iDEAL, Debit, and the Card You Still Can't Leave Home Without: Paying in the Netherlands

The Dutch are among Europe's most cashless consumers. But behind the tap-to-pay culture lies a payment landscape that surprises many merchants — and still has a clear role for credit cards.

If Germany's payment story is about a domestic card that couldn't go international, the Netherlands tells a different story: a country that embraced digital payments earlier than almost anyone else in Europe, built one of the world's most successful online payment systems from scratch, and yet still has a distinct set of rules about when — and where — different payment methods actually work.

For merchants selling to Dutch consumers, understanding those rules is the difference between a checkout that feels native and one that quietly signals you don't really know your audience.

A Nation That Skipped Cash Early

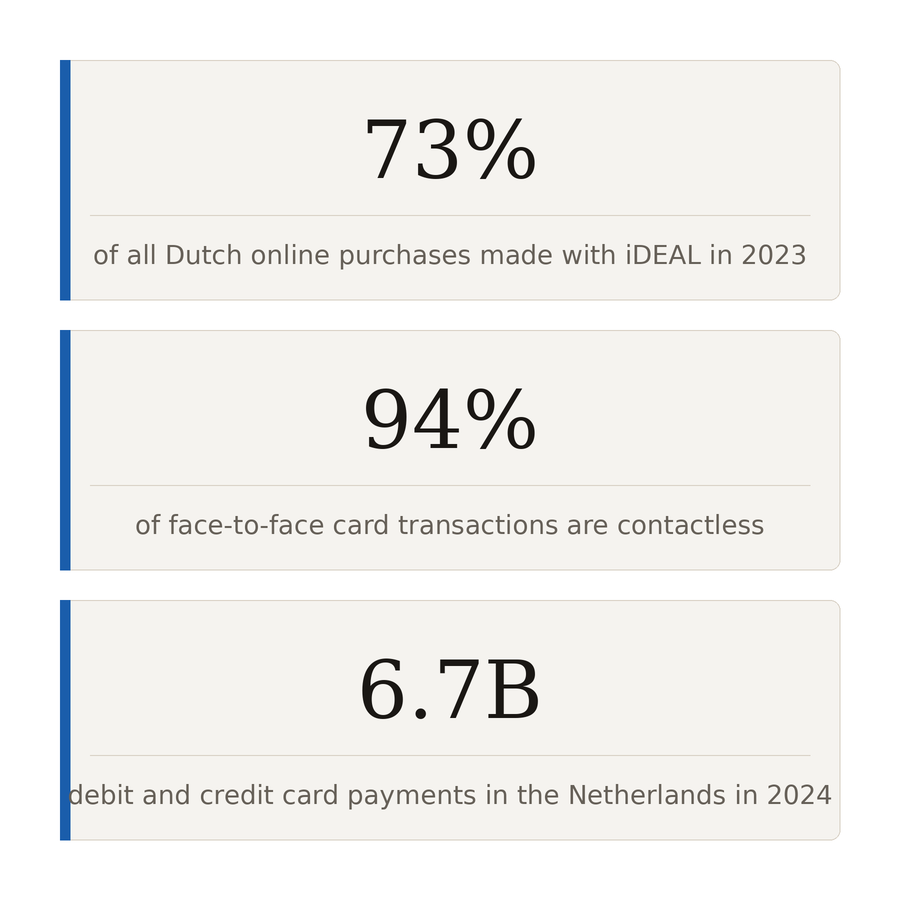

The Netherlands has long been one of Europe's least cash-dependent societies. Long before contactless payments became the norm elsewhere, Dutch consumers were paying by PIN at the supermarket, the market stall, and the corner café. Today, contactless card payments account for 94% of all face-to-face card transactions, and over 4 in 10 of those are made with a smartphone or smartwatch. The Dutch were not late adopters of digital payments. They were early ones.

