MATCH listing is serious. It makes acquiring significantly harder, it follows you for five years, and most merchants discover it at the worst possible moment. But it does not make payment processing impossible — and understanding what it actually is, and what it isn't, is the starting point for recovery.

What MATCH Actually Is

MATCH stands for Member Alert to Control High-Risk Merchants. It is a database maintained by Mastercard — and accessed by acquiring banks globally — that contains records of merchants whose accounts have been terminated for cause. Visa operates its own equivalent database, the Visa Merchant Screening Service (VMSS). When processors refer to the MATCH list or the Terminated Merchant File (TMF), they are typically referring to the Mastercard database, though both networks' records will be checked during underwriting.

When an acquirer terminates a merchant account for a qualifying reason, Mastercard requires that the acquirer add the merchant to MATCH within one business day of termination. The entry includes business details, principal owner information, and a reason code identifying why the merchant was listed. Mastercard does not verify the accuracy of these entries — the responsibility lies entirely with the adding acquirer. The entry then stays on the database for five years, after which it ages off automatically.

Here is the detail most merchants do not know: they are rarely informed when they are added. There is no notification from Mastercard, and the adding acquirer is not obligated to tell the merchant. Most businesses discover their MATCH status only when a new merchant account application is declined — and an underwriter reveals the reason. By then, the listing has often been in place for weeks or months.

What Gets You Listed — and What Doesn't

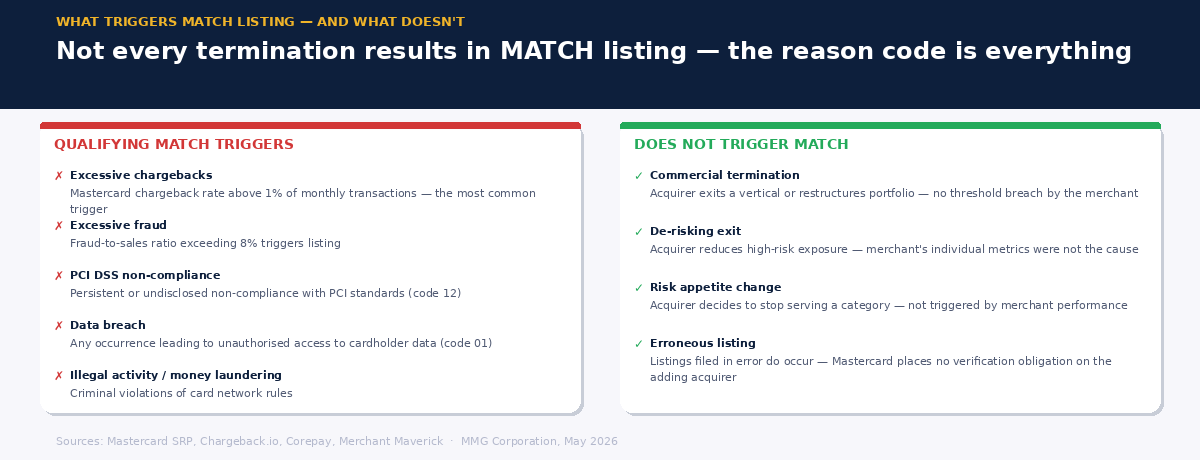

MATCH listing is not triggered by every merchant account termination. It requires a specific qualifying reason, defined by one of Mastercard's reason codes — updated most recently in February 2025. The most common triggers are excessive chargebacks (a chargeback rate above 1% of monthly transactions with Mastercard), fraud (a fraud-to-sales ratio exceeding 8%), and PCI DSS non-compliance. Other reason codes cover data breaches, money laundering, illegal activity, identity theft, and collusion.

What does not trigger MATCH listing: a merchant whose account is terminated for commercial reasons — the acquirer exiting a vertical, a portfolio restructuring, or a risk appetite change — without the merchant having breached any of the qualifying thresholds. These terminations, which are common in de-risking scenarios, should not result in a MATCH entry. If a merchant in this situation discovers they have been listed, that listing may have been filed in error — which is more common than most people know, because Mastercard places no verification obligation on the adding acquirer.

Understanding your reason code is therefore the first and most important step after discovering a MATCH listing. A code 12 (PCI non-compliance) can be resolved by achieving compliance, which may qualify the merchant for early removal. A code 01 (account data compromise) carries different implications than a code 04 (excessive chargebacks). The path forward depends entirely on why you are listed — and the reason code is the starting point for determining what is possible.

Why MATCH Does Not Mean the End of Processing

The myth — that MATCH listing makes card payment processing impossible — is understandable, because for standard merchant account providers it is effectively true. Most mainstream processors and banks will decline a MATCH-listed application without further review. Their underwriting is automated, their risk appetite is low, and the MATCH flag triggers an immediate rejection. For a merchant who has only ever worked with standard providers, the experience of applying and being declined repeatedly can feel like a definitive answer.

It is not. The MATCH list is explicitly an informational tool, not a blanket prohibition. Mastercard's own documentation describes it as a database for acquiring banks to use in risk assessment — not a list of merchants who are permanently excluded from card payment processing. The decision about whether to work with a MATCH-listed merchant rests with the individual acquirer, and acquirers differ enormously in their risk appetite.

