Debanking, Financial Censorship, and What High-Risk Merchants Need to Know

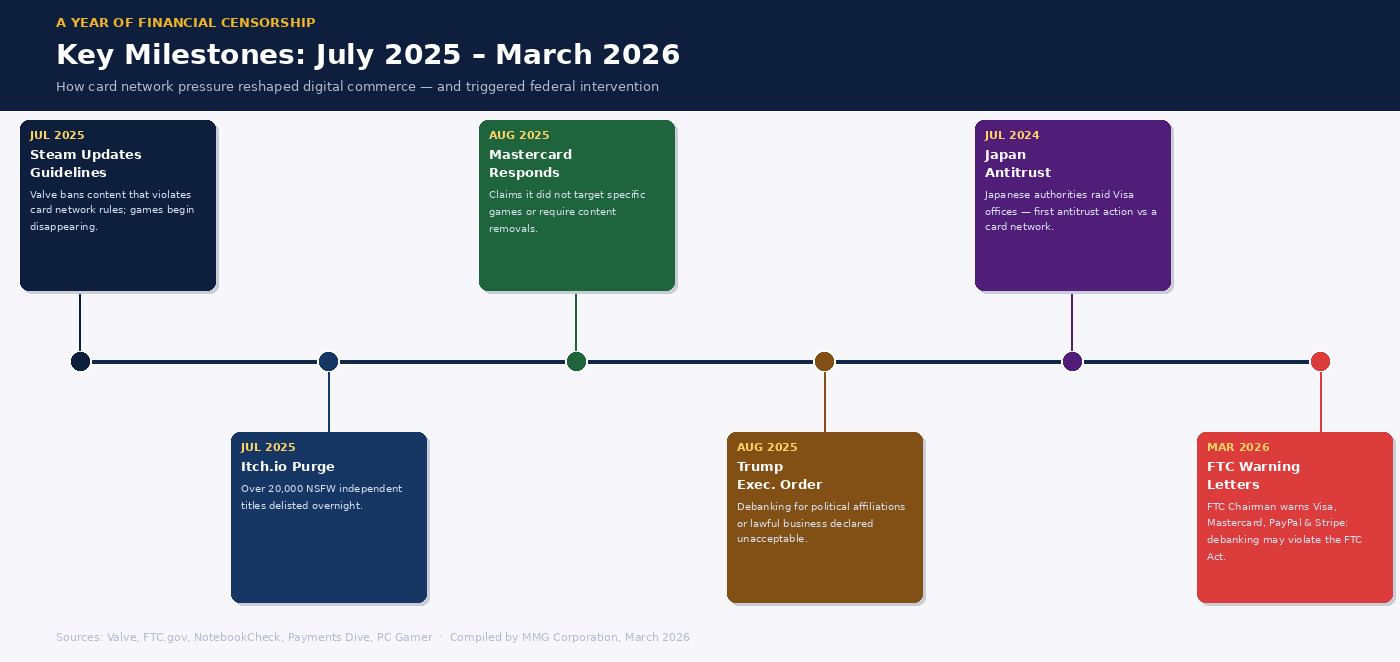

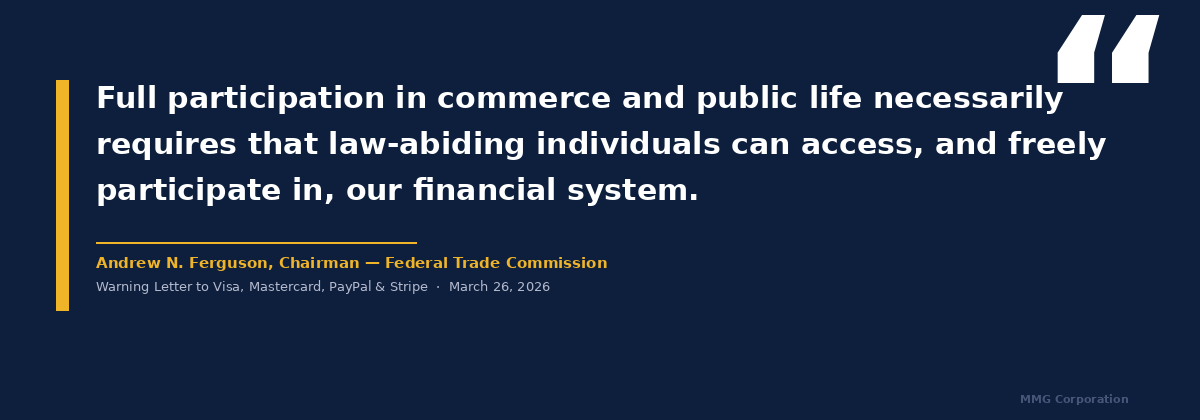

On March 26, 2026, FTC Chairman Andrew N. Ferguson sent formal warning letters to the CEOs of Visa, Mastercard, PayPal, and Stripe. The message was unusually direct for a regulatory body: denying law-abiding businesses access to financial services — regardless of the industry they operate in — may violate federal law, and the FTC is prepared to act.

For most merchants, this was background noise. For high-risk merchants — those in industries like gaming, adult entertainment, travel, nutraceuticals, CBD, or online lending — it was something closer to a lifeline. Because the problem the FTC was describing isn't hypothetical. It's been playing out, quietly and relentlessly, for years.

Let's walk through what's actually happening, why it matters, and what merchants can do about it.

The Slow Squeeze on High-Risk Merchants

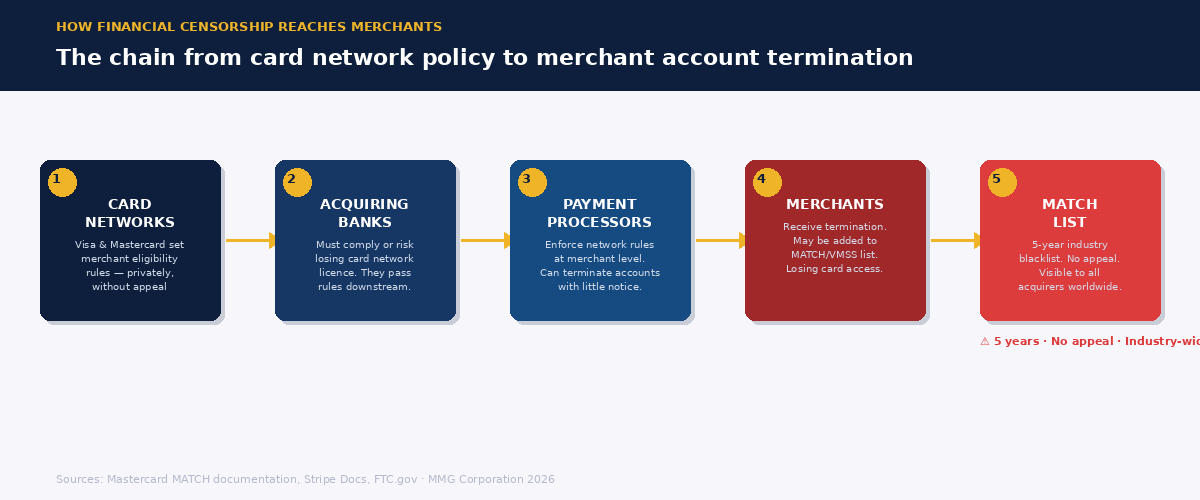

To understand the FTC action, you need to understand what's been building underneath it. Card networks — primarily Visa and Mastercard — don't process payments directly. They set the rules that acquiring banks and payment processors must follow. Those rules include which merchant categories are acceptable and which are not. And over the past decade, the list of "not acceptable" has been growing.

It started with clearly illegal content, which few would dispute. But the pressure has since expanded into territory that is entirely lawful. Adult entertainment platforms, certain gaming operators, firearms retailers, CBD businesses, online pharmacies, and politically contentious organizations have all found themselves cut off — not because they broke any law, but because their acquirer decided the reputational or compliance risk wasn't worth it. Or because an activist group wrote the right letters to the right executives at Visa or Mastercard.

The Steam episode from July 2025 illustrated this dynamic in unusually public fashion. Valve — the company behind the world's largest PC gaming platform — was pressured by card networks to remove games flagged as potentially non-compliant. Valve's own statement made the stakes clear: if it lost payment processing access, customers wouldn't be able to buy anything on Steam at all. Not just the flagged games. Everything. That's the leverage card networks hold, and it explains why even large platforms comply rather than fight.