But what they adopted — and how — is quite specific. The dominant instruments are debit cards and iDEAL, not credit cards. And that distinction matters enormously for how you structure your checkout.

iDEAL: The System That Became the Standard

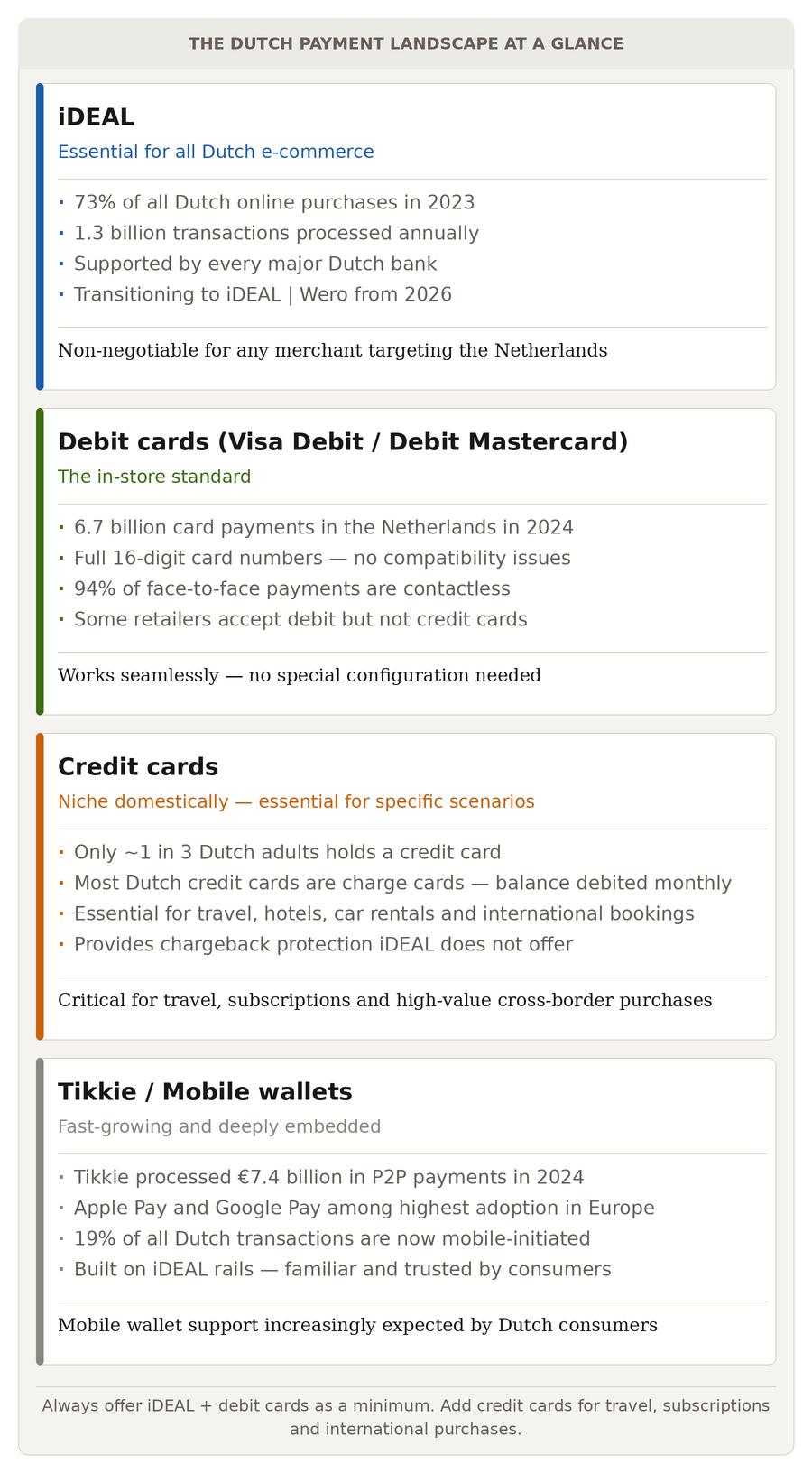

Launched in 2005 by a consortium of Dutch banks, iDEAL is an online bank transfer system that allows consumers to pay directly from their bank account without entering card details. When a Dutch consumer chooses iDEAL at checkout, they are redirected to their own bank's secure environment, authenticate via their banking app, and the payment is confirmed in real time.

