Visa's new monitoring program is tightening the screws on fraud and disputes — and high-risk merchants are feeling it first

If you process card payments in a high-risk industry — iGaming, adult entertainment, travel, nutraceuticals, online lending, or any other verticals that standard banks treat with suspicion — there is a significant change you need to understand right now. It came into force in April 2025, enforcement started in October, and it tightened again in January 2026. It's called VAMP: the Visa Acquirer Monitoring Program.

Most merchants haven't heard of it. That's a problem, because VAMP doesn't just affect how Visa monitors your acquirer. It affects whether your acquirer keeps you.

What VAMP Is and Why It Was Created

Before April 2025, Visa managed fraud and chargebacks through two separate programs: the Visa Fraud Monitoring Program (VFMP) and the Visa Dispute Monitoring Program (VDMP). Each tracked different metrics, had different thresholds, and triggered different remediation processes. The result was a patchwork system that was difficult to navigate and, in Visa's own assessment, not keeping pace with modern fraud patterns.

VAMP replaced both. It consolidated five existing programs and 38 separate remediation processes into a single unified framework. The new program tracks a combined ratio of fraud reports and disputes against total settled transactions — and it does so primarily at the acquirer level, not the merchant level. That last detail is the part that changes everything for high-risk merchants.

Why the Acquirer-Level Model Matters to You

Under the old system, Visa monitored merchants directly. If your fraud or chargeback ratio exceeded a threshold, Visa would flag your account and your acquirer would have to respond. The problem was yours to fix.

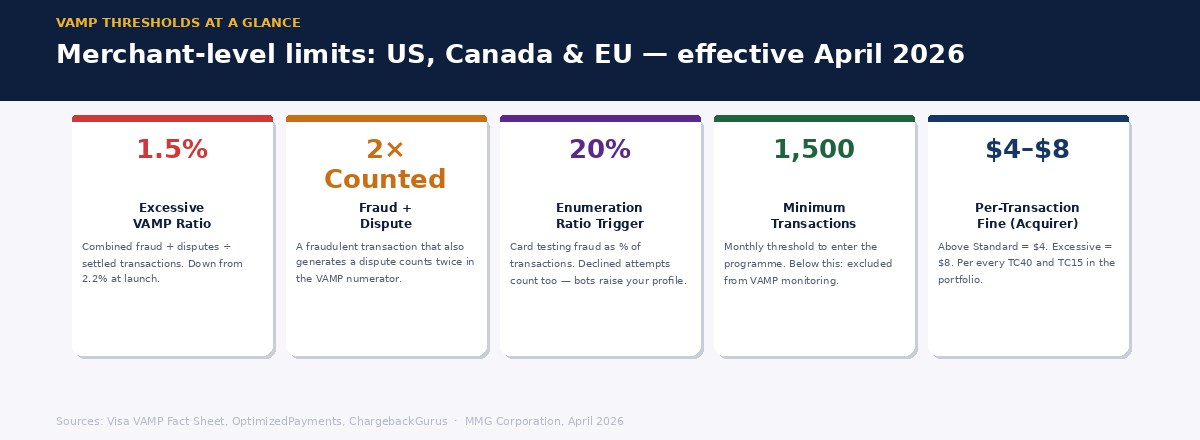

Under VAMP, Visa monitors the acquirer's entire portfolio. Your dispute activity contributes to a combined ratio across all of that bank's merchants. If the portfolio ratio exceeds Visa's thresholds, the acquirer faces penalties — and those penalties are per transaction. At the "Above Standard" level, that's $4 per fraud report and dispute. At the "Excessive" level, it's $8. For a bank processing millions of transactions a month, that adds up fast.

The consequence for merchants is straightforward: acquirers are now highly motivated to manage their portfolio risk proactively. That means they will not wait for Visa to flag you. If your metrics are trending in the wrong direction, your acquirer may tighten your reserve terms, reduce your processing limits, or terminate your account — before you've technically exceeded any of Visa's own thresholds. They're protecting themselves. Your clean record doesn't fully protect you if it's dragging their numbers up.

For high-risk merchants, who already operate closer to the edge of acceptable ratios by definition, this dynamic is particularly acute. You are more likely to be the account an acquirer decides to remove when they need to bring their portfolio ratios down.

The Numbers You Need to Know

The VAMP ratio is calculated as the combined count of fraud reports (TC40 data) and disputes, divided by total settled transactions. One important nuance: a single fraudulent transaction that results in both a fraud report and a dispute is effectively counted twice in the numerator. This means most merchants see significantly higher VAMP ratios than they would expect based on their chargeback rate alone.

