France is the largest e-commerce market in the EU. It also has a payment landscape unlike any other in Europe — shaped by a domestic card network that most international merchants don't fully understand, and a consumer base with very specific expectations at checkout.

When merchants expand into France, they typically assume that accepting Visa and Mastercard is enough. That assumption costs conversion. France has a domestic card payment infrastructure — Cartes Bancaires, universally known as CB — that dominates the market in a way that is genuinely unusual by European standards. Understanding what CB is, how it works, and why it matters for authorization rates is the starting point for any serious approach to the French market.

Beyond CB, the French checkout has its own distinctive shape: deferred debit is the norm rather than the exception, digital wallets are growing fast, BNPL has reached mainstream adoption, and a new European payment system is now live and expanding. Getting payment localization right in France is not a minor optimization — it is a meaningful driver of revenue.

Cartes Bancaires: The Network That Actually Runs French Card Payments

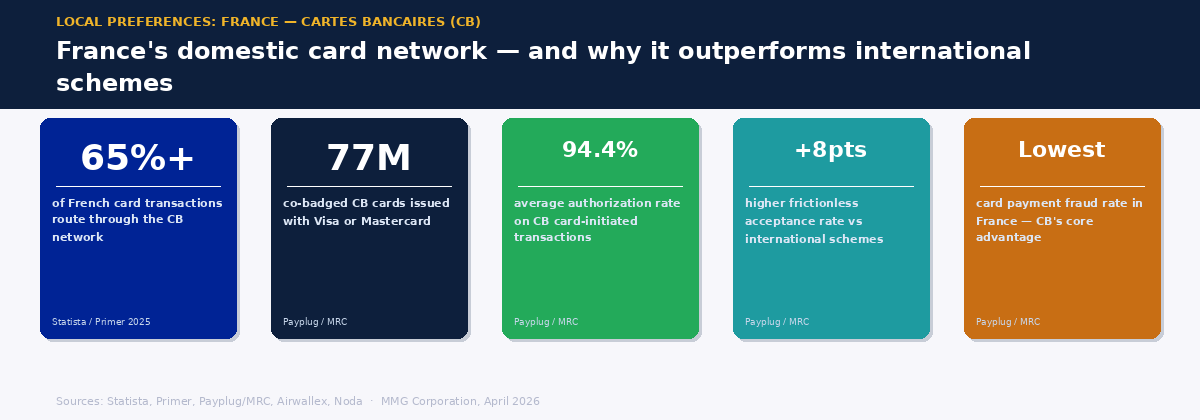

Founded in 1984, Cartes Bancaires (CB) is France's domestic card payment scheme, operated by GIE Cartes Bancaires — a non-profit grouping of French banks. Over two-thirds of all French card transactions route through the CB network. Most French debit and charge cards carry both the CB logo and a Visa or Mastercard co-badge, which means the card can transact domestically through CB and internationally through the global networks. The co-badge is standard; the CB routing is the default.

For merchants, this distinction matters practically. CB frictionless acceptance rates average around eight percentage points higher than those on international schemes for the same French cardholders. CB's authorization rate on card-initiated transactions is 94.4% on average — a figure that reflects its deep integration with French issuing banks and its highly optimized fraud detection, which achieves the lowest card payment fraud rate in France. When a French consumer pays with their CB-badged card and the transaction routes through the international scheme rather than CB, both the authorization rate and the potential for unnecessary 3DS friction increase.

