Three out of four consumers prefer to resolve payment issues through their bank rather than contacting the merchant. For subscription businesses, understanding why — and what to do about it — is no longer optional.

There is a moment that subscription merchants know well. A chargeback arrives. The reason code says "unauthorized transaction." The merchant pulls the records and finds that the customer signed up willingly, received the service, and was billed exactly as the terms described. The charge was entirely legitimate. And yet, rather than cancelling or requesting a refund, the customer went straight to their bank.

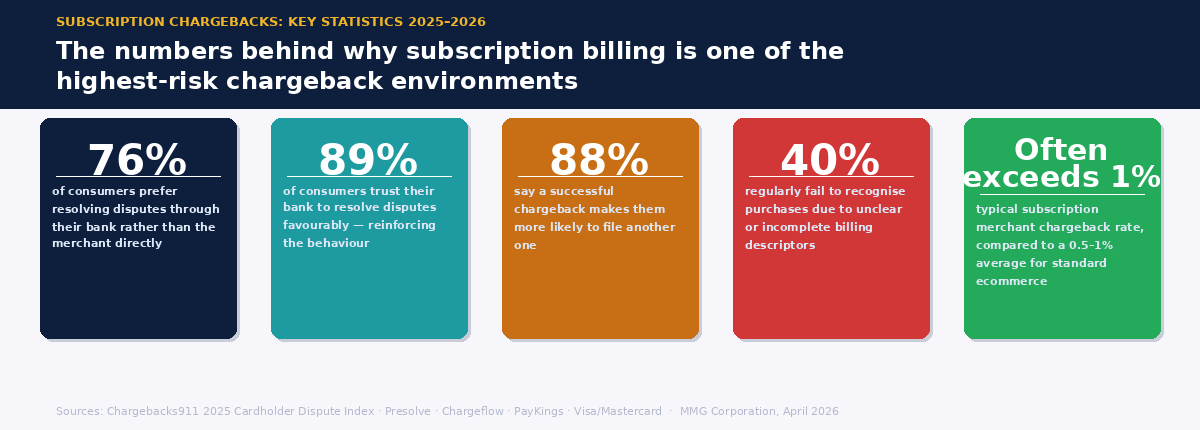

This is not an edge case. According to Chargebacks911's 2025 Cardholder Dispute Index — based on surveys of over 1,200 cardholders across the US and UK — 76% of consumers prefer to resolve payment disputes through their bank rather than contacting the merchant directly. Nearly half admit bypassing the merchant entirely. And 89% trust their bank to resolve disputes in their favor, with 88% saying a successful dispute makes them more likely to file another one.

The system designed to protect consumers from genuine fraud has become the default cancellation method for a significant portion of subscription customers. For merchants operating in high-risk verticals — iGaming, adult entertainment, nutraceuticals, online lending, travel — where chargeback ratios are already under scrutiny, this behavioral shift has material consequences.

Why Customers Reach for the Bank Instead of the Cancel Button

Understanding the behavior requires looking at it from the customer's perspective — which is rarely as calculating as it might appear. Most subscription chargebacks are not driven by deliberate fraud. They are driven by a combination of friction, confusion, and the path of least resistance.

