Some of it is. But the majority isn't — and treating the entire problem as a dishonesty problem leads merchants to deploy the wrong solutions, miss the disputes they could prevent, and antagonize customers who had no fraudulent intent at all.

The Scale of the Problem

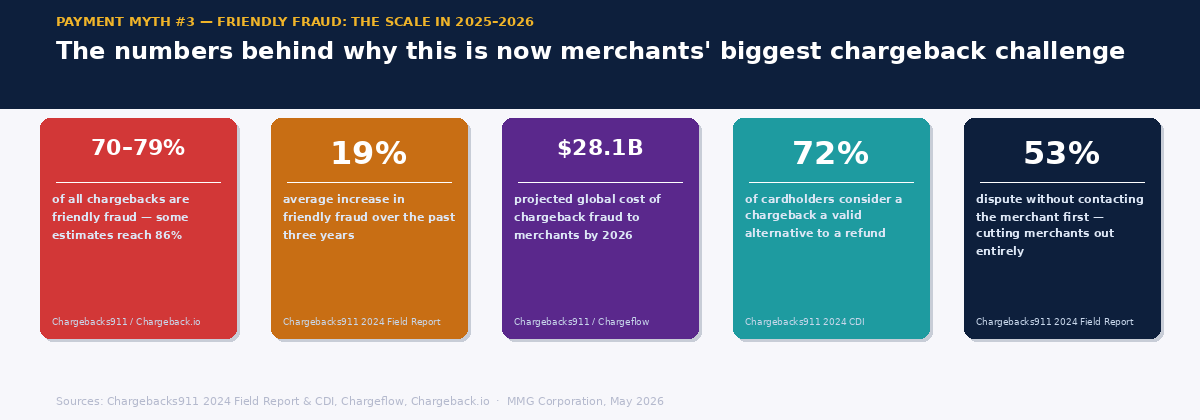

Friendly fraud — disputes filed against legitimate transactions — now accounts for between 70% and 79% of all chargebacks, with some broader definitions placing the figure as high as 86%. It has increased by approximately 19% over the past three years. By 2026, chargeback fraud is expected to cost merchants $28.1 billion globally — a 40% increase from 2023.

For high-risk merchants in verticals like iGaming, digital goods, nutraceuticals, and subscription services, these numbers are not abstract. Friendly fraud is the dominant driver of chargeback exposure, and the VAMP framework means every dispute — regardless of intent — counts against the ratio that determines your acquirer relationship. Understanding what actually generates these disputes is the prerequisite for doing anything useful about them.

