Rolling Reserves: What They Are, Why Acquirers Use Them, and How to Negotiate Yours

A rolling reserve is one of the most misunderstood elements of a high-risk merchant account. Most merchants accept the terms they're offered without understanding how reserves work, how they're calculated — or that they're negotiable.

When a high-risk merchant account agreement arrives, the reserve clause is usually somewhere in the middle of a dense document. A percentage. A number of days. A note that funds will be held and released on a rolling basis. Most merchants sign without asking questions — because they need the account, and because the reserve feels like a fixed condition rather than an opening position.

That assumption is expensive. Rolling reserves affect cash flow from day one, can tie up significant working capital during a business's growth phase, and persist for months or years unless the merchant actively manages the relationship. Understanding how they work — and how acquirers actually think about them — is the foundation for negotiating terms that are fair rather than simply standard.

What a Rolling Reserve Actually Is

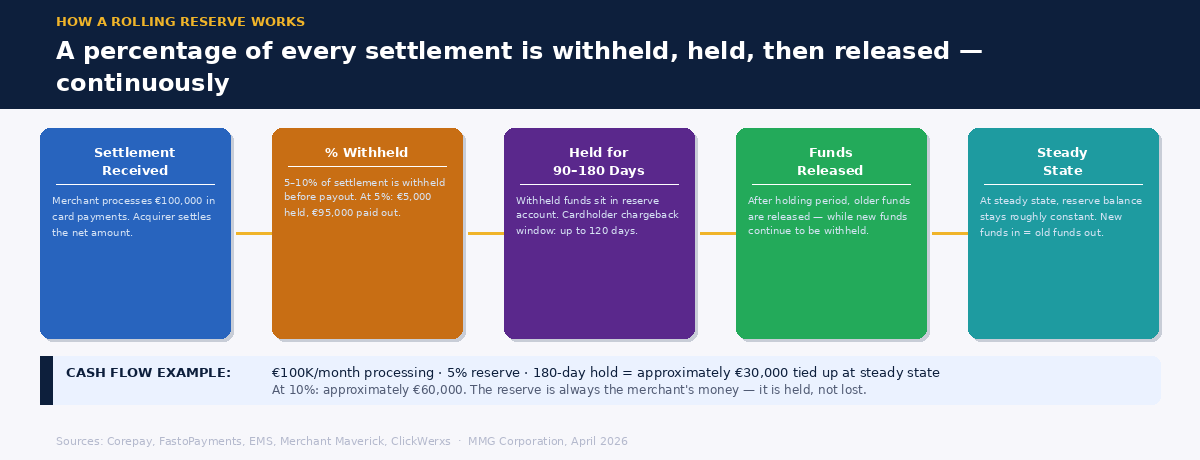

A rolling reserve is a percentage of a merchant's transaction volume that is temporarily withheld by the acquirer. It is not a fee. It is not a penalty. It is the merchant's own money, held by the acquirer as a financial buffer against potential future losses — primarily chargebacks and refunds that may occur after a payment has already been settled.

