rest of their file is. If licensing is pending, say so clearly and provide the application reference. Acquirers can work with merchants in the licensing process; they cannot work with merchants who misrepresent their regulatory status.

Proof of bank account. A recent bank statement (no older than three months) in the legal name of the contracting merchant company, showing the account details to which settlements will be paid. This is not optional — it is the account into which every settlement will flow, and it must be verified.

Section 2: Financial Documents

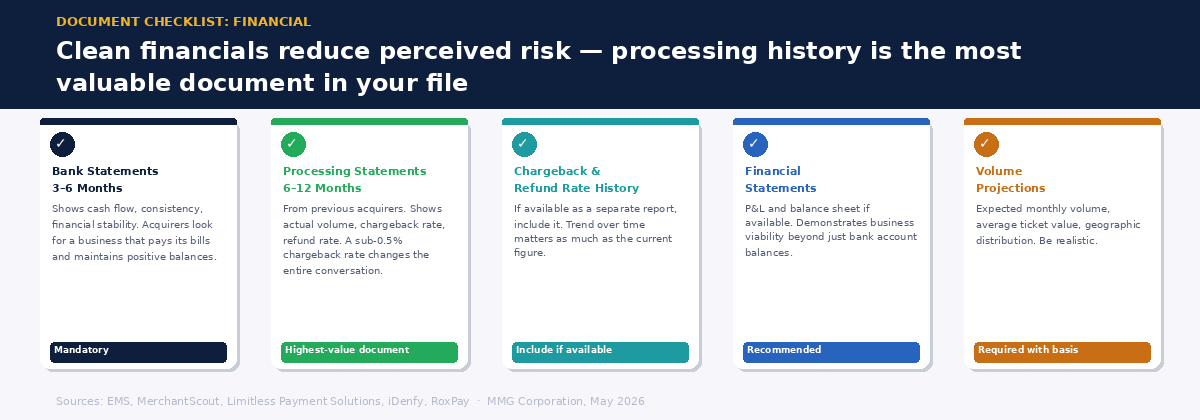

Financial documents tell the acquirer whether the business is stable enough to operate without generating financial risk to the acquiring relationship. Three to six months of bank statements are the standard requirement — they show cash flow, consistency, and overall stability. The acquirer is looking for a business that pays its bills, maintains a positive balance, and does not show signs of financial distress.

If the business has existing payment processing history, the most valuable document in the entire file is the processing statement from the previous acquirer. Six to twelve months of statements showing processing volume, chargeback rate, refund rate, and settlement amounts tells the underwriter what you will actually look like as a merchant — not what you project you will look like. A clean processing history with a chargeback rate consistently below 0.5% is the strongest single asset a merchant can bring to an underwriting conversation.

For new merchants without processing history, this gap is the biggest underwriting challenge. It can be partially addressed with strong financials, a detailed business plan, and evidence of risk controls — but there is no substitute for track record, and the initial terms offered to merchants without history will reflect that. Building clean processing history as early as possible, even at lower volumes, is the most reliable investment a new high-risk merchant can make.

Section 3: Website and Product Compliance

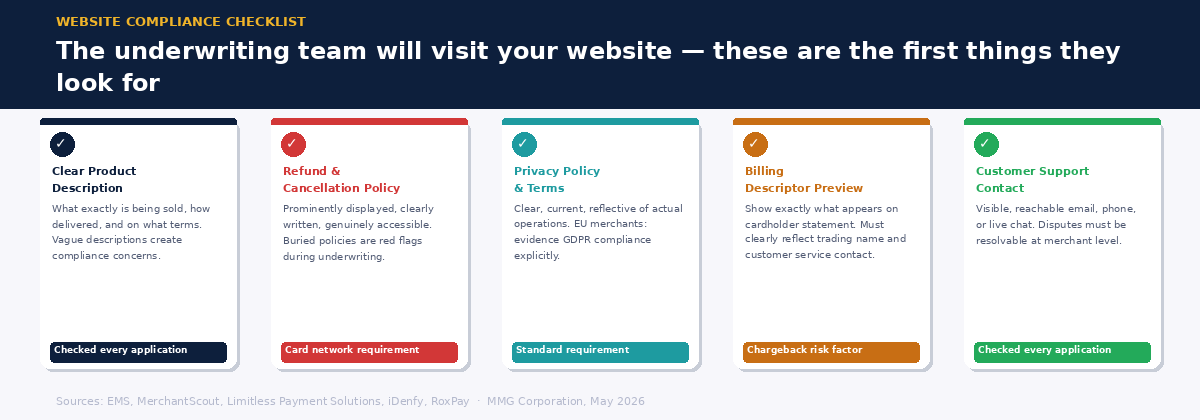

The acquirer's underwriting team will visit your website. They are looking for specific things — and the absence of any of them is a red flag that either delays the application or triggers additional questions.

Clear product and service description. What exactly is being sold? How is it delivered? What are the terms? Vague or misleading product descriptions create compliance concerns and reduce underwriter confidence. Describe your products clearly, accurately, and completely.

