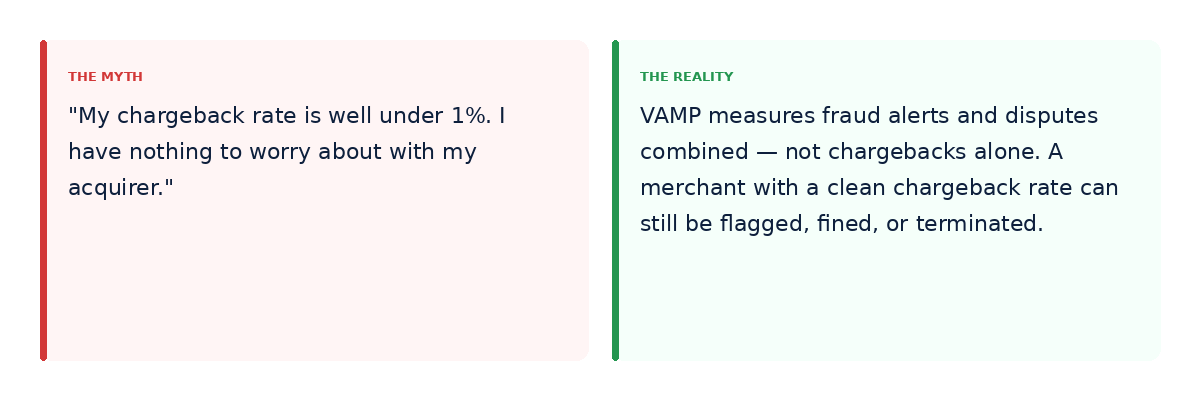

It sounds reasonable. Keep your chargebacks low and your acquirer is happy. That logic worked under the old monitoring framework. Under VAMP, it no longer does — and the merchants who haven't caught up yet are already taking the hit.

Where the Myth Comes From

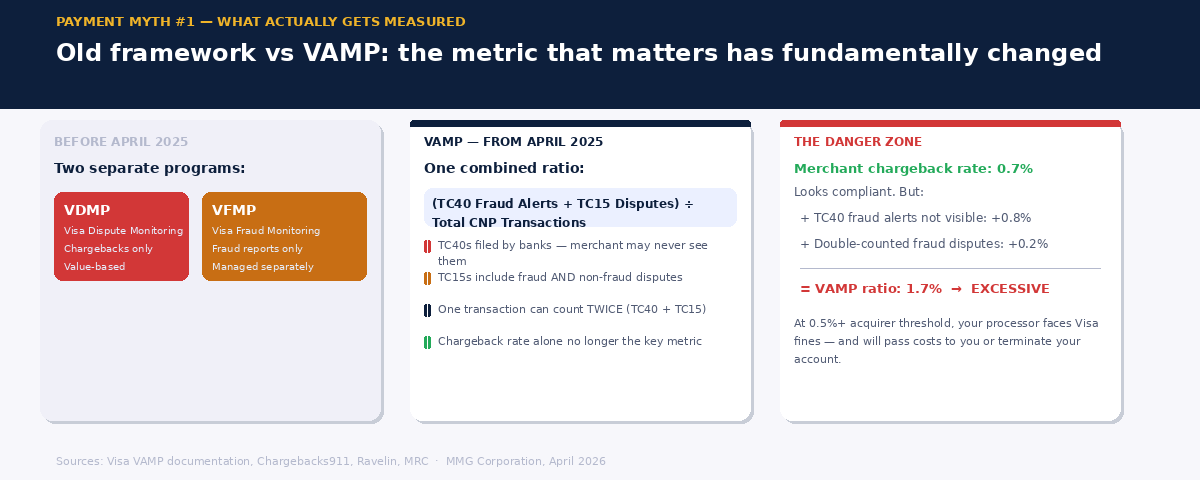

For years, Visa ran two separate monitoring programs: the Visa Dispute Monitoring Program (VDMP), which tracked chargeback ratios, and the Visa Fraud Monitoring Program (VFMP), which tracked fraud separately. Merchants learned to manage both independently, and the chargeback ratio became the primary metric most used to gauge their standing with acquirers. Keep it under 1% — ideally well under — and you were broadly considered compliant.

That framework was retired on 31 March 2025. On 1 April 2025, Visa launched VAMP — the Visa Acquirer Monitoring Program — replacing both programs with a single, combined metric. The chargeback rate as merchants have historically understood it is no longer the number that matters. And many merchants are still operating as though it is.