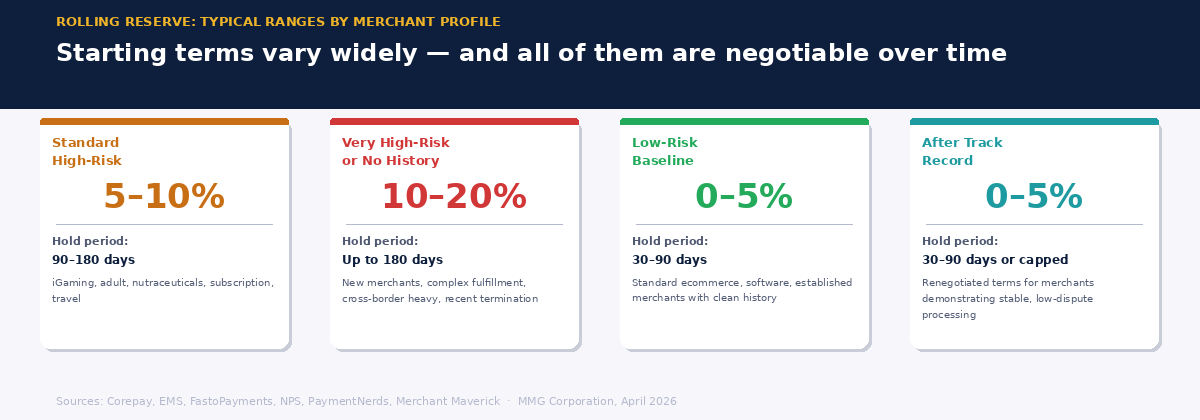

The mechanics are straightforward. A set percentage — typically 5% to 10% for most high-risk merchants, and potentially 10% to 20% for extremely high-risk verticals — is withheld from each settlement. That withheld amount is held for a defined period, usually 90 to 180 days. After that period expires, the funds are released — but new funds are being withheld continuously, so at steady state, the reserve account maintains a roughly constant balance that turns over on a rolling cycle.

The logic behind the holding period is grounded in the chargeback window. Cardholders generally have up to 120 days to dispute a transaction. By holding a percentage of settlement funds for 90 to 180 days, the acquirer ensures there are funds available to cover disputes that arrive after settlement has already occurred. Without a reserve, the acquirer would need to pursue the merchant directly to recover chargeback losses — which is operationally complex and, for merchants operating on thin margins, may not be recoverable at all.

The Three Types of Reserve

Rolling reserves are the most common structure for high-risk merchants, but they are not the only option. Understanding the alternatives matters for negotiation.

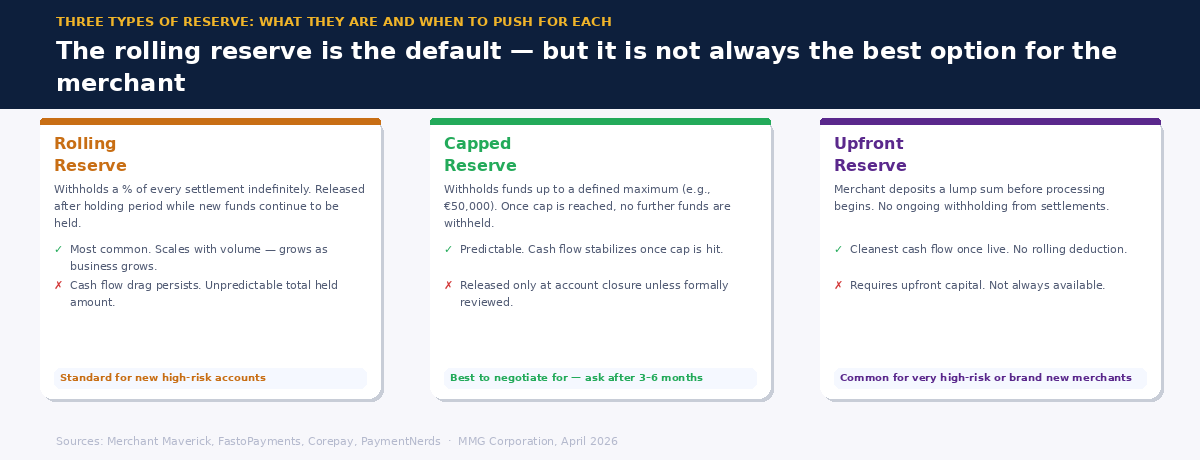

A rolling reserve withholds a percentage of every settlement indefinitely, releasing funds after the holding period expires. It is flexible and scales with volume, which makes it the default for acquirers who want ongoing coverage as the merchant's processing grows.

A capped reserve withholds funds up to a defined maximum — for example, €50,000 or the equivalent of one month's processing volume. Once the cap is reached, no further funds are withheld. The cap provides predictability: the merchant knows exactly how much capital will be tied up, and once that amount is accumulated, the drag on cash flow stops. Funds held in a capped reserve are typically released only when the account is closed or the reserve is formally reviewed and released.

An upfront reserve requires the merchant to deposit a lump sum before processing begins. This is most common for very high-risk or brand new businesses with no processing history. It eliminates the rolling drain on cash flow but requires capital availability before the account goes live.

For most high-risk merchants, the rolling reserve is the structure they will encounter. But the capped reserve is often the better outcome from a cash flow perspective — and it is frequently available to merchants who ask for it, particularly once they have established a track record.