Refund and cancellation policy. Prominently displayed, clearly written, and genuinely accessible. This is not just a card network requirement — it is one of the first things an underwriter checks. A refund policy that is buried in the terms of service, difficult to find, or written in a way that discourages refund requests will raise concerns during underwriting.

Privacy policy and terms of service. Clear, current, and reflective of how the business actually operates. For merchants handling EU consumer data, GDPR compliance should be evidenced.

Billing descriptor preview. Show the underwriter what will appear on the cardholder's statement. It should clearly reflect the trading name and a customer service contact. A clear billing descriptor is both a consumer protection measure and a chargeback prevention tool — and acquirers increasingly assess it as part of the risk profile.

Customer support contact. A reachable customer service channel — email, phone, or live chat — that is visibly displayed. The acquirer needs to know that disputed transactions can be resolved at the merchant level before they become chargebacks.

Section 4: Risk Controls and Fraud Prevention

This is the section most merchants underestimate — and the one that most directly affects the reserve terms and fees they are offered. An acquirer who can see that a merchant has active, documented risk controls in place is underwriting a different risk profile than one who cannot.

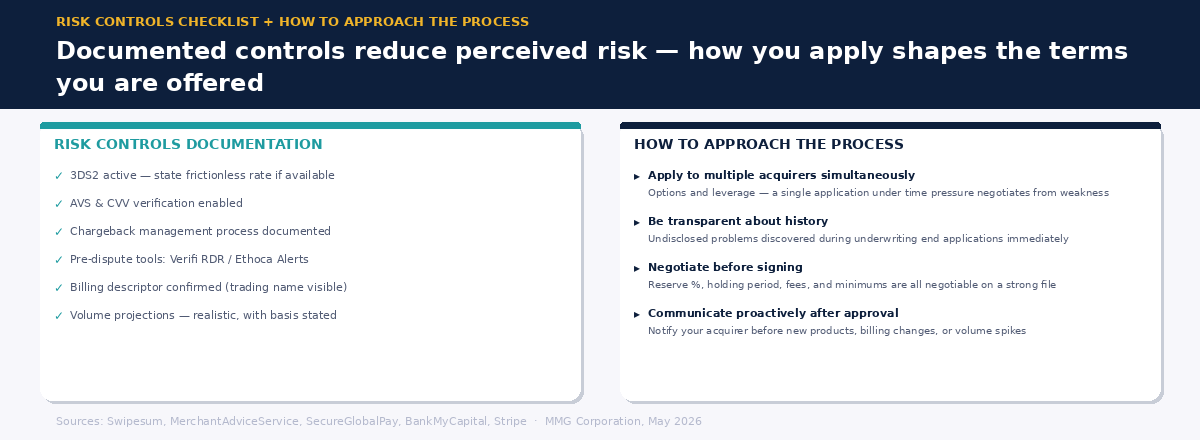

3DS2 implementation. Confirm that 3D Secure 2 is active on your checkout, state whether you are using native mobile SDKs, and provide your frictionless flow rate if available. This is increasingly assessed as a baseline expectation, not an optional feature.

AVS and CVV verification. Address Verification Service and Card Verification Value checks should be enabled. Document that they are active and describe how you handle mismatches.

Chargeback management process. Describe how you monitor chargebacks, how you respond to disputes, and what pre-dispute tools (Verifi RDR, Ethoca Alerts) you have in place. A merchant who can describe a documented dispute management process is materially easier to approve than one who has no plan.

Billing descriptor. Provide the exact descriptor that will appear on customer statements. Make it clear it matches your trading name.

Projected processing volume. State expected monthly volume, average transaction value, and geographic distribution of customers. Be realistic — significantly overestimating volume creates concerns about business model viability; significantly underestimating it creates problems when you scale and exceed agreed limits.

How to Approach the Process

Apply to multiple acquirers simultaneously. High-risk underwriting takes time, and approvals are not guaranteed on the first application. Approaching several specialist acquirers at the same time creates options and negotiating leverage. A merchant with one offer in hand is in a stronger position than one waiting on a single response under time pressure.

Be transparent about your history. Undisclosed terminations, prior chargebacks, or MATCH status discovered during underwriting will end an application immediately. Acquirers who know about a difficult history and can assess what has changed are more likely to approve than acquirers who discover problems they weren't told about.

Negotiate before signing. Reserve percentage, holding period, processing fees, and monthly minimums are all negotiable — particularly if your documentation is strong. The initial offer reflects the acquirer's risk assessment under uncertainty. A complete file that reduces uncertainty creates room for negotiation. Ask about a reserve review after six months of clean processing history.

Treat the relationship as ongoing, not transactional. Notify your acquirer before you launch new products, change your billing model, or significantly scale volume. The merchants who maintain stable, long-term acquiring relationships are those who communicate proactively rather than confronting their acquirer with surprises. A relationship built on transparency produces better terms over time than one built on minimal disclosure.

Getting into a well-structured high-risk acquiring relationship takes preparation. Staying in one takes consistent performance and clear communication. Both are manageable — with the right approach and the right partner.

MMGCorporation provides specialist acquiring for high-risk merchants across EU markets. If you're preparing to apply for a merchant account and want to talk through your file before you submit, we're glad to help.

Request Info