Three Types of Friendly Fraud — and Why the Distinction Matters

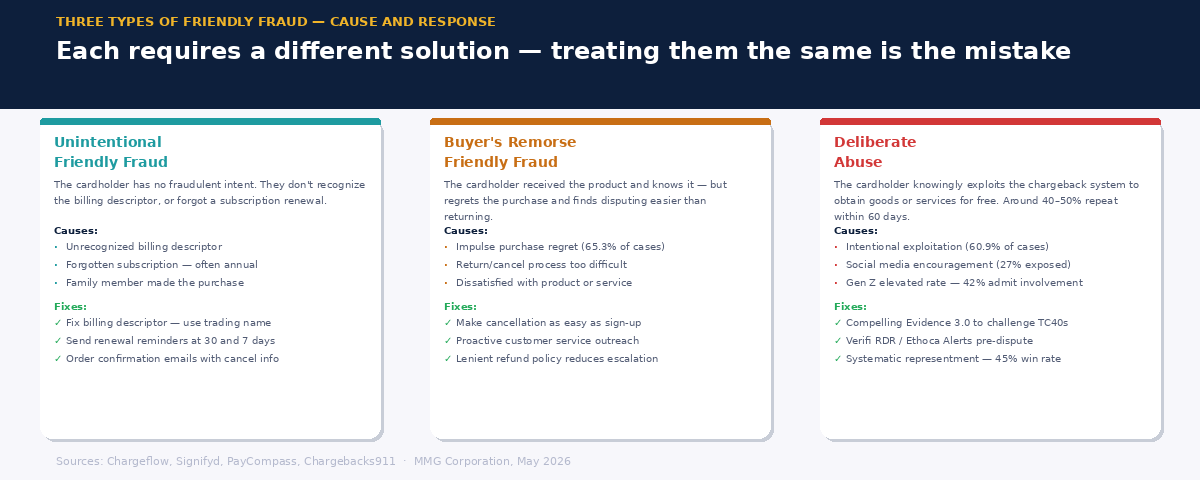

Friendly fraud is not a single phenomenon. It falls into three meaningfully different categories, and the right response to each is different.

Unintentional friendly fraud occurs when a cardholder disputes a legitimate transaction without any fraudulent intent. The most common trigger is a billing descriptor they don't recognize — a legal entity name, a processor code, or an abbreviation that bears no resemblance to the product they purchased. Forgotten subscriptions are another significant driver, particularly for annual renewals where the gap between sign-up and billing can be twelve months or more. The cardholder is not lying. They genuinely do not know what the charge is.

Buyer's remorse friendly fraud sits in a gray zone. The cardholder received the product or service, and they know it — but they regret the purchase and find disputing through the bank easier than navigating the merchant's returns process. Industry data indicates that 65.3% of friendly fraud cases are driven by buyer's remorse. These customers are not fraudsters in any meaningful sense. They are unhappy customers who found a frictionless exit that the merchant failed to provide.

Deliberate abuse is the category that matches the myth: cardholders who knowingly exploit the chargeback system to obtain products or services for free, or to claim refunds they are not entitled to. Around 60.9% of friendly fraud cases involve some element of intentional abuse — though it is worth noting that these categories are not mutually exclusive, and many cases involve more than one driver. Social media has become a meaningful accelerant: 27% of consumers report seeing posts that encourage chargeback abuse, and Gen Z in particular shows elevated rates of first-party fraud. Around 40–50% of those who commit deliberate friendly fraud repeat the behavior within 60 days.

Why Treating It All as Dishonesty Is Expensive

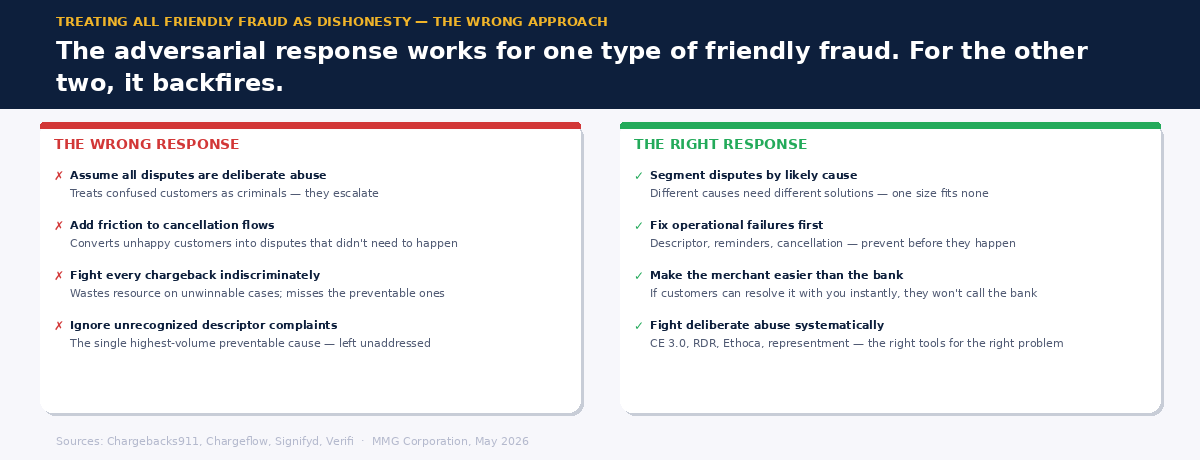

When merchants assume all friendly fraud is deliberate, the response is typically adversarial: tighten the dispute process, fight every chargeback, add friction to cancellation flows to reduce refund requests. For the 60% of cases that involve deliberate abuse, some of this is appropriate. For the significant portion of cases that are unintentional or remorse-driven, it makes the situation worse.

