One acquirer means one point of failure. For a standard e-commerce merchant, that's a risk. For a high-risk merchant, it's a structural vulnerability that can end the business in a single email.

The Illusion of Stability

A merchant who has had the same acquiring relationship for two or three years, processes without incident, and maintains a clean chargeback record is a merchant who feels stable. That feeling is understandable — and it is also misleading. Payment processing stability for a high-risk merchant is not a property of the merchant alone. It is a property of the relationship between the merchant and their acquirer, mediated by the card networks, the regulatory environment, and the acquirer's own commercial decisions. None of those external factors are within the merchant's control.

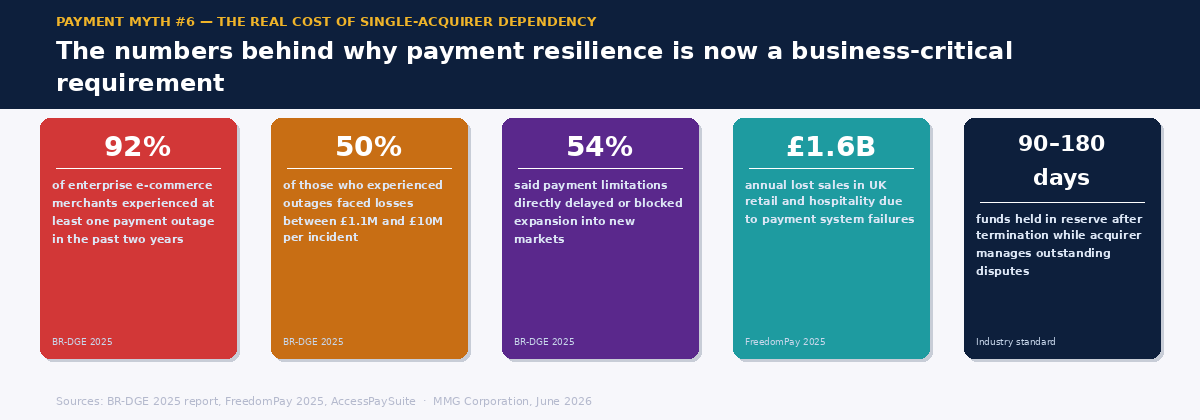

Industry research from 2025 found that 92% of enterprise e-commerce merchants experienced at least one payment outage in the past two years. Among those who experienced outages, 50% faced losses between £1.1 million and £10 million. A further 54% said payment limitations had directly delayed or blocked their expansion into new markets. These are not edge-case failures — they are the baseline experience of merchants who rely on payment infrastructure they do not control and cannot fully predict.

For high-risk merchants, the risk is compounded. The acquirer who terminates a standard merchant account does so through a commercial decision. The acquirer who terminates a high-risk merchant account may do so through a compliance decision — one driven by VAMP portfolio pressure, a shift in their risk appetite, a de-risking mandate from their correspondent bank, or a regulatory change that moves the goalposts overnight. Clean processing history does not protect against any of these.

