The Smarter Way for High-Risk Merchants to Build a Resilient Processing Stack

Relying on a single payment provider is one of the biggest operational risks a high-risk merchant can carry.

Payment processing is infrastructure — something that should work quietly in the background while the business gets on with everything else. For high-risk merchants, it rarely stays that quiet. Chargeback ratios creep up. A processor flags the account. A bank changes its risk appetite. A new card network rule shifts the thresholds. And suddenly the thing that was supposed to be infrastructure is front and center, demanding attention at exactly the wrong moment.

The traditional response to this problem is to find a better processor. The smarter response is to stop depending on just one.

That's the core idea behind payment orchestration — and in 2026, it's becoming less of a premium feature and more of a practical necessity for any high-risk merchant serious about stability and growth.

What Payment Orchestration Actually Is

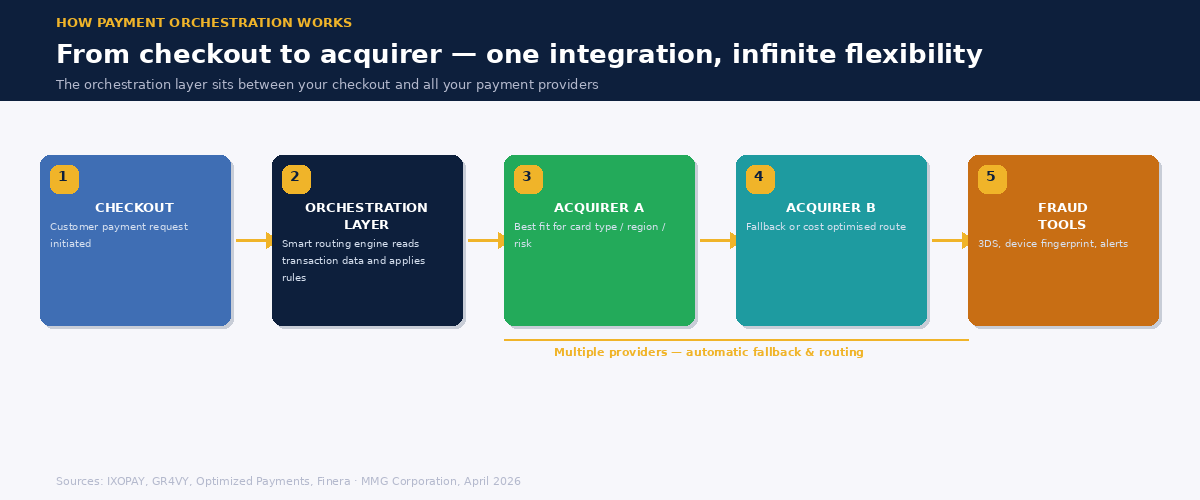

A payment orchestration platform sits as an intelligent layer between your checkout and your payment providers. Rather than routing every transaction through a single processor, it connects you to multiple acquirers, gateways, and fraud tools simultaneously — and makes real-time decisions about which route each transaction should take.

Think of it like air traffic control for your payments. Each transaction arrives with its own characteristics: the card type, the issuing country, the transaction amount, the customer's risk profile. The orchestration engine reads those characteristics, checks them against live performance data and your own business rules, and routes the payment to the provider most likely to approve it — at the best cost and with the lowest risk of a dispute.

The merchant integrates with the orchestration platform once. Everything behind that — adding new processors, adjusting routing rules, connecting fraud tools — happens without touching your checkout code. It's a single point of control over what was previously a fragmented, difficult-to-manage stack.