The current thresholds for merchants in the US, Canada, and EU are: "Excessive" begins at a 1.5% VAMP ratio as of April 2026, down from 2.2% in the programs early phase. (Other regions may remain at 2.2% until later phases — check with your acquirer if you operate outside these markets.) Merchants below 1,500 applicable transactions per month are excluded from the program entirely. There is also a separate enumeration ratio for card testing fraud — if 20% or more of your transactions are flagged as card testing attempts, that triggers its own enforcement track regardless of your overall dispute ratio.

Critically, declined transactions count toward your enumeration ratio. Bot attacks probing your checkout with stolen card numbers raise your profile with Visa even if every attempt is declined. This is new territory for many merchants, who have historically focused only on approved transaction chargebacks.

Rolling Reserves: The Other Pressure Point

VAMP doesn't operate in isolation. For high-risk merchants, it sits alongside the reserve structures that acquirers use to manage their exposure — and VAMP is causing acquirers to reassess those structures.

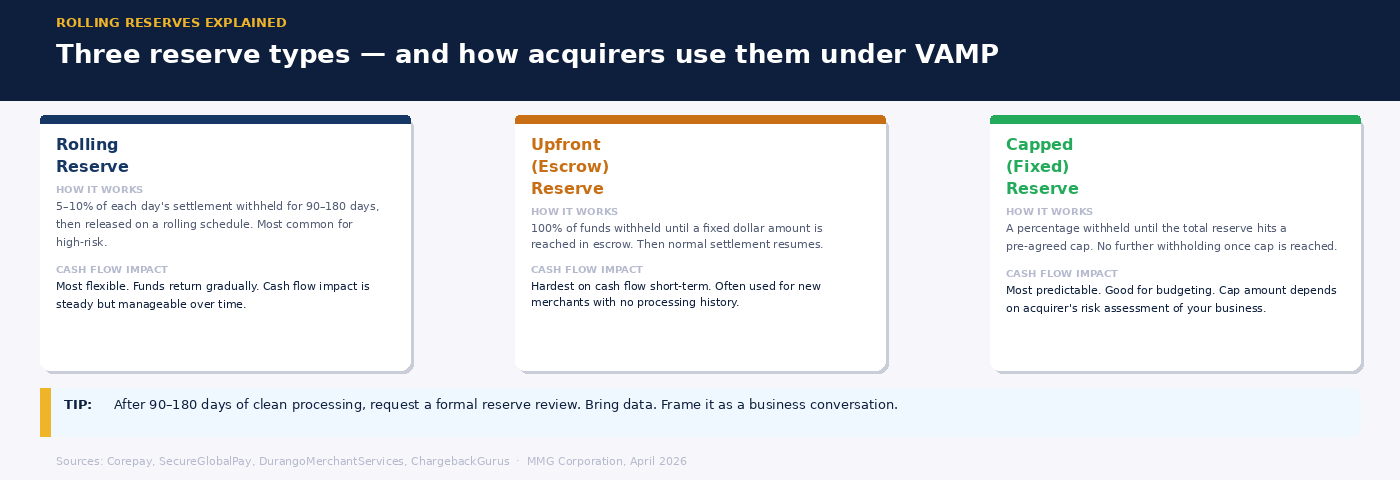

Rolling reserves — where an acquirer withholds a percentage of each day's settlement for a fixed period (typically 90 to 180 days) before releasing it — are standard practice for high-risk accounts. The typical range is 5% to 10% of processed revenue. Under VAMP, acquirers facing tighter portfolio pressure are increasingly using reserve terms as a first-response lever when a merchant's metrics deteriorate. Before terminating an account, many will increase the reserve percentage or extend the holding period as a way of building a larger buffer against potential losses.

This creates a cash flow challenge that compounds quickly. A merchant already operating on tight margins, hit by rising chargebacks and a sudden increase to a 10% rolling reserve with a 180-day hold, may find itself effectively funding its acquirer's risk management out of its own working capital. The funds do come back — but the timing mismatch can be serious for businesses with consistent high-volume processing.

The path out of elevated reserve terms is consistent, documented performance. Acquirers typically review reserve terms at 90 to 180-day intervals. Merchants who can demonstrate a stable VAMP ratio, controlled chargebacks, and no fraud flags have a genuine basis to negotiate reserve reductions. The key is treating that review as a planned event rather than waiting for the acquirer to initiate it.