The MATCH List: When "High-Risk" Becomes a Permanent Label

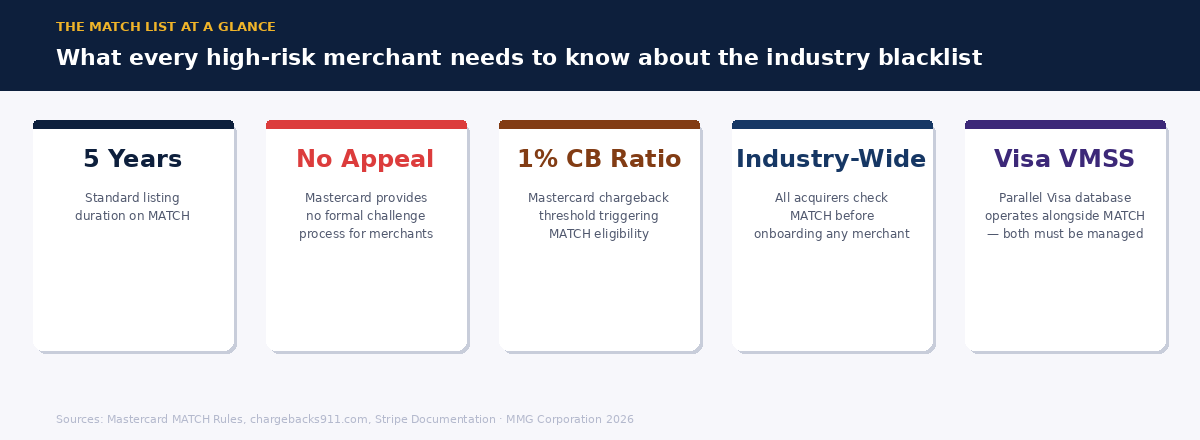

For high-risk merchants, the stakes don't stop at a single account termination. Mastercard maintains a database called the MATCH list — the Member Alert to Control High-Risk Merchants. When an acquiring bank terminates a merchant account for certain violations, it is required to add that merchant to the list within one business day. Once you're on it, almost every other acquirer in the industry can see it, and most will refuse to onboard you.

A MATCH listing typically lasts five years. During that window, the business loses access to standard card processing. It may find a specialist high-risk processor willing to take it on — but at significantly higher fees, stricter reserves, and more punishing contract terms. In extreme cases, the merchant loses card acceptance entirely, which for an online business is effectively a shutdown.

What makes this especially difficult is that the MATCH system has no formal appeal process. Mastercard defers entirely to the acquiring bank that placed the listing. If a merchant believes it was added unfairly, there is no official route to challenge that decision through the card network itself. The only path is through legal action or negotiating directly with the bank — a process that is slow, expensive, and rarely conclusive.

Equally important is Visa's equivalent system, the VMSS — Visa Merchant Screening Service — which operates as a parallel terminated merchant file. A merchant flagged by one network is often flagged by both.

What the FTC Warning Actually Says — and What It Doesn't

The FTC letters of March 26 were framed around "debanking" — a term that has gained traction in US political discourse to describe the denial of financial services based on political or religious views. Chairman Ferguson cited President Trump's August 2025 executive order on the subject and pointed to specific cases reported in the press where payment providers had closed accounts for reasons that appeared ideologically motivated.

It's worth being precise about what the letters say. They are not a ban on card networks maintaining content policies. They are a warning that any practice which denies customers access to financial services in ways that are inconsistent with the companies' own stated terms — or with customers' reasonable expectations — may constitute an unfair or deceptive act under Section 5 of the FTC Act. If that threshold is crossed, the FTC has indicated it will investigate and potentially take enforcement action.

This is a meaningful distinction. The FTC is not telling Visa and Mastercard they must process every transaction for every business. It is telling them they cannot apply their rules selectively, secretly, or in ways that contradict their own policies. For high-risk merchants who have been terminated without clear explanation or due process, that framing opens a door that didn't exist before.

What This Means for High-Risk Merchants Right Now

Regulatory signals like this rarely translate into overnight change. Card networks have large legal teams and well-established positions, and the FTC's letters are the beginning of a conversation, not the end of one. But the direction is clear, and for merchants in high-risk industries, there are practical steps that make sense regardless of how the regulatory landscape ultimately shifts.

