It's one of the most common explanations merchants reach for after a termination. It's also usually wrong — or at best, incomplete. The industry is rarely the real reason. The processing profile almost always is.

Why the Industry Explanation Feels True

When a termination notice arrives with no detailed explanation, merchants naturally look for a reason. The industry they operate in is visible, obvious, and impossible to change — so it becomes the explanation that fits. And there is some truth in it: industry classification does influence baseline risk assessment. An iGaming merchant is underwritten differently from a software merchant from day one, and some acquirers do have blanket exclusions for specific verticals.

But blanket exclusions — the true industry-based refusals — are much less common than merchants assume. What is far more common is the outcome-based termination: an acquirer assessed this specific merchant's chargeback history, fraud rates, VAMP ratio exposure, and compliance posture, found the risk-to-revenue balance unfavorable, and exited the relationship. The industry was a factor in setting expectations. The processing profile was the reason for the decision.

The distinction matters enormously, because it determines whether anything can be done — now, and in future relationships.

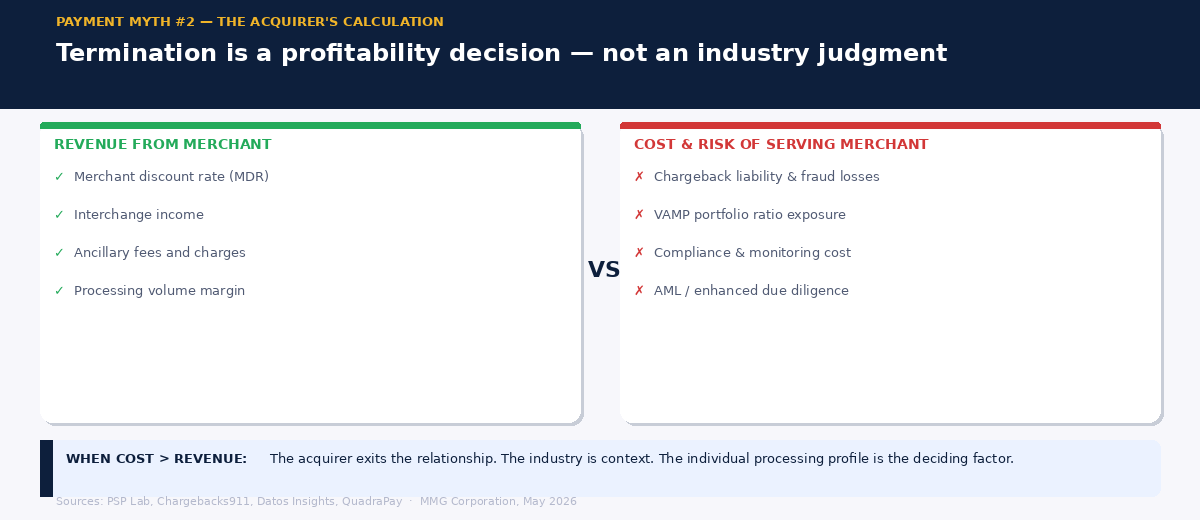

What Acquirers Are Actually Calculating

An acquirer's decision to exit a merchant relationship is a profitability calculation — and a compliance one. On one side of the equation is the revenue: the merchant discount rate, interchange income, and ancillary fees generated by processing the merchant's volume. On the other side is the cost: the operational overhead of monitoring the account, the liability for chargeback losses, the compliance cost of enhanced due diligence, and — since April 2025 — the direct VAMP exposure created by the merchant's fraud and dispute ratio within the acquirer's portfolio.

When that balance tips — when the cost and risk of serving a merchant exceeds what the relationship generates — the acquirer exits. It is not a moral judgment and it is rarely a regulatory requirement. It is a commercial decision, made on the basis of individual merchant data that the merchant may never see.

The data that drives the decision includes chargeback ratio and trend over time, TC40 fraud alert rate, VAMP ratio contribution to the acquirer's portfolio, reserve utilization, PCI compliance status, and the overall stability and predictability of processing volume. These are all metrics a merchant can influence. None of them are determined solely by the industry the merchant operates in.