What VAMP Actually Measures

The VAMP ratio is calculated as follows:

VAMP RATIO FORMULA

(TC40 Fraud Reports + TC15 Disputes) ÷ Total CNP Settled Transactions

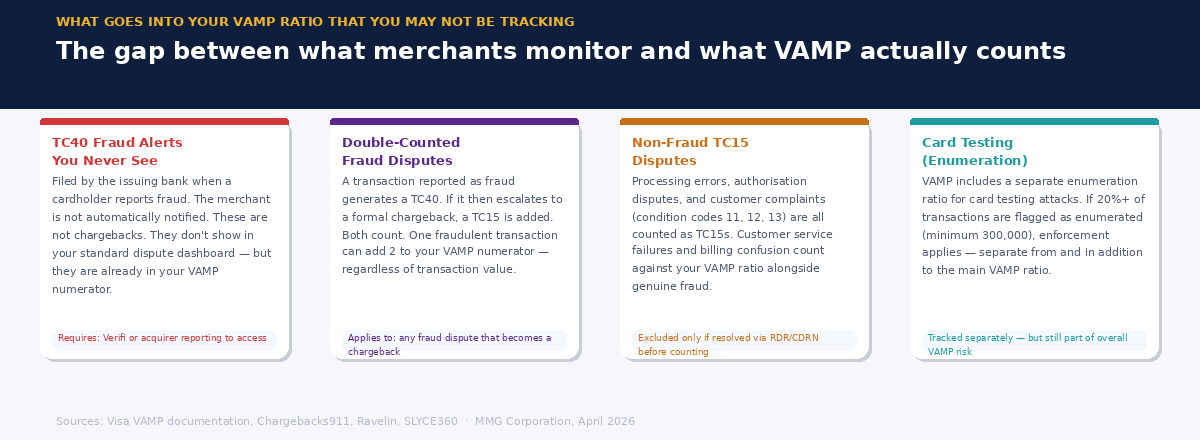

TC40s are fraud alerts filed by issuing banks when a cardholder reports a transaction as fraudulent. They are not chargebacks. They don't show up in the chargeback ratio a merchant monitors daily. Many merchants never see them at all — TC40 data is typically only accessible by requesting it directly from your acquirer or through Verifi.

TC15s are disputes — which include both fraud-related chargebacks and non-fraud disputes such as processing errors and customer complaints. These overlap with what merchants think of as chargebacks, but the coverage is broader.

VAMP adds both together and divides by total card-not-present settled transactions. The result is a single combined ratio that captures a much wider range of activity than the old chargeback-only metric. And here is the critical detail: a transaction can count twice. If a cardholder reports a payment as fraudulent, a TC40 is filed. If that same transaction then escalates to a formal dispute, a TC15 is generated. Both count in the numerator. One transaction, two strikes.

The Thresholds That Apply Now

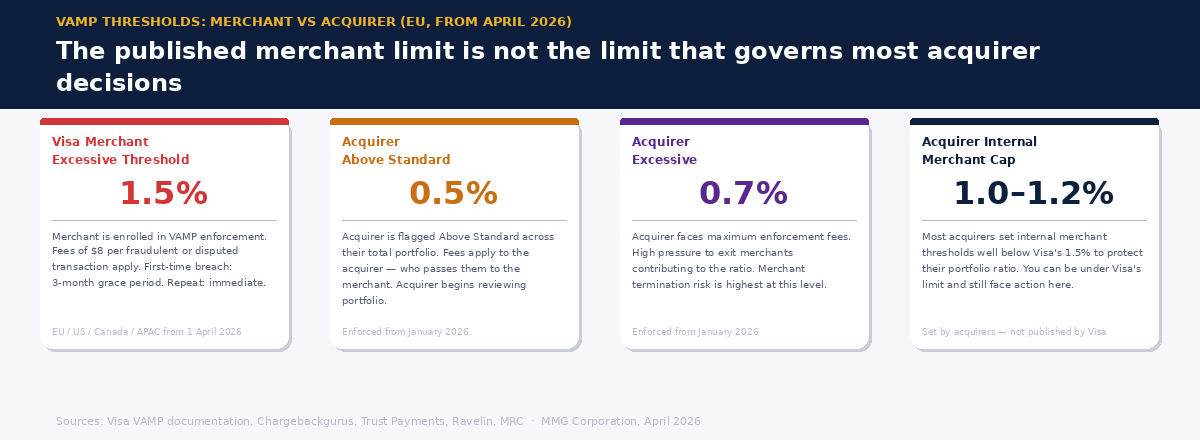

From 1 April 2026, the merchant Excessive threshold in the EU, US, Canada, and Asia-Pacific dropped from 2.2% to 1.5%. Merchants above this threshold with at least 1,500 combined TC40s and TC15s per month are enrolled in VAMP enforcement and face fees of $8 per fraudulent or disputed transaction. A 3-month grace period applies to first-time offenders, after which fees apply immediately.