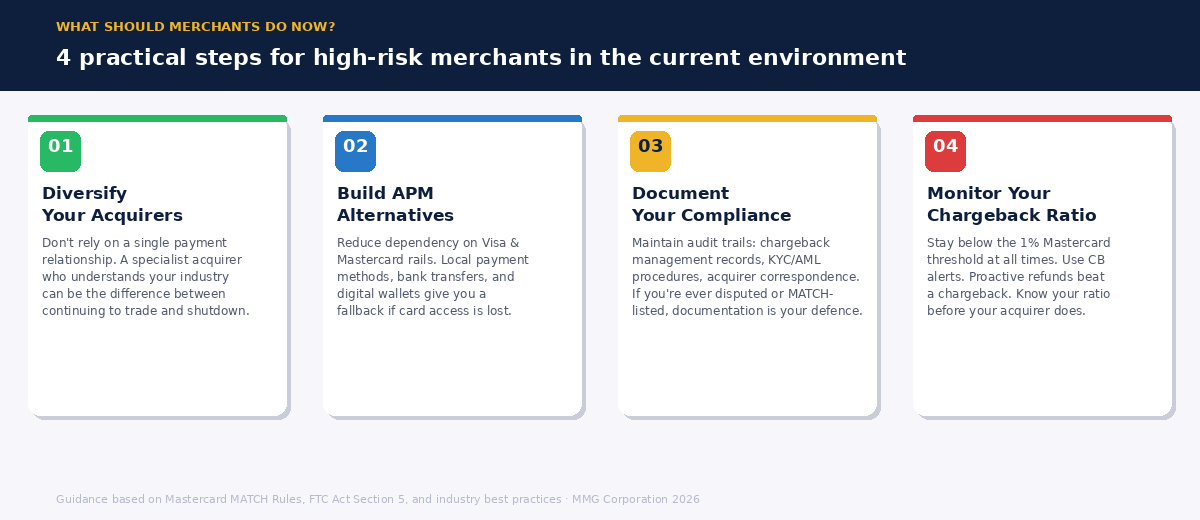

Acquirer diversification is not optional. Relying on a single acquiring relationship is one of the highest operational risks a high-risk merchant can carry. When that relationship ends — often without advance notice — the business has no fallback. Working with a specialist acquirer who understands your industry and has experience maintaining stable relationships in high-risk categories is the first and most important line of defense.

Alternative payment methods reduce card network dependency. Local payment rails, bank transfers, digital wallets, and in some markets stablecoins all represent ways to serve customers that don't run through the Visa/Mastercard network. Building these into your checkout doesn't eliminate card processing risk, but it means a card network decision doesn't take your entire payment infrastructure offline at once.

Documentation and compliance records matter more than ever. If the FTC's framing gains traction — that terminations must be consistent with stated terms and reasonable expectations — merchants who can demonstrate a clean compliance record, clear chargeback management practices, and documented communication with their acquirer are in a much stronger position to contest unfair decisions. Treat your compliance posture as the business asset it is.

Know your chargeback ratio at all times. The MATCH list threshold is a chargeback ratio above 1% on Mastercard transactions. For high-risk merchants, operating close to that line without active monitoring is playing with fire. Chargeback alerts, proactive refund policies, and clear customer communication are not just good practice — they are the most direct tool available to stay out of the terminated merchant file in the first place.

What's unfolding right now is a genuine tension between two competing ideas of how financial infrastructure should work. On one side, card networks argue that they have a responsibility to manage risk and protect their brands — and that setting standards for the merchants who use their rails is simply part of that. On the other side, regulators, legal scholars, and a growing number of merchants argue that when two companies control the vast majority of card payments globally, their decisions about who gets access are not really private business choices. They are effectively policy.

That argument is gaining regulatory traction in the US, in Japan — where antitrust authorities raided Visa's offices in 2024 over similar concerns — and increasingly in Europe, where payment regulation continues to evolve toward greater merchant protections.

The FTC's March 2026 action is a data point in that larger trend. It doesn't resolve the tension. But it does signal that the era of card networks operating as unchecked arbiters of who gets to participate in digital commerce may be ending — and that for high-risk merchants who have long operated in that shadow, the landscape is beginning, slowly, to change.

Working in a High-Risk Industry?

MMG specialises in payment solutions for merchants that standard processors turn away.

We understand the regulatory landscape, the chargeback dynamics, and the acquirer relationships that make processing stable for complex businesses.