Credit Cards Aren't Enough

Your checkout accepts Visa and Mastercard. Your European customers have both. And yet a significant percentage of them are leaving without buying — not because of price, not because of product, but because you didn't offer the payment method they actually trust.

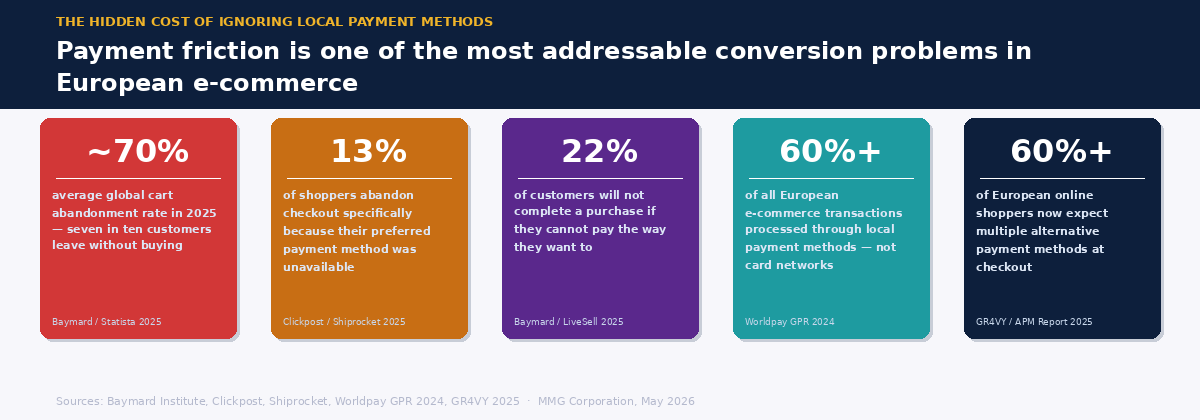

The average global cart abandonment rate sits at approximately 70%. That means seven out of ten customers who add a product to their basket and reach checkout do not complete the purchase. The reasons are many — unexpected shipping costs, forced account creation, a checkout flow with too many steps. But buried consistently in the data is a reason that surprises many merchants: 13% of shoppers abandon their cart specifically because their preferred payment method was not available. Another study puts the figure at 22% of customers who will not complete a purchase if they cannot pay the way they want to.

For merchants selling into Europe, this is not a marginal problem. It is a structural one — because Europe is a market where the payment method a consumer considers natural, familiar, and trustworthy varies enormously from country to country. And in many of those countries, a credit card is not the default.

The Myth of the Universal Credit Card

In thirty years of working in payments, I have seen this assumption repeated constantly: credit cards are universal, so accepting them is enough. It was never entirely true, and it is less true now than it has ever been.

Credit cards are widely held across Europe. But holding a card and preferring to use it online are two different things. European consumers have grown up with alternative payment methods that are faster, more familiar, and — crucially — feel safer to them than entering a sixteen-digit card number into a checkout form. These alternatives are not obscure edge cases. In several major EU markets, local payment methods account for the majority of all online transactions.

More than 60% of all European e-commerce transactions are now processed through local payment methods rather than international card networks. Over 60% of online shoppers across the continent expect multiple alternative payment methods at checkout. The merchant who offers only Visa and Mastercard is, in many markets, offering a checkout experience that the majority of their target audience does not prefer.