How Acquirers Calculate Reserve Terms

Reserve terms are not arbitrary. Acquirers use a set of factors to determine both the percentage withheld and the holding period, and understanding those factors is the first step toward influencing them.

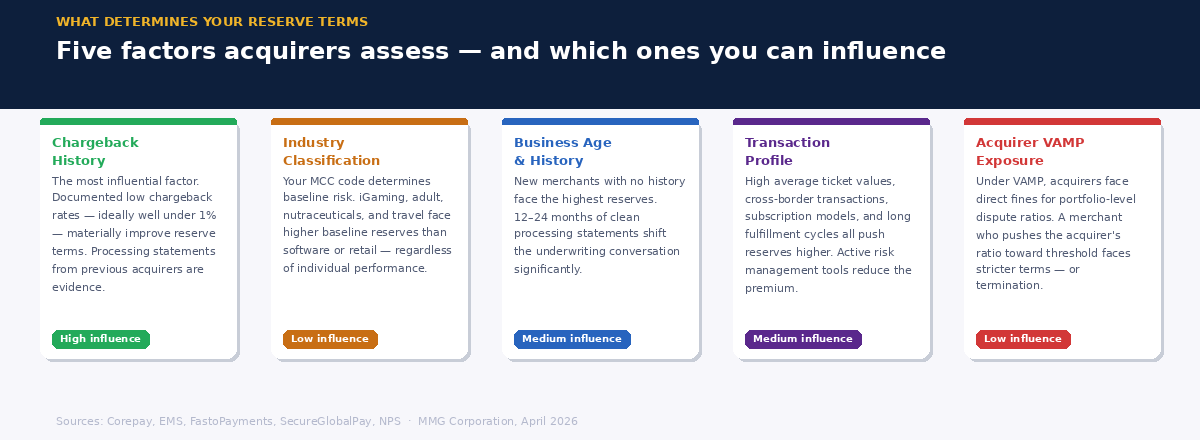

The most significant factors are chargeback history and industry classification. A merchant with a documented history of low chargebacks — ideally well under 1% — presents a materially lower risk than one with an elevated or volatile dispute rate. Industry classification matters independently: a nutraceuticals merchant may face higher reserve requirements than a software merchant processing similar volumes, simply because the industry's aggregate chargeback profile is worse.

Business age and processing history are the second major factor. A merchant with two years of clean processing history at a previous acquirer is a fundamentally different underwriting proposition from one with no history at all. Providing documented processing statements — showing volume, chargeback rates, and refund rates over a 12-to-24-month period — can significantly improve reserve terms at onboarding.

Transaction characteristics also matter. High average ticket values create larger individual chargeback exposures. Cross-border transactions carry higher fraud rates. Subscription and recurring billing models generate disputes that can arrive months after the initial transaction. All of these push reserve requirements higher. A merchant who can demonstrate active management of these risks — through pre-dispute tools, clear billing descriptors, transparent cancellation flows — can present a more favorable risk profile than the industry average suggests.

Finally, the acquirer's own regulatory environment and VAMP exposure plays a role. Under Visa's VAMP program, acquirers are held directly accountable for the aggregate fraud and dispute ratios across their merchant portfolio. A merchant whose processing profile puts pressure on the acquirers portfolio-level VAMP ratio will face stricter reserve requirements — or termination — regardless of their absolute chargeback rate.

How to Negotiate Reserve Terms

The most important thing to understand about rolling reserve negotiation is that it happens at two stages: at onboarding, before the account is live, and during the relationship, as the merchant builds a track record. Both stages offer genuine leverage — but most merchants only engage with one of them.