What industry does determine is the baseline expectation. Acquirers underwriting an iGaming merchant expect higher dispute rates than they would from a standard e-commerce merchant. The threshold for acceptable performance is calibrated to the industry. A chargeback rate that would be alarming for a software company may be entirely manageable for a gaming platform — if it is within the range the acquirer planned for. The problem arises when a merchant's profile significantly exceeds the industry baseline, or when the overall risk environment shifts — as it did with VAMP's introduction — and the tolerable range contracts.

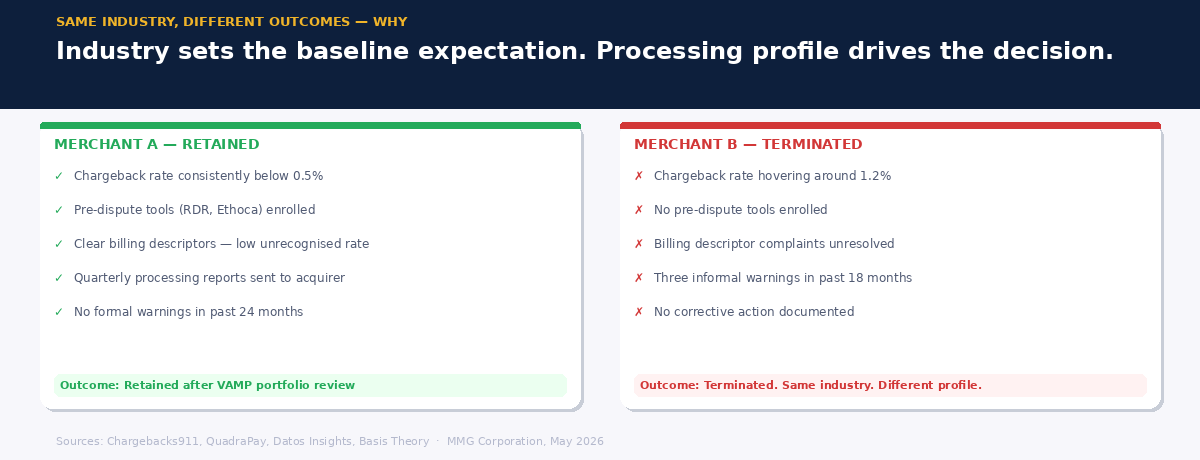

Why Two Merchants in the Same Industry Get Different Outcomes

Consider two iGaming merchants, both operating legally in the EU, both processing similar monthly volumes. Merchant A has a chargeback rate consistently below 0.5%, uses pre-dispute tools that intercept fraud alerts before they escalate, maintains clear billing descriptors, and has provided their acquirer with quarterly processing reports showing stable, well-managed operations. Merchant B has a chargeback rate hovering around 1.2%, has not enrolled in any pre-dispute service, and has had three informal warnings from their acquirer over the past 18 months.

When VAMP thresholds tighten and the acquirer reviews its portfolio, which merchant gets retained? The industry is the same. The risk profile is not.

This is not a hypothetical — it reflects how acquirer portfolio reviews actually work. Acquirers now use AI-powered risk models that assess individual merchant transaction patterns, behavioral signals, and industry risk indicators in real time. The days of manual review where a sympathetic account manager might overlook a difficult quarter are largely over. The decision is driven by data, and the data is specific to the merchant's actual performance.

The implication is straightforward: a merchant who believes their termination was purely industry-driven, and who takes no action to improve their processing profile before approaching a new acquirer, will likely face the same outcome again. The problem follows the merchant — not the industry classification.