What High-Risk Merchants Should Do Right Now

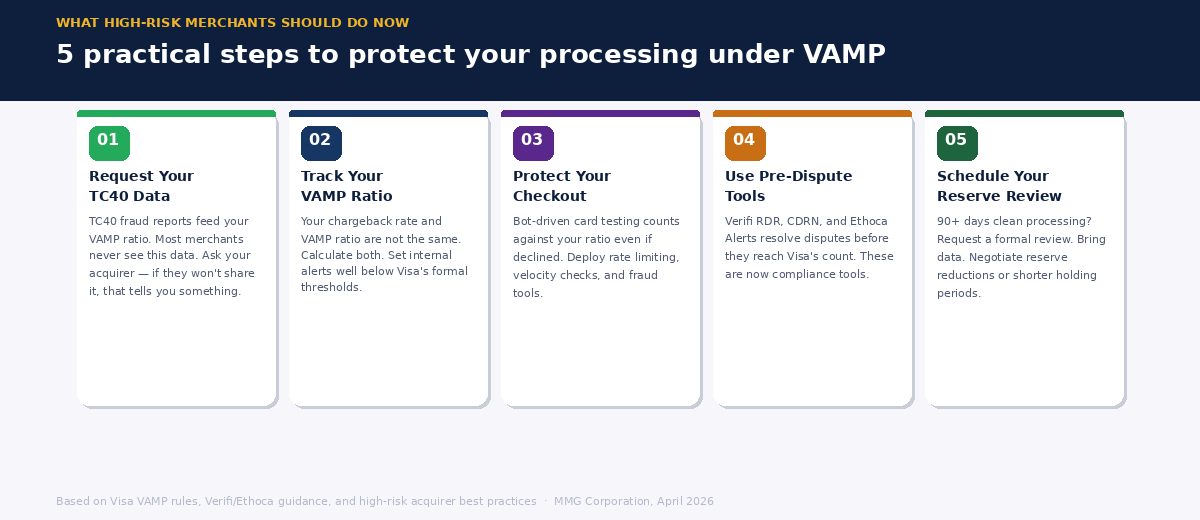

Request your TC40 data from your acquirer. TC40 is the fraud report data that feeds your VAMP ratio, and most merchants never see it directly. Without it, you're managing your risk blind. Your acquirer should be able to provide this — if they won't, that's itself useful information about the relationship.

Separate your VAMP ratio from your chargeback rate. These are not the same thing. A clean chargeback rate does not mean a clean VAMP ratio. Calculate both, and build internal thresholds that give you an early warning before you hit Visa's or your acquirer's limits.

Protect your checkout from card testing. Enumeration attacks — automated bots probing your checkout with stolen card numbers — now count against your VAMP ratio even if every attempt fails. AI-powered fraud detection, rate limiting on authorization attempts, and velocity checks at checkout are no longer optional for high-risk merchants. They're compliance infrastructure.

Use pre-dispute resolution tools. Verifi's Rapid Dispute Resolution (RDR) and Cardholder Dispute Resolution Network (CDRN), as well as Ethoca Alerts, allow disputes to be resolved before they become chargebacks and before they count toward your VAMP ratio. These tools are now among the most directly effective ways to manage your numbers under the new framework.

Schedule your reserve review. If you've been processing cleanly for 90 days or more, request a formal review with your acquirer. Bring data: your chargeback ratio, your VAMP-equivalent calculations, your fraud prevention measures. Frame it as a business conversation, not a favor. The worst outcome is that they say no. The best outcome is better terms and a stronger relationship.

VAMP is part of a broader tightening of the risk environment for high-risk merchants. Mastercard has its own equivalent monitoring under its Excessive Chargeback Program, which similarly places acquirers in the position of managing merchant portfolios rather than individual accounts. Both card networks are moving toward a model where acquirers bear greater responsibility for the merchants they board — and where acquirers respond to that responsibility by becoming more selective, more reactive, and quicker to act.

For high-risk merchants, this means that the quality of your acquirer relationship has never been more important. An acquirer who understands your industry, monitors your account proactively, and works with you to manage metrics is a fundamentally different proposition from one who treats you as a line item in a risk spreadsheet. In a VAMP world, the difference between those two relationships can determine whether you process payments next quarter or not.

The rules have changed. The merchants who understand the new rules — and build their processing infrastructure around them — will be the ones still operating when others have been quietly removed from the network.

MMG Corporation specializes in stable, transparent acquiring for merchants that standard processors turn away.

We understand VAMP, reserves, and the compliance requirements of complex industries. Let's talk about building a processing relationship that lasts.