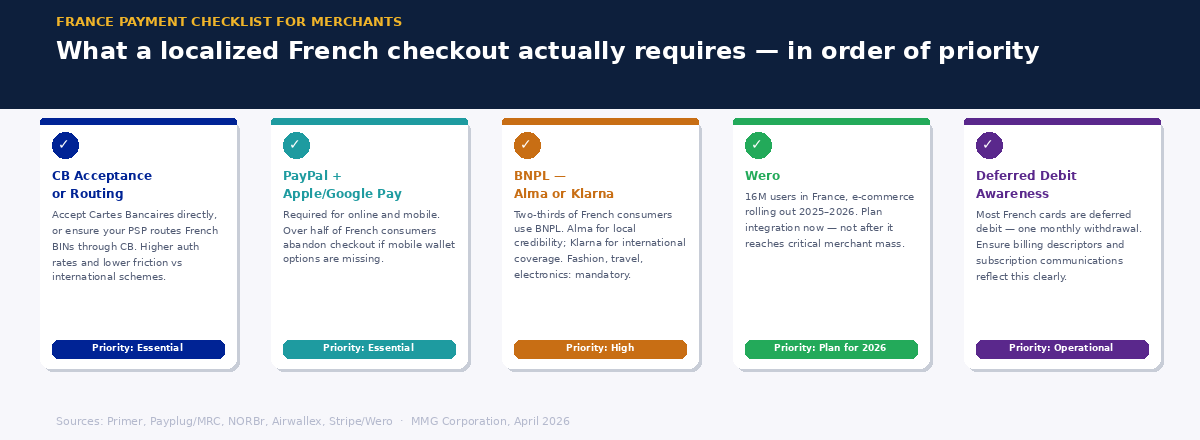

The practical implication for merchants is clear: accepting CB directly — or working with a payment service provider that routes French BINs through CB — delivers measurably better performance than treating French cards as generic Visa or Mastercard transactions. J.P. Morgan recognized this when it joined CB in March 2025, specifically to reduce cross-border interchange leakage and improve merchant acquiring performance in France.

How French Consumers Actually Use Their Cards

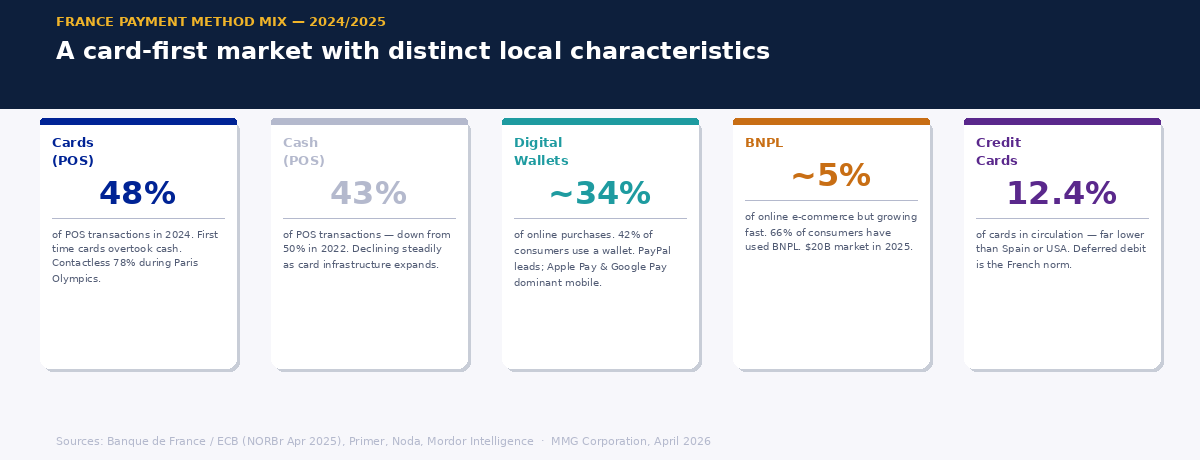

French card usage has some characteristics that differ meaningfully from neighboring markets. Credit cards are significantly less common than in many European countries — they represent just 12.4% of cards in circulation. The typical French cardholder uses a debit card, often a deferred debit card: one where all transactions made during the month are batched and debited from the account in a single withdrawal, usually at the end of the month. This is neither a credit card nor a standard immediate-debit card — it is a structure that is common enough in France to be the default expectation for many consumers, and unusual enough in the rest of Europe to catch international merchants off guard.