Why Termination Hits Harder Than Merchants Expect

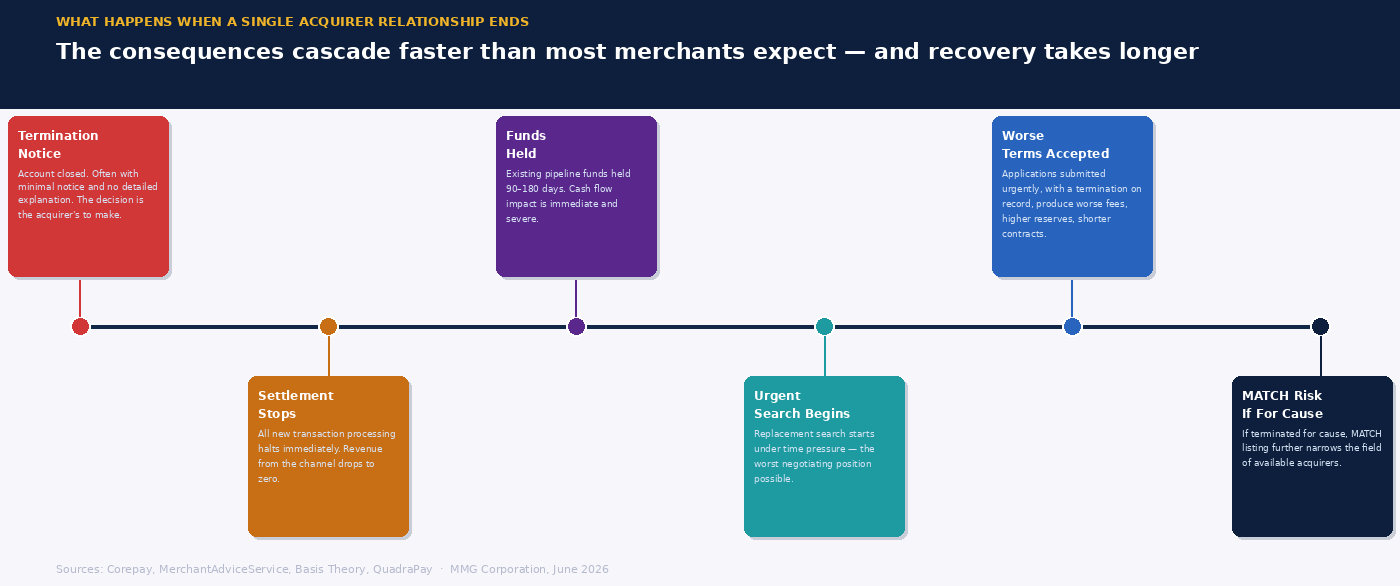

When a high-risk merchant account is terminated, the consequences are immediate and cascade quickly. Settlement stops. Funds already in the processing pipeline may be held in reserve for 90 to 180 days while the acquirer manages any outstanding dispute liability. Revenue from in-flight transactions that have been authorized but not yet settled is frozen. The merchant's ability to process new payments drops to zero while the replacement search begins.

The replacement search itself is the second problem. Onboarding a new high-risk merchant account takes time — typically three to ten business days for a complete file, but often longer when the application arrives under time pressure, with incomplete documentation, and with a recent termination on the record. A merchant who was terminated yesterday and needs processing tomorrow is negotiating from the weakest possible position. The terms they accept under those conditions are rarely the terms they would have accepted if they had approached the same acquirer six months earlier, calmly, with full documentation and an existing alternative account already live.

And if the termination resulted in a MATCH listing, the field of available acquirers narrows further still. Standard processors decline automatically. Specialist acquirers who will consider MATCH-listed merchants do so with stricter terms, higher reserves, and more intensive monitoring — all of which are compounded by the urgency of the merchant's situation.

VAMP Has Made Single-Acquirer Dependency More Dangerous

Before VAMP, an acquirer's decision to exit a high-risk merchant was primarily a commercial one — was this merchant worth the operational overhead? Since April 2025, it has also become a compliance one. Acquirers are now directly fined for portfolio-level VAMP ratios. A merchant whose combined fraud alert and dispute rate pushes the acquirer toward their Above Standard or Excessive threshold becomes a liability to the acquirer's entire portfolio — not just their own account.

The rational response for an acquirer managing VAMP pressure is to exit merchants who are contributing to ratio risk — and to do it before the threshold is breached, not after. This means merchants can be exited not because their individual performance is unacceptable in isolation, but because the acquirer's portfolio dynamics have changed. A merchant who represents 0.8% of the acquirer's volume but contributes a disproportionate share of the VAMP ratio is a candidate for removal even if their own chargeback rate is well within normal bounds.

The merchant with a single acquiring relationship has no leverage in this situation. They cannot route volume away to reduce their contribution to the acquirer's ratio. They cannot demonstrate that they are actively managing the issue by showing stable processing elsewhere. They are entirely dependent on a decision that is being made at the portfolio level — not on their behalf.