A customer who disputed a charge because they genuinely didn't recognize the billing descriptor, and who then receives an adversarial response to their dispute, is not a fraudster who has been caught. They are a confused customer who has now been antagonized. They will not return, they will leave negative reviews, and they may file additional disputes out of frustration.

More practically: the preventable friendly fraud — the unintentional and remorse-driven categories — can be addressed at almost zero cost with operational changes that have no downside. A billing descriptor that clearly shows the brand name the customer recognizes. A renewal reminder sent 7 to 30 days before an annual subscription renews. A cancellation flow that takes two clicks rather than a phone call. These changes do not require legal action, fraud scoring, or chargeback representment. They require operational attention to the customer experience at the points where disputes are most commonly generated.

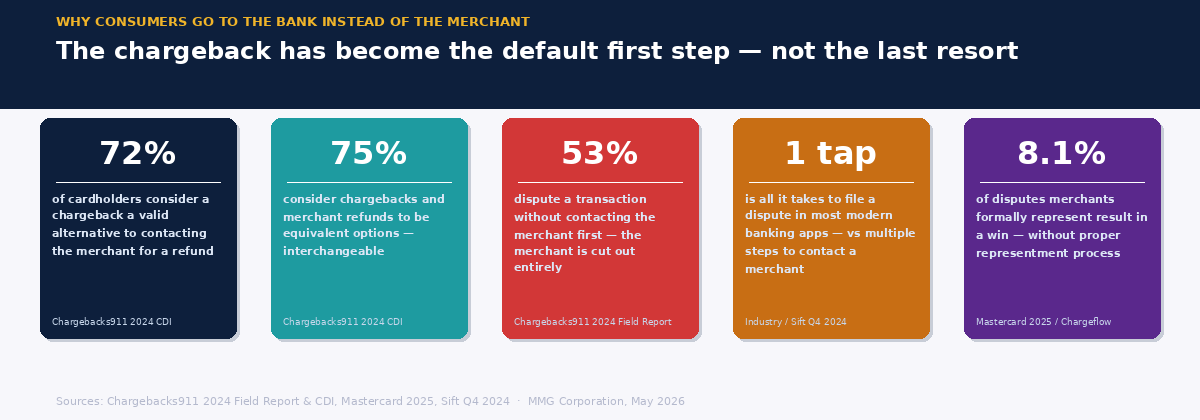

The deliberate abuse category does require a different response — and that response is also worth understanding clearly. Visa's Compelling Evidence 3.0 framework allows merchants to challenge fraud-coded chargebacks by demonstrating that the cardholder completed a prior legitimate, undisputed transaction from the same device and location. Pre-dispute tools like Verifi RDR allow merchants to resolve disputes before they register as chargebacks. And consistent representment — formally contesting chargebacks with documentation — produces win rates significantly above the industry average of 8.1% when done properly.

The Consumer Psychology Behind the Chargeback Default

One reason friendly fraud has grown so significantly is that the chargeback has become, for many consumers, the default first step rather than the last resort. Seventy-two percent of cardholders now consider filing a chargeback with their bank a valid alternative to requesting a refund from the merchant. Seventy-five percent consider the two methods equivalent. Fifty-three percent dispute a transaction with their bank without contacting the merchant at all.

This shift in consumer behavior has been driven by two things: the ease with which disputes can now be filed — often a single tap in a banking app — and the speed with which banks resolve them in the consumer's favor. From the consumer's perspective, disputing through the bank is faster, easier, and almost always successful. The merchant is cut out of the resolution process entirely.