It sounds simple — because it is. And that simplicity is why it won.

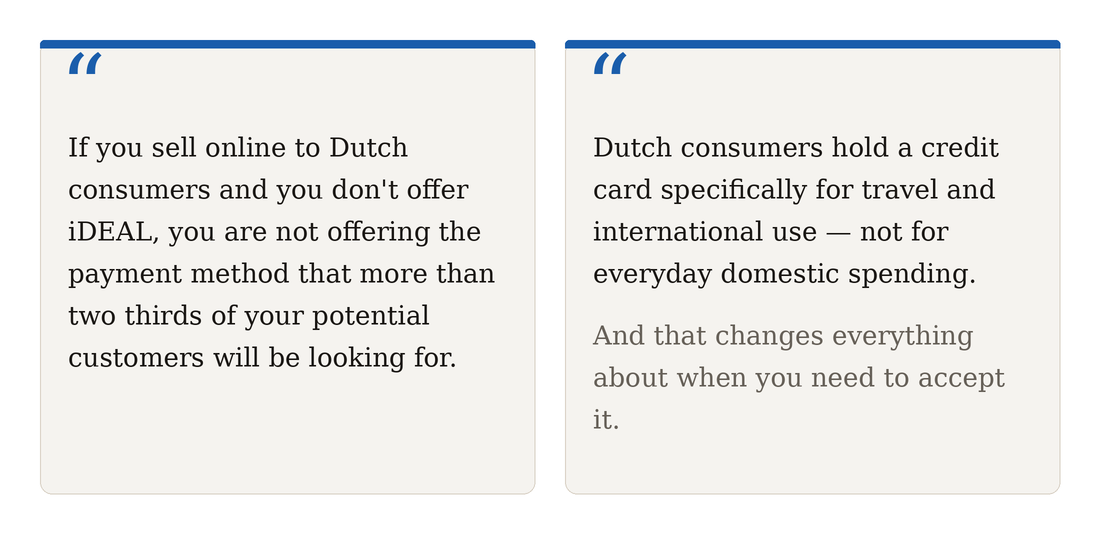

By 2023, iDEAL accounted for 73% of all Dutch online purchases, processing over 1.3 billion transactions annually. Every major Dutch bank supports it. Every significant Dutch e-commerce platform offers it. If you sell online to Dutch consumers and you don't offer iDEAL, you are not offering the payment method that more than two thirds of your potential customers will be looking for.

The numbers speak for themselves: during Black Friday Week 2024, iDEAL alone processed 56.82 million transactions — a 12% increase on the previous year.

The iDEAL of Tomorrow: Meet Wero

Here is where it gets interesting for merchants planning their payment stack. iDEAL is not standing still.

In October 2025, iDEAL announced it will begin rebranding to iDEAL | Wero in 2026, as part of a gradual transition to Wero — the European digital wallet backed by the European Payments Initiative (EPI). Already used by over 45 million Europeans, Wero aims to become a pan-European payment solution that works across borders, not just within the Netherlands.

For merchants, this means two things. First, iDEAL is not going away — it is evolving, and the transition will be gradual. Second, the Dutch payment infrastructure is moving towards broader European interoperability, which will eventually make it easier to offer a single wallet solution across multiple European markets. Watch this space.

Debit Cards: The Everyday Workhorse

At the physical point of sale, the Dutch pay primarily with debit cards. These are Visa Debit or Debit Mastercard products — full 16-digit card numbers, globally routable, and compatible with standard payment terminals worldwide. Unlike Germany's Girocard situation, Dutch debit cards have long carried proper international card numbers.

In 2024, Dutch consumers made 6.7 billion debit and credit card payments totalling €198 billion. The vast majority of these — around 6.4 billion — were in-store payments.

What surprises many international merchants is that debit card acceptance does not always mean credit card acceptance. A number of Dutch supermarkets — including some branches of major chains like Albert Heijn — accept debit cards but not credit cards. The economics are the same as in Germany: credit card interchange fees are higher, and Dutch merchants in domestic retail actively manage this cost.