The Commercial Benefits Beyond Risk Management

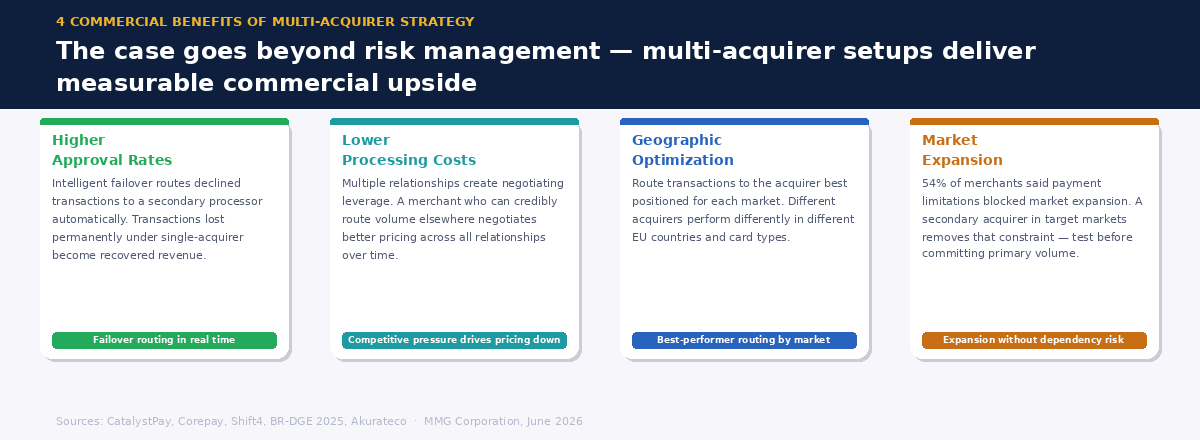

The case for multiple acquiring relationships is not only defensive. Multi-acquirer strategies deliver measurable commercial benefits that single-acquirer merchants forfeit by default.

Higher approval rates. Different acquirers have different BIN routing, different issuer relationships, and different optimization for specific geographies and card types. A transaction declined by one acquirer may be approved by another. Multi-acquirer routing with intelligent failover — sending declined transactions to a secondary processor automatically — recovers approval rates that a single-acquirer merchant loses permanently.

Lower processing costs. Working with multiple acquirers creates negotiating leverage that a single-acquirer relationship does not. A merchant who can credibly offer to route volume elsewhere is in a different position than one who has no alternative. Over time, the competitive pressure of multiple relationships drives better pricing across all of them.

Geographic optimization. Different acquirers perform differently in different markets. A specialist acquirer with deep EU coverage may produce significantly better acceptance rates for European transactions than one without. A merchant processing across multiple EU markets benefits from routing transactions to the acquirer best positioned to process them — which requires having more than one.

Market expansion without risk. A 2025 research study found that over 54% of merchants said payment limitations had directly delayed or blocked their expansion into new markets. A multi-acquirer setup removes this constraint — new markets can be tested through an existing secondary acquirer before primary volume is committed.

How to Build a Multi-Acquirer Setup

The objection most merchants raise to multi-acquirer strategy is complexity — managing two or more acquiring relationships, integrations, settlement accounts, and reporting streams is operationally heavier than managing one. This is true, and it is a real consideration. But the complexity is manageable, and it is substantially reduced by the right infrastructure.

Start with a secondary relationship before you need it. The worst time to onboard a second acquirer is immediately after your primary account has been terminated. The best time is when the primary relationship is stable, your file is clean, and you can approach the underwriting process from a position of strength rather than urgency. A secondary account that processes a modest volume keeps the relationship live and the integration tested — and means you have somewhere to route to if you need to.

Consider payment orchestration. Payment orchestration platforms connect merchants to multiple acquirers through a single integration, with intelligent routing logic that distributes transactions based on approval rates, cost, geography, and risk profile. For merchants operating across multiple EU markets and processing significant volumes, orchestration removes much of the operational overhead of multi-acquirer management. We covered payment orchestration in detail in an earlier article — the multi-acquirer resilience case is one of its strongest use cases.

Choose acquirers with complementary strengths. A primary acquirer with deep vertical experience in your industry, and a secondary with strong geographic coverage in your key expansion markets, gives you both redundancy and optimization. Two identical acquirers give you only redundancy — which is valuable, but not the full benefit of the strategy.

The single-acquirer relationship feels like simplicity. It is actually exposure — to one bank's risk appetite, one compliance decision, one VAMP portfolio review, one de-risking exit. The merchants who have lived through that exposure once build redundancy before the second time. The ones who build it before the first time are the ones who never have to negotiate from desperation.

MMGCorporation works with high-risk merchants on acquiring strategy across EU markets — including how to structure a multi-acquirer setup that provides genuine resilience without unnecessary operational complexity. If you want to talk through your current setup, we're glad to help.

Get in touch