Why It Matters More for High-Risk Merchants

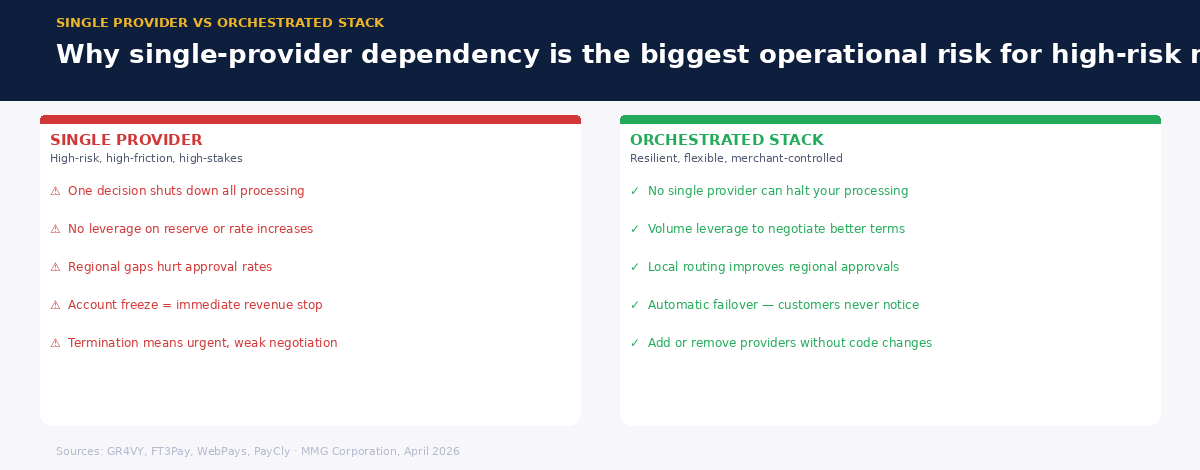

Every merchant benefits from better approval rates and lower processing costs. But for high-risk merchants, the stakes around single-provider dependency are categorically higher.

When a standard e-commerce retailer loses their processor, it's a serious problem. When a high-risk merchant loses theirs — particularly one operating in iGaming, adult entertainment, nutraceuticals, travel, or online lending — they often discover that finding a replacement quickly is extremely difficult. Their industry is flagged. Their processing history shows a recent termination. And the urgency of the situation means they're negotiating from a weak position, likely accepting worse terms than they would have under normal circumstances.

Orchestration directly addresses this vulnerability. With multiple acquirers connected through the platform, no single provider decision can take your entire payment capability offline. If one bank tightens its risk policy or changes its appetite for your industry, traffic routes automatically to another. The business keeps processing. The customer never notices.

Beyond resilience, orchestration creates something equally valuable for high-risk merchants: negotiating leverage. When your volume is concentrated with a single acquirer, you have limited power to push back on reserve increases, rate changes, or contract terms. When your platform supports multiple providers and you can credibly shift volume elsewhere, the conversation changes.

Approval Rates — The Revenue Impact You Can Measure

One of the most immediate and quantifiable benefits of orchestration is the improvement in transaction approval rates. High-risk merchants routinely see decline rates that their low-risk counterparts never encounter — not because of fraud or genuine risk, but because of blunt-instrument bank policies that apply broad category restrictions regardless of the individual transaction's merits.

Orchestration attacks this problem with intelligent routing. A transaction from a German customer that might be declined by a US-based acquirer unfamiliar with the merchant category can be automatically rerouted to a European bank with existing experience in that vertical and a higher tolerance for the associated risk profile. A subscription renewal from a known, verified customer can be separated from a new high-value transaction and sent through different paths, with different authentication requirements, optimized for each context.

The numbers behind this are meaningful. Merchants implementing orchestration with smart routing consistently report approval rate improvements of several percentage points. At meaningful transaction volumes, the revenue recovery from declined transactions that would otherwise have been lost represents a genuine return on the platform investment — often within the first few months of operation.

Chargebacks, Fraud, and VAMP — Orchestration's Role in Compliance

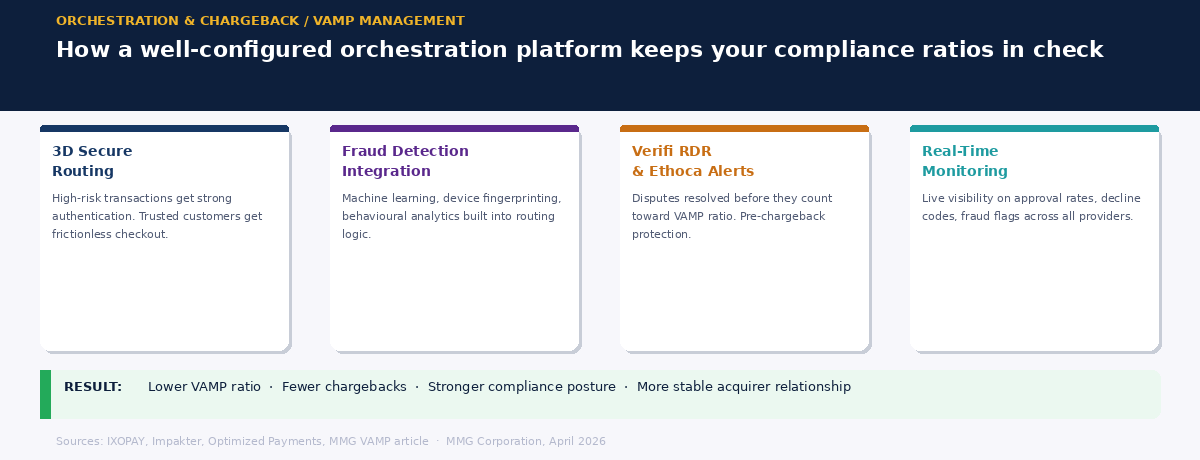

For high-risk merchants navigating the current compliance environment — particularly Visa's VAMP program and Mastercard's Excessive Chargeback Program — orchestration also plays a meaningful role in keeping ratios under control.