But the threshold that most directly affects merchant behavior is not the 1.5% merchant limit — it is the acquirer threshold. Acquirers must keep their aggregate VAMP ratio across their entire merchant portfolio below 0.5% (Above Standard) and 0.7% (Excessive). To stay safely below those levels, most acquirers set internal merchant-level caps between 1.0% and 1.2% — well below Visa's official 1.5% merchant limit.

This means a merchant could be operating below Visa's published threshold and still face action from their acquirer, because the acquirer is managing the ratio across all their merchants combined. A single high-ratio merchant puts pressure on the entire portfolio.

Why High-Risk Merchants Are Particularly Exposed

TC40 fraud alerts are filed by issuing banks — not by merchants, and not by acquirers. A cardholder calls their bank, claims a transaction was fraudulent, and the bank files a TC40. The merchant may never know it happened. The charge may not become a chargeback. But the TC40 is already in the VAMP numerator.

For high-risk merchants operating in verticals where consumer disputes and friendly fraud are more common — iGaming, nutraceuticals, subscription services, adult entertainment — this creates a structural exposure that does not exist in the chargeback rate alone. A merchant who has worked hard to keep chargebacks under 0.5% may be sitting at 1.8% or above on the VAMP ratio, because TC40s they have never seen are accumulating in the background.

The situation is compounded by the fact that most merchants cannot access their TC40 data directly. Requesting it requires going to your acquirer or enrolling in a service like Verifi. Many merchants have been operating blind on this metric since VAMP launched in April 2025 — and enforcement has been live since October 2025.

What to Do About It

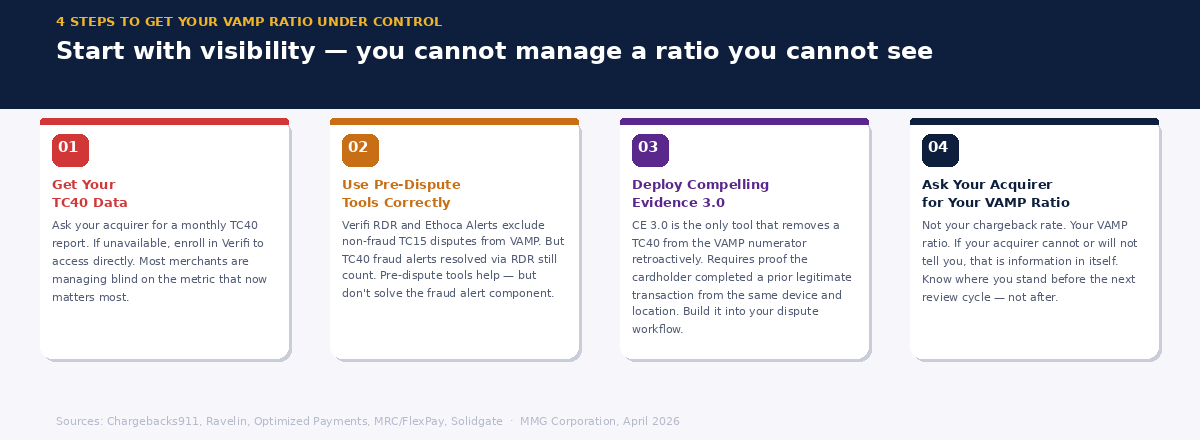

Get your TC40 data. Ask your acquirer for a monthly TC40 report. If they can't provide it, enroll in Verifi to access it directly. You cannot manage a ratio you cannot see, and many merchants are currently managing blind on the metric that now matters most.

Use pre-dispute tools — but understand their limits under VAMP. Verifi RDR and Ethoca Alerts resolve disputes before they become chargebacks. Under VAMP, non-fraud TC15 disputes resolved through these tools are excluded from the ratio. However, TC40 fraud alerts resolved through RDR are still counted. Pre-dispute tools help, but they are not a complete solution for the fraud alert component of VAMP.

Use Compelling Evidence 3.0. This is the only mechanism that can remove a TC40 from the VAMP numerator retroactively. When you can demonstrate that a cardholder who disputed a transaction has previously completed a legitimate, undisputed transaction from the same device and location, the TC40 can be excluded. It requires documentation and timely submission, but for merchants with significant TC40 exposure, it is worth building into the dispute response workflow.

Ask your acquirer where you actually stand. Not on chargebacks. On VAMP. These are different numbers. If your acquirer cannot or will not tell you your current VAMP ratio, that is information in itself — and worth taking seriously before the next review cycle.

The myth that a low chargeback rate equals safety is not a small misconception. Under the old framework it was accurate. Under VAMP it is genuinely dangerous — because it leads merchants to ignore the part of the ratio that is now doing the most damage, and which is the hardest to see.

The metric changed. The monitoring practices need to change with it.

MMGCorporation works with high-risk merchants who need an acquirer that understands how the compliance landscape is actually evolving. If you want to talk through your VAMP exposure or your processing setup more broadly, get in touch.