What Actually Triggers Termination — and What Doesn't

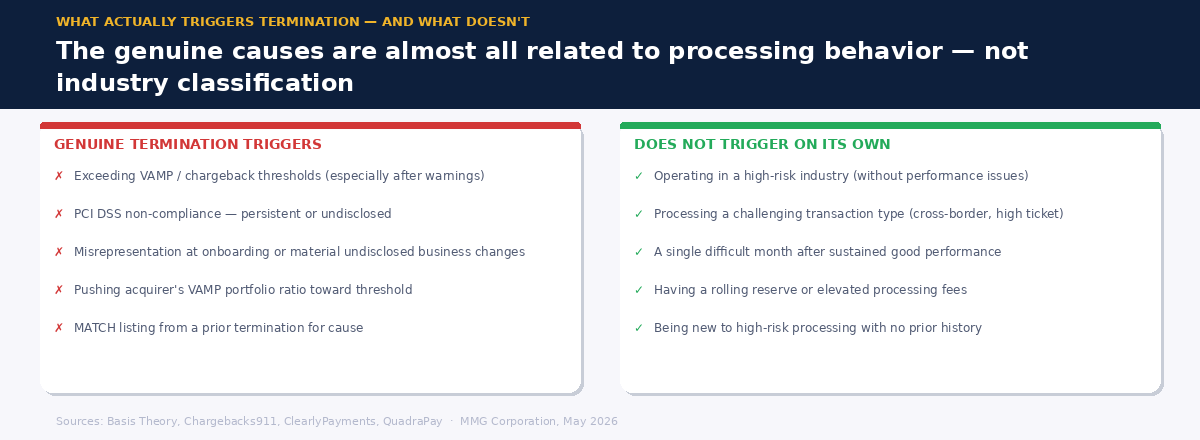

Understanding the genuine triggers for merchant account termination helps separate the controllable from the structural. The most common causes fall into three categories.

Threshold breaches. Exceeding Visa or Mastercard chargeback thresholds — or, under VAMP, exceeding the combined fraud alert and dispute ratio — triggers a formal monitoring program. Card networks notify the acquirer, who then faces a choice: work with the merchant to remediate, or exit the relationship before the acquirer itself faces fines. Merchants who have received warnings and not acted on them are the most likely to be terminated at this stage.

Compliance failures. PCI DSS non-compliance, failure to disclose material changes to business model or products, or misrepresentation during onboarding all create grounds for immediate termination — and MATCH listing. These are genuine industry-agnostic triggers: a compliant iGaming merchant is at less risk than a non-compliant software company.

Portfolio-level VAMP pressure. Under VAMP, an acquirer's aggregate portfolio ratio must stay below 0.5% (Above Standard) and 0.7% (Excessive). A merchant whose dispute and fraud profile pushes the acquirer toward those thresholds creates portfolio-level pressure — even if the merchant themselves has not breached their own individual threshold. The acquirer may exit the merchant not because they are above their limit, but because the acquirer needs headroom across the portfolio.

What does not typically trigger termination on its own: operating in a high-risk industry, processing a challenging transaction type, or having a single bad month after a sustained period of good performance. These may prompt a conversation, or a reserve adjustment. They do not, by themselves, end the relationship.

What To Do After a Termination — and Before the Next One

If a termination has already occurred, the first step is to understand it accurately. Request a written explanation from the acquirer — vague explanations are common but a specific reason is always worth pursuing, both for operational understanding and because new acquirers will ask. Download at least six months of processing statements, chargeback reports, and compliance documentation before losing dashboard access.

Check your MATCH status. Terminations for cause require MATCH listing by Mastercard. A MATCH-listed merchant faces a significantly harder path to new processing — but not an impossible one, and specialist high-risk acquirers do assess MATCH-listed merchants case by case. Knowing your status is essential before approaching any new provider.

Before approaching a new acquirer, address the underlying issue. If the termination was chargeback-driven, implement the controls that will change the trajectory: pre-dispute tools, better billing descriptors, cleaner cancellation flows. If it was compliance-related, resolve the specific gap. Approaching a new acquirer with a clear explanation of what happened and what has changed is a materially different conversation from approaching them with an industry-is-to-blame narrative that implies no corrective action has been taken.

Finally — and most importantly — do not approach a single acquirer. Apply to multiple specialist providers simultaneously. The underwriting processes take time, and the negotiating position of a merchant who has one offer in hand is significantly stronger than one who is waiting on a single response under time pressure.

The myth that industry classification is the primary driver of termination decisions leads merchants to feel powerless — and to take no action before their next relationship. The reality is that the processing profile is almost always the deciding factor, and the processing profile is something a merchant can actively manage. Understanding the difference is where recovery starts.

MMG specializes in high-risk merchant acquiring. If you've been terminated and want to understand your options, or if you're looking to build a more resilient processing setup before a problem arises, we're here to talk.