-What it means for your business

For years, stablecoins were something you heard about in crypto circles and largely ignored. That's changing — fast. New legislation, a surge in transaction volumes, and moves by some of the world's biggest companies mean that stablecoins are crossing from the fringes of finance into mainstream payments. Here's what's happening, why it matters, and what it could mean for you as a merchant.

First — What Actually Is a Stablecoin?

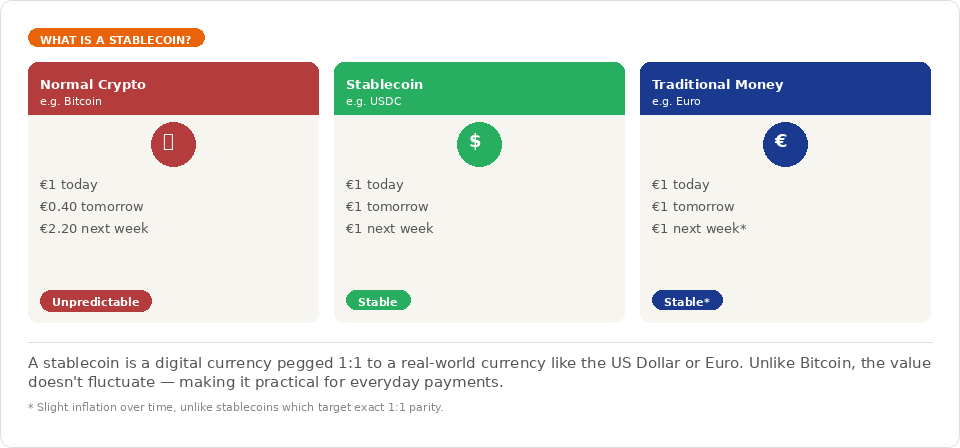

If you've never had to think about this before, that's fine. Here's the short version: a stablecoin is a digital currency that is pegged 1:1 to a real-world currency — usually the US Dollar. Unlike Bitcoin or Ethereum, the value doesn't go up and down wildly. One USDC (a popular dollar-backed stablecoin) is always worth one US Dollar. That's the whole point.

They run on blockchain infrastructure, which means transactions are fast, transparent, and can settle in seconds — but because they're tied to a real currency, they don't carry the volatility risk that has made regular cryptocurrencies impractical for everyday commerce.

Think of it this way: it's the speed and global reach of crypto, combined with the price stability of the Euro or Dollar. That combination is what's making financial institutions, payment networks, and major tech companies sit up and pay attention.

The Regulation that changed everything

The GENIUS Act — Why This Is a Turning Point

For a long time, the biggest obstacle to stablecoins going mainstream wasn't technology — it was regulation. Businesses couldn't confidently build on top of stablecoins because the legal ground was unclear. That changed last year.

On 18 July 2025, the US signed the GENIUS Act (Guiding and Establishing National Innovation for US Stablecoins) into law — the most significant piece of digital asset legislation in US history. It passed with strong bipartisan support: 68–30 in the Senate, 308–122 in the House.

The GENIUS Act does one crucial thing: it establishes a clear federal framework for who can issue stablecoins, how they must be backed, and what oversight they're subject to. Every regulated stablecoin must now be backed 1:1 with liquid assets — primarily US Dollars or short-term Treasury bonds — and issuers must prove this with monthly audited reports. The legal ambiguity that held back adoption is gone.

The impact was immediate. According to Circle — the company behind USDC, one of the largest stablecoins — daily transaction volumes jumped from $1 trillion before the Act to $4 trillion after it passed. Solana, one of the blockchains that processes stablecoin transactions, handled $650 billion in stablecoin volume in February 2026 alone — more than double its previous record.

The regulatory signal was clear: this is real money infrastructure now, not an experiment.

The Big Players Are All In

This isn't just happening in the US. Major financial institutions and technology companies across the globe are moving quickly to position themselves in the stablecoin space.

JPMorgan Chase is already offering a blockchain-based deposit token to institutional clients for global transactions. Bank of New York is providing tokenised deposits to improve collateral and margin workflows. Smaller banks are forming consortia to issue their own dollar stablecoins, aiming to compete with fintech companies for cross-border payments and small business transactions.

On the tech side, Meta is planning to integrate stablecoin payments across Facebook, Instagram, and WhatsApp in the second half of 2026 — this time partnering with a regulated third-party provider rather than trying to build its own (a lesson learned from the failed Libra/Diem project). When stablecoin payments are available natively in WhatsApp, the question for merchants will shift from "should I accept this?" to "can I afford not to?"

What Does This Actually Mean for You?