Specialist high-risk acquirers — those who have built their business specifically around industries and merchants that standard processors will not serve — assess MATCH-listed applications case by case. The factors they weigh include the reason code, the age of the listing, what the merchant has done to address the underlying issue since listing, the current processing profile and chargeback trajectory, and the nature of the business itself. A merchant listed three years ago for excessive chargebacks who has since implemented pre-dispute tools, reduced their ratio, and has clean processing history at an alternative provider is a fundamentally different proposition from a merchant listed last month for fraud.

The terms will be less favorable than for a non-MATCH merchant: higher processing fees, stricter reserve requirements, closer monitoring, and potentially shorter initial contract terms pending review. That is the realistic expectation. But processing is achievable — with the right acquirer, the right preparation, and the right framing of the application.

Getting Off the MATCH List

Early removal from the MATCH list is possible in limited circumstances — and impossible in others. Understanding the distinction saves significant time and frustration.

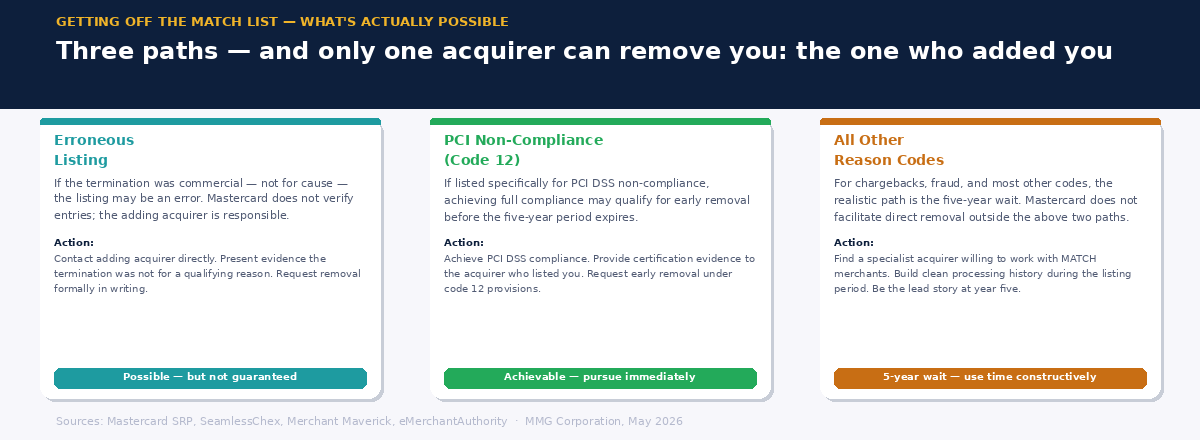

The acquirer who added you is the only party who can remove you. Mastercard cannot remove an entry directly, and no third party can do it on your behalf. If you believe you were listed in error — because the termination was commercial rather than for cause, or because your chargeback rate was miscalculated — you must contact the adding acquirer directly, make your case, and request removal. This process can be slow and is not guaranteed to succeed, but erroneous listings can and do get corrected.

If you were listed for PCI non-compliance (reason code 12), achieving full PCI DSS compliance may qualify you for removal before the five-year period expires. This is the clearest path to early resolution and worth pursuing immediately.

For all other reason codes, the realistic path is the five-year wait, combined with using that period to rebuild a clean processing record. A merchant who has been MATCH-listed for chargebacks, has found a specialist acquirer willing to work with them, and has spent three years demonstrating consistently low dispute rates is in a significantly stronger position at year four than one who has done nothing and is simply waiting for the clock to run out.

One practical alternative worth noting: the MATCH list covers card payment processing. ACH and direct debit payment options are not subject to MATCH screening. For merchants whose customer base can support non-card payment methods — particularly subscription businesses and B2B merchants — ACH processing can maintain revenue during the card processing recovery period, and in some cases offers advantages for high-ticket recurring billing.

The Five Steps After Discovering a MATCH Listing

Find out your reason code. Ask the acquirer who terminated you, or ask a specialist processor to check on your behalf. The reason code determines every subsequent decision.

Assess whether the listing is accurate. If your account was terminated for commercial reasons without a threshold breach, you may have grounds to request removal. Act on this quickly — the sooner you challenge an erroneous listing, the more straightforward the resolution.

Resolve the underlying issue. If the listing was for excessive chargebacks, implement the controls that change the trajectory. If it was for PCI non-compliance, achieve compliance. Approaching a new acquirer without having addressed the root cause is the fastest way to be declined again.

Approach specialist acquirers — and approach several simultaneously. Standard processors will decline. Specialist high-risk acquirers who explicitly work with MATCH-listed merchants exist, and their underwriting is based on the full picture — not just the listing flag. Apply to multiple providers at the same time to create options and negotiating leverage.

Use the recovery period constructively. Every month of clean processing history with a specialist acquirer is an asset in future conversations. Document your chargeback rates, your dispute management processes, and your compliance posture. By the time the five-year listing expires, the record you have built should be the lead story — not the listing itself.

MATCH listing is not the end of the road. It is a serious obstacle with a defined structure — a reason code, a five-year timeline, and a specific set of options depending on the circumstances. Merchants who understand that structure recover faster than those who treat the listing as a permanent verdict.

MMG specializes in high-risk merchant acquiring, including working with merchants navigating difficult processing situations. If you'd like to talk through your options, we're glad to help.

Request Info