A well-configured orchestration platform integrates fraud detection tools directly into the routing logic. High-risk transactions are channeled through stronger authentication flows — 3D Secure, device fingerprinting, behavioral analytics — while lower-risk transactions from verified repeat customers are routed through friction less paths. This means better fraud prevention without the blunt cost of applying maximum friction to every single payment.

Pre-dispute resolution tools like Verifi RDR and Ethoca Alerts can also be connected through the orchestration layer, allowing disputes to be resolved before they register as chargebacks in your VAMP ratio. The result is a more controlled, defensible compliance posture — one that's managed actively through the platform rather than re-actively after the fact.

What to Consider Before Implementing

Payment orchestration is a powerful tool, but it works best when the underlying acquiring relationships are sound. A platform routing transactions intelligently across multiple providers is only as good as the acquirers connected to it. If those acquirers don't understand your industry, don't have experience with your chargeback dynamics, or aren't structured around your specific risk profile, the routing logic has less to work with.

This is why orchestration and specialist acquiring are complementary rather than alternatives. The orchestration layer provides the intelligence and the redundancy. The acquiring relationships underneath it provide the stability and the industry expertise. Together, they create a payment stack that can absorb pressure — from card network rule changes, from fraud spikes, from regulatory shifts — without the business grinding to a halt.

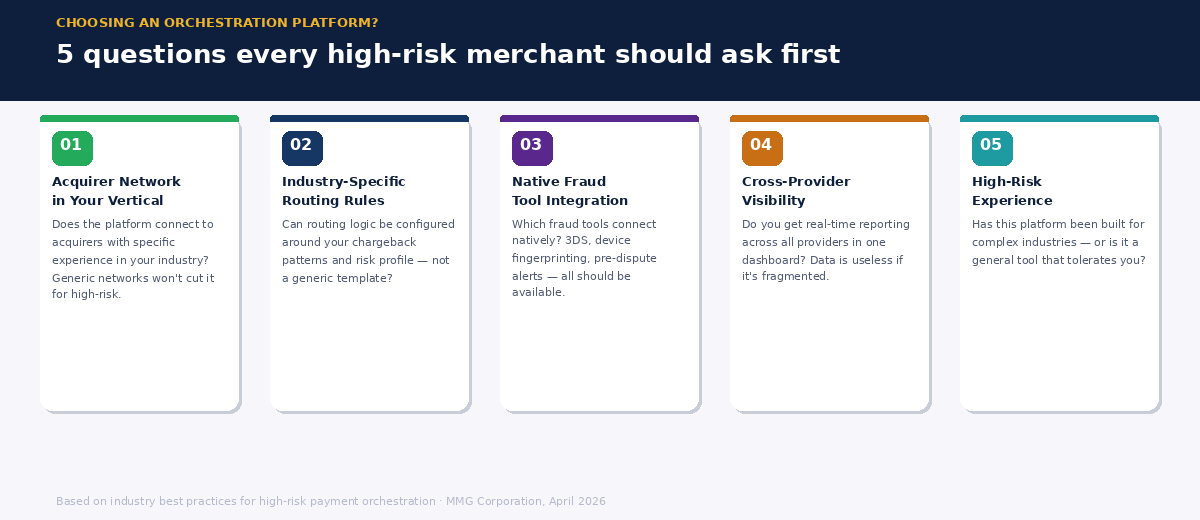

For high-risk merchants evaluating orchestration, the questions worth asking are: How many acquirers does the platform connect to in my specific vertical? Can routing rules be configured around my industry's specific chargeback patterns? What fraud tools integrate natively? And critically — does the platform give me visibility into performance across providers, so I can make data-driven decisions rather than guessing?

The answers to those questions will tell you whether a particular platform is built for your type of business — or whether it's a general-purpose tool that happens to be available to you.

At MMGCorporation, we work with high-risk merchants across Europe and beyond — providing the acquiring relationships that form the foundation of a well-orchestrated payment stack. Whether you're looking to build resilience into your existing setup, improve approval rates in specific markets, or simply reduce the risk of a single provider decision affecting your entire business, we're happy to talk through what a stronger processing infrastructure might look like for your operation.

MMGCorporation provides the specialist acquiring relationships that high-risk merchants need at the foundation of a strong orchestrated setup.

Let's talk about your industry, your volumes, and what stable, high-risk-friendly acquiring looks like for your business.