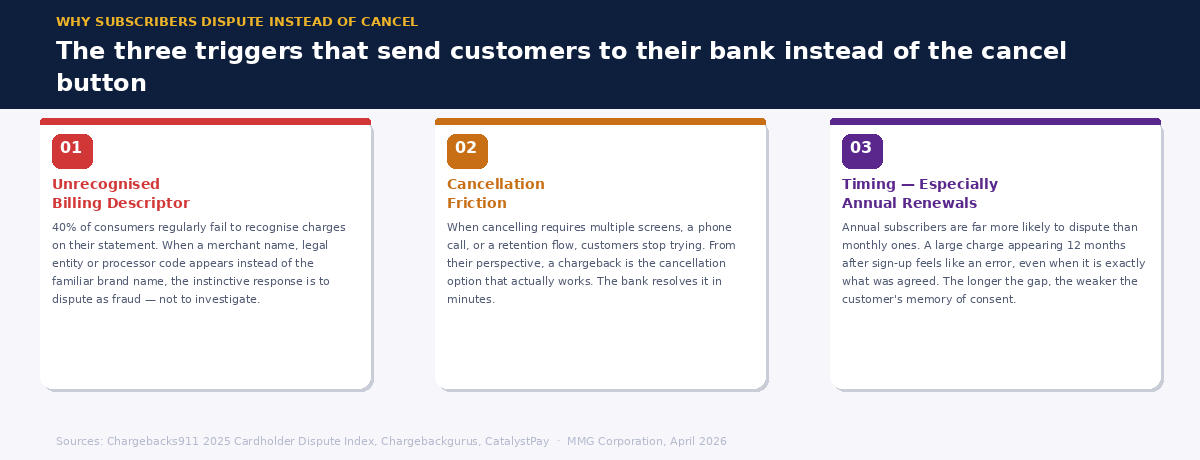

The single most common trigger is a charge the customer does not recognize. Chargeflows 2025 data shows that 40% of consumers regularly fail to recognize purchases on their statement due to unclear or incomplete billing descriptors. When a recurring charge appears under a legal entity name, a payment processor identifier, or an abbreviation that bears no resemblance to the product the customer signed up for, the instinctive response is to dispute it as fraudulent — not to investigate it.

The second major trigger is cancellation friction. When customers cannot cancel easily — when the process requires navigating through multiple screens, calling a support line, or sitting through a retention flow — many simply stop trying. From their perspective, a chargeback is the cancellation option that actually works. As one industry source put it directly: "If cancelling a subscription isn't just as easy to end as it was to sign up, people won't even try. They'll just hit 'dispute' in their banking app."

The third trigger is timing. Annual subscriptions are particularly vulnerable. A customer who signed up twelve months ago and has not used the service in six is far more likely to dispute a renewal charge than a monthly subscriber who has been receiving regular reminders. The psychology is different: a large, unexpected annual charge feels like an error — even when it is exactly what was agreed. Industry data consistently shows that annual renewals generate disproportionately high dispute volumes relative to their share of total billing cycles.

The Cost Is Larger Than the Chargeback Fee

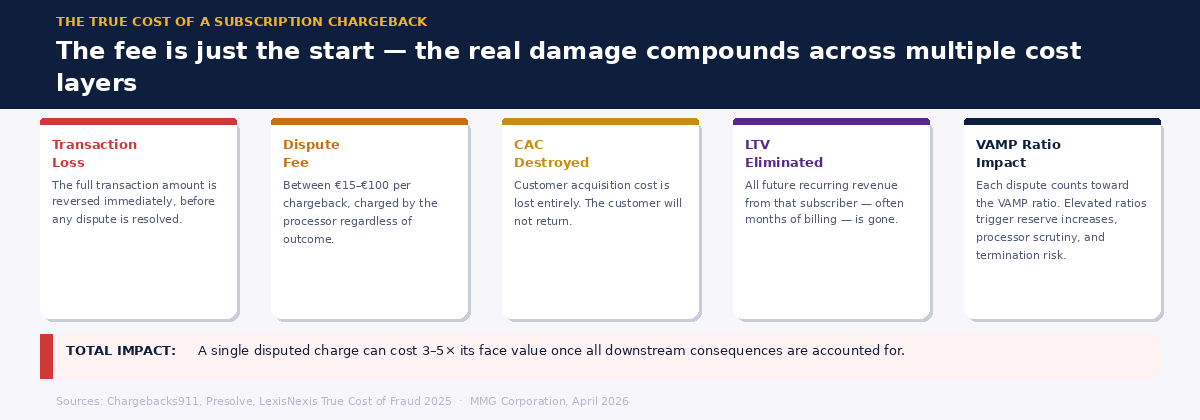

Merchants typically account for the direct cost of a chargeback: the transaction amount, the dispute fee (typically between €15 and €100 depending on the processor and risk profile), and the operational time spent gathering evidence and responding. These are real costs, but they understate the full picture significantly.