Trust Is the Variable Most Merchants Miss

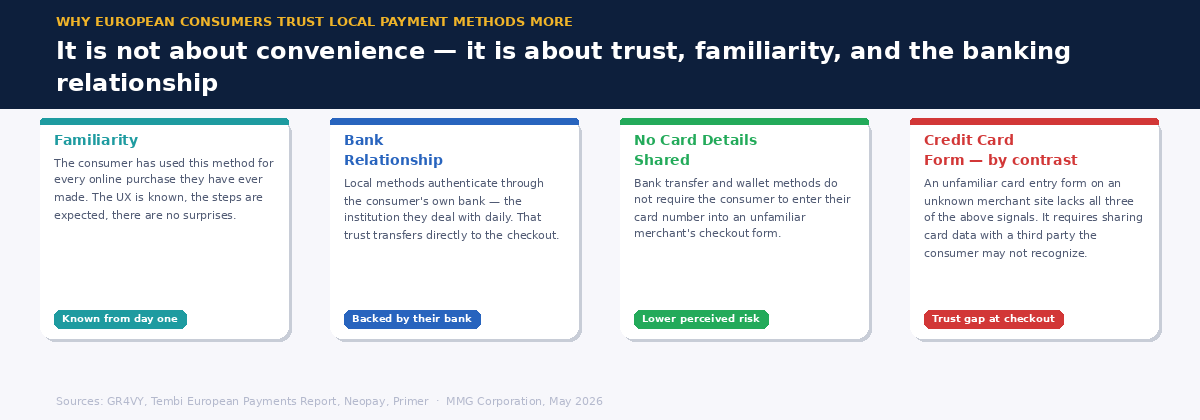

The reason European consumers prefer local payment methods is not primarily about convenience — it is about trust. Research is consistent on this point: European consumers trust local payment options and often prefer them over global ones. The word "familiar" appears repeatedly in the data, alongside "secure" and "trusted." These are not the same as convenient.

A Dutch consumer who has used iDEAL for every online purchase they have ever made does not experience a Visa card entry form as equally trustworthy. The credit card form is less familiar, requires sharing card details with a merchant they may not know, and carries no association with their own bank — the institution they deal with daily. The local payment method, by contrast, authenticates through the consumer's banking app or bank website, using credentials they have used hundreds of times. The trust is baked in.

This dynamic plays out differently in every European market, but the underlying principle is consistent: when a consumer cannot pay through the method their banking relationship is built around, the checkout experience becomes a trust problem, not just a convenience problem. And trust problems at checkout result in abandoned carts — even when the customer genuinely wants to buy.

What "Local" Actually Means — Market by Market

The European payment landscape is often described as fragmented. That description misses the point. It is not fragmented — it is localized. Each market has developed payment infrastructure around its own banking system, consumer habits, and regulatory environment. Understanding what that looks like on the ground is the starting point for building a checkout that actually converts.

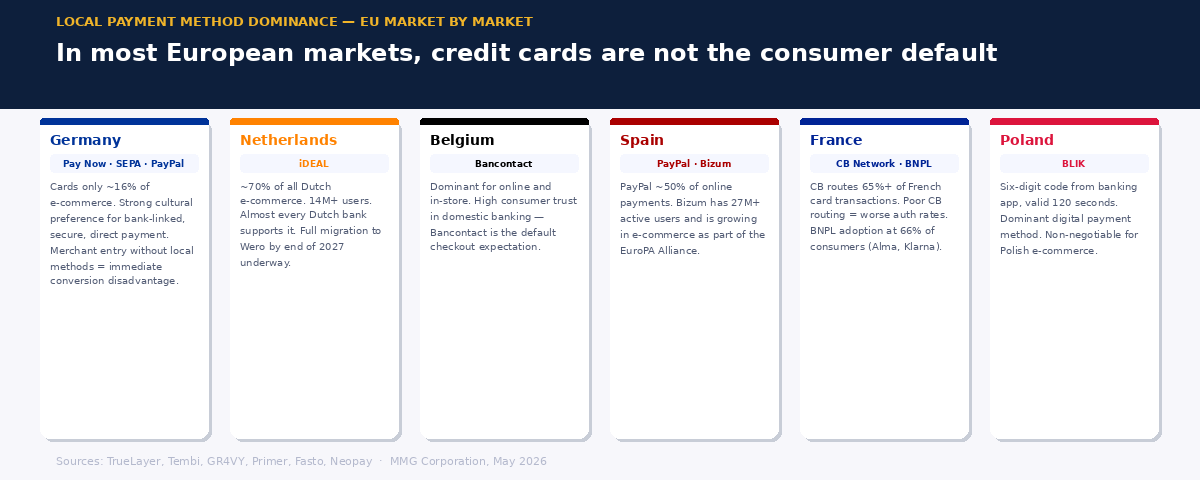

Germany is the clearest illustration of why credit card assumptions fail. Germany is the fourth largest economy in the world and the sixth largest e-commerce market globally. And yet credit cards account for only around 16% of German e-commerce transactions. German consumers strongly prefer bank-based payment options — Sofort (now rebranded as Pay Now under Klarna), SEPA direct debit, and PayPal, which is widely trusted in Germany for its buyer protection. The preference is not anti-digital — it is pro-bank, and it is rooted in a cultural preference for security and control over payment outgoings. A merchant entering Germany without offering these methods is starting at a significant conversion disadvantage.