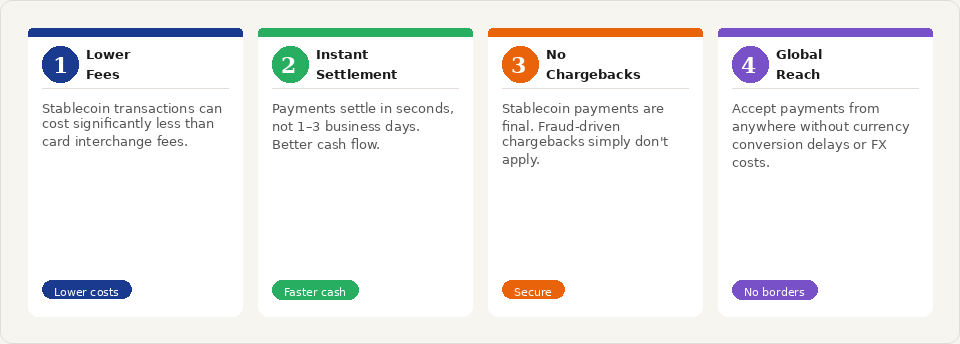

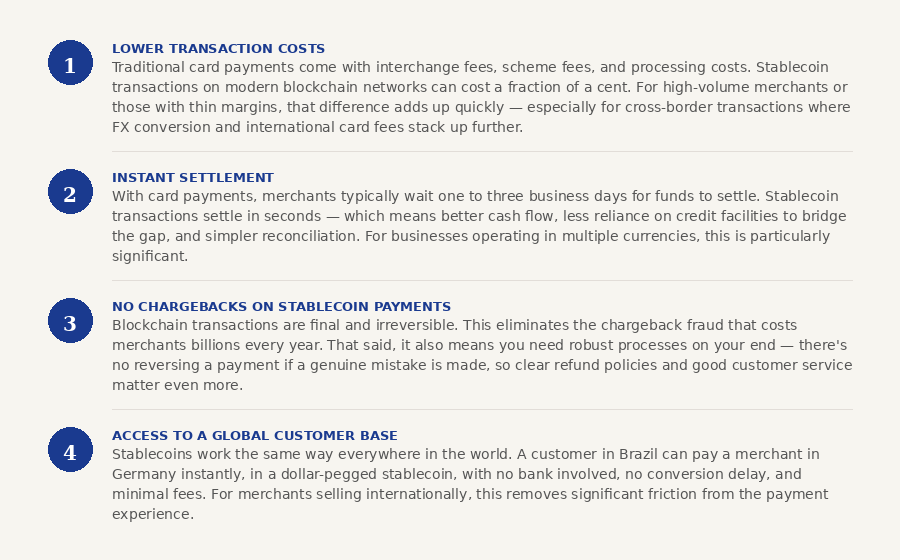

You don't need to accept stablecoins tomorrow. But understanding the genuine advantages — and the genuine complications — puts you in a much better position as this develops.

What to Watch Out For

A balanced picture means being honest about the challenges too. Stablecoins aren't a straightforward swap for card payments — at least not yet.

The GENIUS Act regulations are still being finalized. Final rules are due by July 2026, with the Act fully taking effect in January 2027. This means the landscape is still shifting, and some details — including how tax reporting works, which stablecoins will be compliant, and how dispute resolution will function — are still being worked out. Moving carefully and staying informed is the right approach for now.

There are also practical questions around customer readiness. Most consumers don't yet hold stablecoins or have wallets set up to use them. That will change as banks and apps integrate stablecoin functionality — but it means merchant adoption will likely be gradual, following consumer adoption rather than leading it.

Tax reporting is another area worth understanding. When you receive a stablecoin payment, you recognise income at the fair market value at the time of receipt. For a stablecoin pegged at $1, this is functionally identical to receiving cash — but the reporting obligation exists and the rules are evolving. If you're considering accepting stablecoins at volume, involving a tax advisor familiar with digital assets is strongly recommended.

Stablecoins have crossed a threshold. They are no longer a niche crypto product — they are becoming regulated financial infrastructure, backed by the world's largest banks and technology companies, governed by federal law, and processing trillions of dollars in transactions. The question for merchants is not whether stablecoins will become a payment option their customers expect — it's how quickly that happens, and whether they're ready when it does.

You don't need to act today. But staying informed, understanding the technology, and working with a payment partner who is watching this space closely puts you in the best position to move quickly when the time is right.

At MMG, we're tracking how stablecoin regulation evolves and what it means practically for the merchants we work with. We'll keep you updated as the GENIUS Act rules are finalised and the market develops.

Talk to the MMGCorporation team — we'll help you understand the options, the risks, and what to watch as regulation finalizes.

Learn more about MMGCorporation