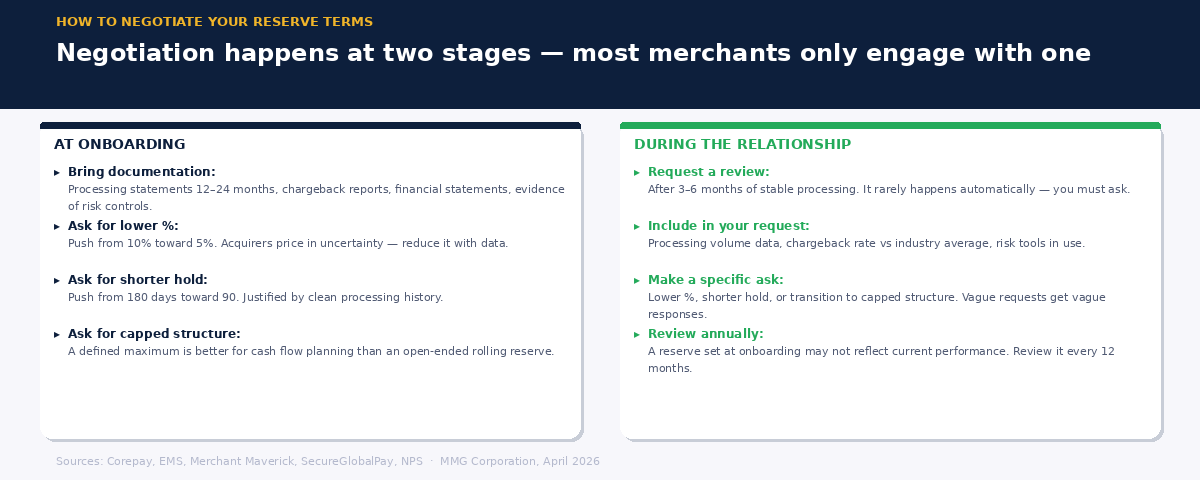

At onboarding: The initial reserve terms in an agreement are a starting position, not a final offer. Come to the conversation with documentation: processing statements from previous acquirers, chargeback reports, financial statements showing business stability, and evidence of risk management practices in place. Acquirers are underwriting a risk — a merchant who can reduce the perceived risk with evidence will get better terms than one who cannot.

Specific things worth negotiating at the outset include the percentage (pushing from 10% toward 5%), the holding period (pushing from 180 days toward 90), and the structure (pushing from rolling to capped). Not all of these will move in every case, but all of them are negotiable in principle. Asking costs nothing. Not asking locks in whatever was offered.

During the relationship: Most acquirers will review reserve terms after three to six months of stable processing. This review rarely happens automatically — the merchant needs to request it. A formal request, backed by processing data showing consistent volume, low chargeback rates, and clean fraud metrics, gives the acquirer the justification to reduce or release the reserve. Without a request, the existing terms simply persist.

The review request should include a summary of processing performance over the review period, a comparison of actual chargeback rates against the industry average, documentation of any risk management tools in use, and a specific ask — whether that is a reduction in the withholding percentage, a shorter holding period, or a transition to a capped structure.

Choosing the right acquirer in the first place: Reserve terms vary significantly between acquirers, even for identical merchant profiles. A specialist acquirer with deep experience in a specific high-risk vertical will have calibrated their reserve requirements against actual experience with that industry — and will typically offer more appropriate terms than a generalist acquirer pricing in a large uncertainty premium. The first negotiation a high-risk merchant makes is which acquirer to work with.

Managing the Cash Flow Impact

Even well-negotiated reserve terms create a cash flow drag, particularly in the early months of a new acquiring relationship. A merchant processing €100,000 per month at a 5% reserve rate with a 180-day holding period will have approximately €30,000 tied up in the reserve account at steady state. At 10%, that figure doubles. Understanding and planning for this is a practical necessity.

The cash flow impact is most acute during the growth phase. As processing volume increases, the absolute amount held in reserve increases in proportion — meaning that a merchant scaling rapidly may find their reserve balance growing faster than their available capital. This is the period when cash flow planning matters most, and when the terms negotiated at onboarding have the greatest operational consequence.

The reserve is always the merchant's money. It cannot be used by the acquirer for their own purposes, and it must be returned — either during the relationship as funds age out of the holding period, or in full when the account is closed. Keeping sight of this is useful when reserve terms feel punitive: the funds are not lost, they are delayed. The goal is to minimize that delay through active negotiation and performance management.

Rolling reserves are a standard feature of high-risk acquiring — not a punishment, and not a fixed condition. The merchants who manage them well are the ones who understand the mechanics, come prepared to negotiate, and treat the reserve review as a regular part of managing the acquirer relationship rather than a one-time event at onboarding.

MMGCorporation works with high-risk merchants across EU markets. If you want to talk through your current reserve terms, your processing setup, or what to expect when applying for a new acquiring relationship, we're glad to help.