Credit Cards: Niche at Home, Essential Abroad

Here is the part that catches most merchants off guard. Despite the Netherlands being one of Europe's most digitally advanced payment markets, only around one third of Dutch adults hold a credit card. By European standards, that is low.

The reason is cultural. Dutch financial culture is conservative when it comes to debt. The idea of spending money you don't yet have — even with a monthly payoff — sits uncomfortably with many Dutch consumers. Most Dutch "credit cards" are actually charge cards: the balance is debited in full at the end of the month, with no revolving credit option. True revolving credit cards are rare.

But this does not mean credit cards are unimportant. Far from it.

When Dutch consumers travel internationally, credit cards become essential. Dutch debit cards are not always accepted outside the Netherlands — particularly at hotels requiring a security deposit, car rental companies, and international subscription services. This is why many Dutch consumers hold a credit card specifically for travel and international use, not for everyday domestic spending.

For online subscriptions and streaming services, credit cards are often the default — particularly for international platforms like Netflix, Spotify, and Adobe, which don't always offer iDEAL as a payment option.

For higher-value purchases and cross-border shopping, credit cards offer consumer protection and chargeback rights that iDEAL — as a bank transfer — does not provide. Dutch consumers booking international hotels, flights, or high-value items from foreign merchants will often reach for a credit card precisely because they want that protection.

The practical implication for merchants: if you sell travel, software subscriptions, digital services, or high-value goods to Dutch consumers, credit card acceptance is not optional. It is the payment method your customer will use when iDEAL is not available or not appropriate.

What This Means If You're Selling to the Netherlands

iDEAL is non-negotiable for e-commerce. If you sell online and the Netherlands is a meaningful market, iDEAL must be in your checkout. Omitting it is the equivalent of not accepting cards. Fortunately, most major payment gateways support iDEAL as standard.

Debit cards work as expected. Dutch debit cards are standard Visa Debit or Debit Mastercard products and process without any special configuration. Unlike the German Girocard situation, there is no hidden compatibility issue here.

Credit cards matter more than the ownership stats suggest. The fact that only a third of Dutch adults hold a credit card does not mean credit card transactions are unimportant. It means the consumers who do use credit cards are doing so for specific, higher-value, or international scenarios — exactly the transactions you most want to capture. Declining a credit card payment from a Dutch consumer often means declining a booking, a subscription, or a high-value order.

Tikkie is worth knowing about. For peer-to-peer and small business payments, Tikkie — a payment request app built on iDEAL and run by ABN AMRO — is extraordinarily popular in the Netherlands. In 2024 it processed €7.4 billion across 157 million requests. While it is primarily a consumer-to-consumer tool, understanding it gives you context for how deeply embedded instant bank transfer culture is in the Netherlands.

Mobile wallets are accelerating. Apple Pay and Google Pay adoption in the Netherlands is among the highest in Europe. 19% of all Dutch transactions are now mobile-initiated. If your checkout doesn't support wallet payments, you are leaving a growing segment of the Dutch market underserved.

The Bigger Picture

The Netherlands is, in many ways, a glimpse of where European payments are heading. A cashless society built on instant bank transfers and debit cards, now accelerating towards mobile wallets and — with Wero — a potential pan-European payment layer that could eventually bridge the gap between iDEAL, Bancontact, Bizum, and other domestic systems.

For merchants, the lesson is straightforward: the Dutch payment mix is not complicated, but it is specific. iDEAL dominates online. Debit cards dominate in-store. Credit cards fill the gap for travel, international use, and consumer protection scenarios. Miss any one of these, and you miss a meaningful portion of what Dutch consumers need.

Get all three right, and the Netherlands rewards you with one of Europe's most digitally confident, high-spending consumer bases.

Ready to Optimise Your European Payment Stack?

At MMG, we help merchants and platforms navigate exactly this kind of local complexity — from payment method mix and routing logic to checkout optimisation by market. If the Netherlands is on your roadmap, we'd love to help.

Get in touch!