For merchants, the response to this behavioral shift is not to make the bank dispute harder — that is not within a merchant's control. The response is to make the merchant interaction so easy, fast, and satisfactory that the consumer has no reason to go to the bank in the first place. A customer who gets an immediate refund or a helpful resolution from the merchant does not file a dispute. The dispute is the outcome of a customer experience failure, not just a consumer behavior problem.

The Practical Checklist

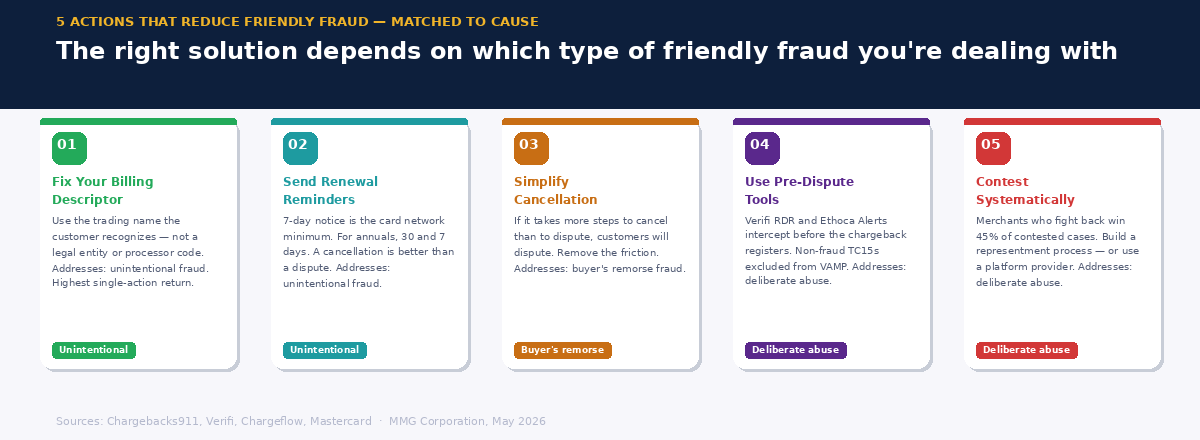

Fix the billing descriptor. This is the single highest-return action available. If the descriptor on the customer's statement doesn't match the brand they recognize, a proportion of your disputes are being generated before the customer even questions whether to contact you. Clear billing descriptors — showing the trading name, not a legal entity or processor code — address unintentional friendly fraud at source.

Send renewal reminders. Card network rules require 7-day advance notification for recurring billing. For annual subscriptions, send reminders at 30 days and again at 7. A customer who cancels before the charge is a closed chapter. A customer who disputes after the charge is a chargeback, a fee, and a VAMP ratio impact.

Make cancellation easier than disputing. If a customer can cancel in two clicks, they will. If they can't, they'll call their bank, which can. The friction that merchants add to cancellation flows does not retain customers — it converts them into disputes. Remove it.

Use pre-dispute tools for deliberate abuse. Verifi RDR and Ethoca Alerts intercept disputes before they register as chargebacks. For non-fraud TC15 disputes, these tools keep the incident out of the VAMP numerator entirely.

Fight the ones worth fighting. Merchants win an average of 45% of chargebacks they contest — significantly better than the 8.1% of disputes they represent through formal channels without proper documentation. Build a representment process, or use a platform provider. Merchants who fight back systematically have measurably better outcomes than those who absorb every chargeback without response.

Friendly fraud is not one problem — it is three. The merchants who manage it effectively are those who understand which category they are dealing with in each case, and who apply the right response to each. Treating all of it as deliberate dishonesty is not only inaccurate — it leaves the most preventable disputes unaddressed and the most recoverable chargebacks unfought.

MMGCorporation specializes in high-risk merchant acquiring. If you want to talk through your chargeback profile and how it affects your processing setup, we're here for that conversation.