For subscription businesses, every chargeback represents the destruction of future lifetime value. A customer who files a dispute will not return. They will be placed on internal blacklists. The customer acquisition cost — paid to attract them in the first place — is lost entirely. And where the chargeback pushes a merchant's ratio toward card network monitoring thresholds, the downstream consequences extend to the entire merchant account: higher reserve requirements, processor scrutiny, and in extreme cases, termination.

Under Visa's VAMP program — which came into force in April 2025 — subscription businesses face particular exposure. VAMP combines fraud alerts (TC40) and disputes (TC15) into a single ratio. Subscription merchants, who already tend to run higher dispute rates than one-time purchase merchants, find themselves structurally closer to the monitoring thresholds simply because of their business model. The April 2026 threshold updates have made this more acute.

What the Regulation Environment Is Adding

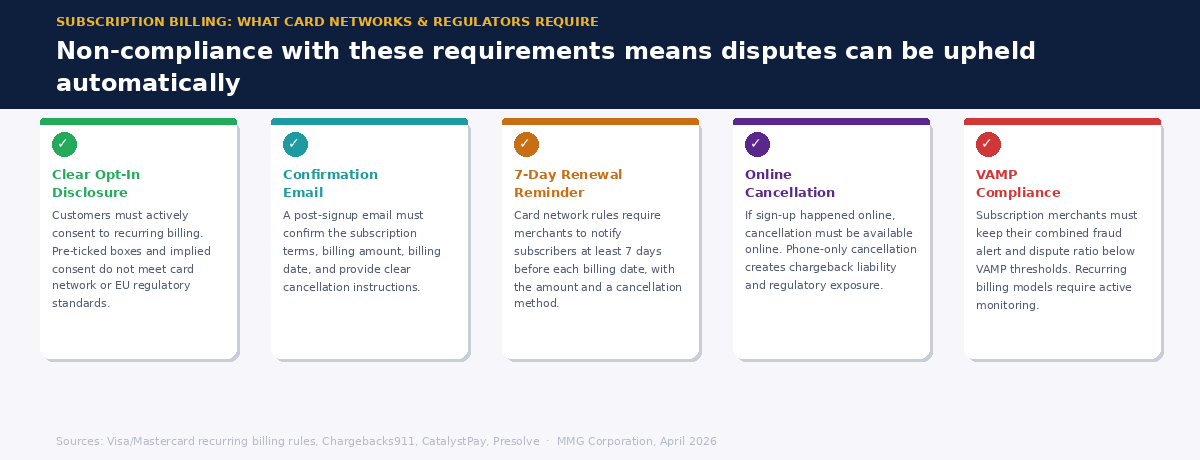

The behavioral shift among consumers is happening at the same time as regulatory pressure on subscription billing practices is increasing across the board. Card network rules already require merchants offering subscriptions or trial-to-paid programs to provide clear opt-in disclosures, confirmation emails with cancellation instructions, and renewal reminders at least seven days before the next billing date. Non-compliance with these requirements does not just create chargeback risk — it creates grounds for the dispute to be upheld automatically.

In the EU, consumer protection frameworks are tightening further. New rules on subscription transparency and auto-renewal disclosures are expected to come into force during 2026, requiring merchants to make cancellation processes clearly accessible online. The principle is consistent across markets: if the sign-up happened online, the cancellation must be available online too. Merchants who rely on friction as a retention tool are building a chargeback pipeline, not a loyal customer base.

Practical Steps That Change the Outcome

The encouraging part of the data is that most subscription chargebacks are preventable. They are not the result of determined fraudsters — they are the result of customers who could not recognize a charge, could not find a way to cancel, or were not given a timely reason to engage before filing a dispute. Addressing those failure points directly reduces chargeback volume without requiring merchants to give up their subscription model or their revenue.