Cards overtook cash at French point-of-sale for the first time in 2024, with cards representing 48% of POS transactions against cash at 43% — a shift from 43% and 50% respectively just two years earlier. The June 2024 increase in the contactless payment limit accelerated this trend; during the Paris Olympics, contactless accounted for 78% of card transactions. The French consumer has decisively moved toward card-first payments in physical retail, and the infrastructure has followed.

Digital Wallets: PayPal, Apple Pay, and Wero

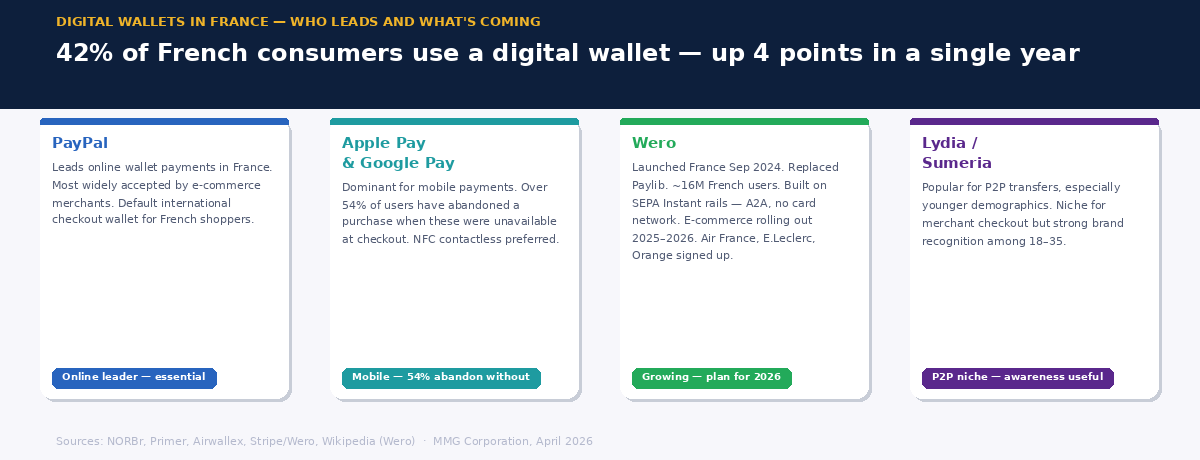

Digital wallets account for around a third of all online purchases in France, with 42% of French consumers using a digital wallet in 2025 — a figure that has grown four percentage points in a single year. PayPal leads international options for online shopping. Apple Pay and Google Pay dominate mobile wallet usage, and over 54% of users have abandoned an online purchase when these options were not available at checkout. The practical conclusion for merchants targeting French consumers online is that wallet support is no longer optional — it is a baseline expectation for the majority of the audience.

The most significant recent development in the French wallet landscape is Wero. Launched in France in September 2024 by the European Payments Initiative, Wero replaced Paylib — the previous bank-linked P2P wallet — and is now active across more than 20 French banks including BNP Paribas, Crédit Agricole, and Crédit Mutuel. Approximately 16 million users in France have active Wero accounts. The service is built on SEPA Instant Credit Transfer rails and settles in seconds, account-to-account, without routing through a card network.

Wero's e-commerce payment functionality is rolling out through 2025 and 2026, with major French merchants — including Air France, E.Leclerc, Orange, and Veepee — already signed up to accept it. Point-of-sale payments are planned for 2026. For merchants operating in France, Wero is now a payment method that will require active consideration over the next 12 to 24 months, particularly as its merchant acceptance base grows and its user base extends further into the mainstream.