The Netherlands is the most concentrated example in Europe. iDEAL — a direct bank transfer system — accounts for approximately 70% of all Dutch e-commerce transactions. More than 14 million Dutch consumers use it. Nearly every Dutch bank supports it. The Netherlands is also in the process of migrating fully from iDEAL to Wero by end of 2027. A merchant who does not offer iDEAL in the Netherlands today is effectively invisible to the majority of the Dutch online shopping market.

Belgium has Bancontact — the domestic debit scheme that is the leading payment method for both online and in-store purchases. Many Belgian consumers do use credit cards, but Bancontact is the default expectation at checkout. The Tembi European payment report describes the Belgian consumer as having high trust in domestic banking systems specifically — a trust that a credit card form does not activate in the same way.

Spain presents a different picture. PayPal captures approximately half of all Spanish online payments — so international methods are not absent here. But Bizum, a mobile payment solution backed by Spanish banks, has over 27 million active users and is increasingly present in e-commerce checkout flows. As Bizum expands through the EuroPA Alliance, its relevance will only grow for merchants serving Spanish consumers.

France has Cartes Bancaires — the domestic card scheme that routes over two-thirds of all French card transactions through its own network rather than Visa or Mastercard's. A French consumer paying with their co-badged CB/Visa card expects the transaction to route through CB by default. A merchant whose PSP is not set up for CB routing gets worse authorization rates, more 3DS friction, and effectively a worse checkout experience for their French customers — even though the card is being accepted. BNPL has also reached 66% consumer adoption in France, making Alma and Klarna significant conversion levers in the French market.

Poland is dominated by BLIK — a mobile payment system that generates a six-digit code from the user's banking app, valid for 120 seconds. For any merchant targeting Polish consumers online, BLIK is not optional.

The Direction of Travel

If the data above describes where European payment preferences are today, the trajectory makes the case for localization even stronger. Account-to-account payment transaction value in Europe is expected to exceed €850 billion by 2026, driven by open banking adoption and the expansion of instant payment rails. The European Payments Initiative's Wero is building cross-border interoperability between iDEAL, Bancontact, Paylib, and the Nordics' Vipps MobilePay — connecting approximately 130 million users across 13 countries.

The direction is clear: European consumers are moving toward payment methods that connect directly to their bank accounts, settle instantly, and operate without the card network intermediary. Credit cards are not disappearing — but their share of the total picture is declining, and the local methods replacing them are doing so on the back of consumer trust, not just feature competition.

Local payment methods also typically cost merchants less to accept. Transaction fees for methods like iDEAL, Bancontact, and BLIK are generally 30–70% lower than card interchange rates. The conversion argument for localization is strong. The cost argument reinforces it.

What Merchants Should Do With This

The practical implication is not that merchants need to integrate every local payment method in every market simultaneously. It is that the question "which payment methods should we offer in this market?" needs to be asked before going live — not treated as a secondary optimization after launch.

Research the market before building the checkout. Each EU market has a dominant payment preference that can be identified in advance. The Local Preferences Series on this blog covers Germany, the Netherlands, and France in detail — with Spain next. Understanding what consumers in your target market trust and expect at checkout is the starting point for building a checkout that converts.

Prioritize by market share, not by complexity. In the Netherlands, iDEAL is non-negotiable — integrate it first. In Germany, direct debit and Pay Now are the priority. In Belgium, Bancontact. In France, Cartes Bancaires routing and at least one BNPL option. Get the dominant method right before adding secondary options.

Consider payment orchestration for multi-market operations. Managing multiple local payment methods across multiple markets is operationally complex without the right infrastructure. Payment orchestration platforms allow merchants to route transactions intelligently, activate local methods through a single integration, and monitor performance across payment types. For high-risk merchants operating across several EU markets, this is increasingly the standard approach rather than an advanced one.

Factor payment localization into acquirer conversations. Not all acquirers offer the same local method coverage. A specialist acquirer with deep EU market experience will typically have better connectivity to local payment rails than a generalist processor. The payment methods available to you are partly a function of which acquirer you work with — making this part of the conversation when evaluating acquiring relationships.

The merchants who have been accepting credit cards only and wondering why European conversion rates underperform are not facing a mystery. They are facing a payment localization gap — and it is one of the most addressable conversion problems in e-commerce. The consumer is there, the intent is there, and the product is there. The checkout just isn't offering what they trust.

MMG provides specialist acquiring for high-risk merchants across EU markets. If you want to talk through your payment method mix, your coverage across specific markets, or how your acquiring setup supports local payment methods, we're glad to help.

Request Info