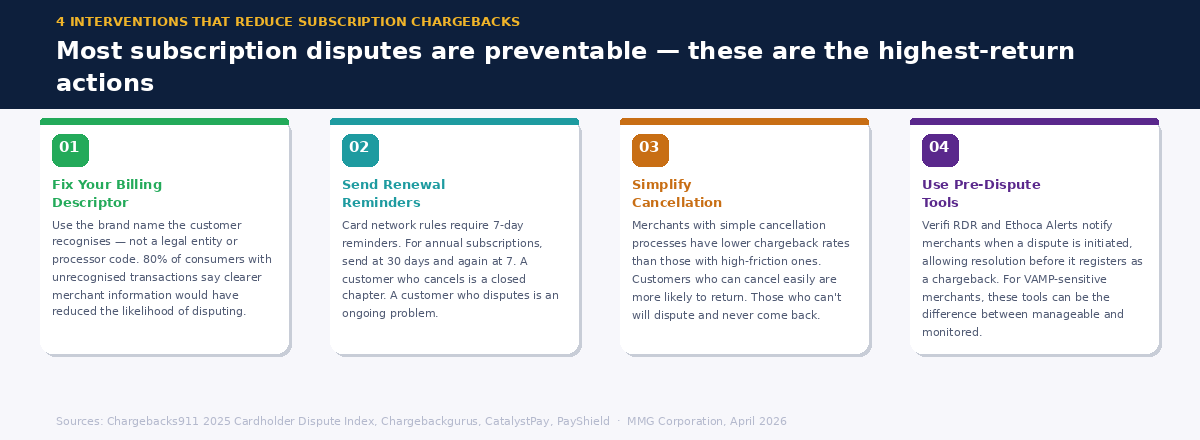

Fix your billing descriptor first. This is the single highest-return intervention available. A descriptor that clearly shows the brand name the customer recognizes — not a legal entity or processor code — can eliminate a significant proportion of "unrecognized transaction" disputes before they are filed. The 2025 data shows that 80% of consumers with unrecognized transactions say clearer merchant information would have reduced their likelihood of disputing.

Send renewal reminders as a matter of policy. Card network rules require seven-day reminders for recurring billing. Treat this as a floor, not a ceiling. For annual subscriptions in particular, a reminder at 30 days and again at 7 days gives customers the window to cancel — and removes their justification for disputing after the fact. A customer who cancels is a closed chapter. A customer who disputes is an ongoing operational problem.

Make cancellation genuinely easy. This feels counterintuitive for businesses focused on retention, but the evidence is consistent: merchants with simple cancellation processes have lower chargeback rates than those with high-friction ones. Customers who can cancel easily are also more likely to return. Customers who had to fight to cancel are gone permanently and will dispute on the way out.

Use pre-dispute tools to intercept disputes before they become chargebacks. Services like Verifi RDR and Ethoca Alerts notify merchants when a dispute is initiated, allowing them to resolve it — typically by issuing a refund — before it registers as a chargeback against the VAMP ratio. For subscription merchants already managing tight chargeback ratios, these tools can make the difference between a manageable dispute volume and a monitoring program.

The Acquirer Relationship Dimension

For high-risk merchants, subscription chargeback management is not just an internal operational matter — it is a factor in the stability of the acquirer relationship. Acquirers monitoring VAMP ratios across their portfolio will identify subscription merchants with elevated dispute rates early. The merchants who are easiest to retain are those who can demonstrate active management of the issue: clear billing descriptors, documented renewal communication, accessible cancellation flows, and pre-dispute tools in place.

A merchant who understands their chargeback drivers and can show they are addressing them systematically is a different conversation from one who presents a problem without a plan. In an environment where high-risk acquiring relationships are increasingly difficult to establish and maintain, that difference matters.

The data is clear on where the problem starts: customers are not calling to cancel because they feel the bank is a faster, easier route. The solution is not to make cancellation harder — it is to make the merchant easier to deal with than the bank. That is achievable. And for subscription businesses operating in high-risk verticals, the cost of not achieving it is one that compounds with every billing cycle.

MMGCorporation provides specialist acquiring for high-risk merchants — including those running subscription models. If you're looking for an acquirer who understands the dynamics of recurring billing and the compliance pressures that come with it, we'd be glad to talk.