BNPL: Mainstream, Not Emerging

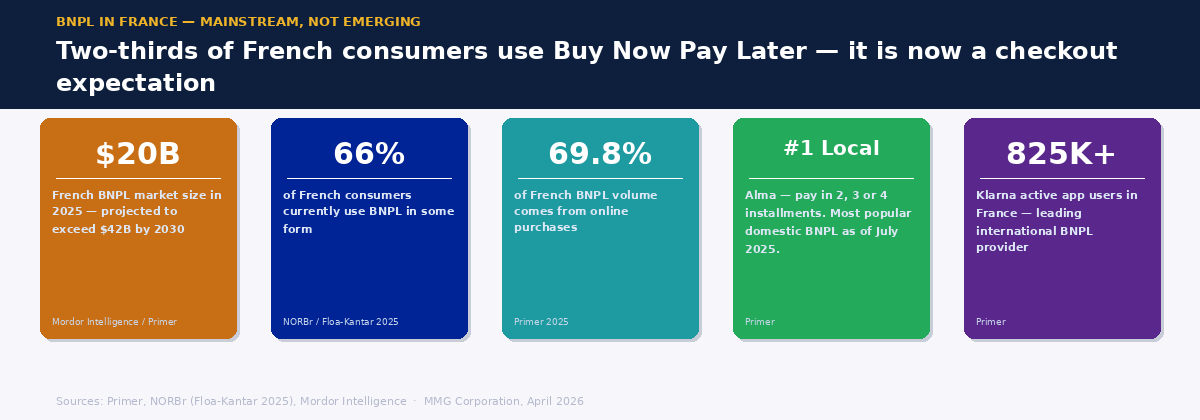

Buy Now, Pay Later has moved well beyond the emerging category in France. The French BNPL market was valued at approximately $20 billion in 2025 and is projected to more than double by 2030. Around 66% of French consumers currently use BNPL, with 69.8% of volume coming from online purchases. Over half of French BNPL users plan to maintain or increase their usage — making this a structural feature of French consumer payment behavior rather than a trend in transition.

The leading local provider is Alma, which as of mid-2025 is the most popular domestic BNPL option. Alma offers payment in 2, 3, or 4 installments, plus deferred payment options of 15 or 30 days. Klarna is the dominant international provider, with over 825,000 active app users in France. Floa, backed by BNP Paribas, is the third major player. For merchants in fashion, electronics, travel, and home goods — all categories where BNPL adoption is particularly high — not offering installment payment options is a direct conversion drag.

For high-risk merchants, BNPL introduces a compliance consideration worth noting: the ECB flagged in 2025 that BNPL products are contributing to increased consumer credit indebtedness across Europe, and regulatory tightening on BNPL disclosure and affordability requirements is expected as part of the broader consumer credit directive reform. Merchants offering BNPL — particularly in high-risk verticals — should monitor how these requirements evolve.

What This Means for Merchants Entering the French Market

France rewards payment localization more directly than most EU markets. The combination of a dominant domestic card scheme, a distinct card usage culture, high digital wallet penetration, and mainstream BNPL adoption means that a generic international payment stack will underperform against a localized one — often significantly.

The practical priorities for merchants entering or optimizing for France are straightforward. CB acceptance — or CB routing for French BINs — should be treated as a baseline requirement, not an optional local optimization. Wallet support for PayPal, Apple Pay, and Google Pay is a checkout necessity. Wero merits active monitoring and early integration planning given its trajectory. And for merchants in retail verticals where BNPL drives conversion, at least one French-recognized provider — Alma being the most important — should be part of the checkout offering.

France is also worth understanding for what it signals about European payment direction more broadly. The CB network's success in maintaining domestic market dominance while operating alongside global schemes, and the relatively rapid adoption of Wero as a Paylib replacement, both reflect a French consumer base that is comfortable with domestic alternatives when they work well. That is a pattern that may matter increasingly as Wero's merchant acceptance base grows and the EuroPA Alliance's cross-border ambitions become operational over the next two years.

MMGCorporation provides specialist acquiring for high-risk merchants across EU markets, including France. If you're looking to understand how France's payment landscape affects your processing setup — or how to structure your checkout for the French market — we're glad to help.