From EC-Karte to Visa Debit: Germany's Quiet Card Revolution

For decades, German shoppers paid with a card that was practically invisible to the outside world. Here's why that mattered — and why it's finally changing.

If you've ever tried to sell something online to German customers, you may have noticed something puzzling: a segment of your audience simply couldn't check out. Not because they didn't want to. Not because their card was declined. But because the card in their wallet — the one they use every single day at the supermarket, the bakery, and the petrol station — had no 16-digit number. No CVV. No way to plug into a standard payment form.

Welcome to Germany's payment paradox: a country of 84 million people, Europe's largest economy, and — until very recently — a debit card system that was essentially invisible to the global payments infrastructure.

That is changing. And if you're processing payments in Europe, you need to understand how, why, and what it means for you.

HISTORY:

The Card Germany Built for Itself

To understand where Germany is going, you need to understand where it came from. The story begins in the 1960s with the Eurocheque — a pan-European initiative to let travelers write cheques across borders. German banks eventually built their own electronic version of this, the EC-Karte (Electronic Cash card), which by the 1990s had become the standard way to pay at German tills.

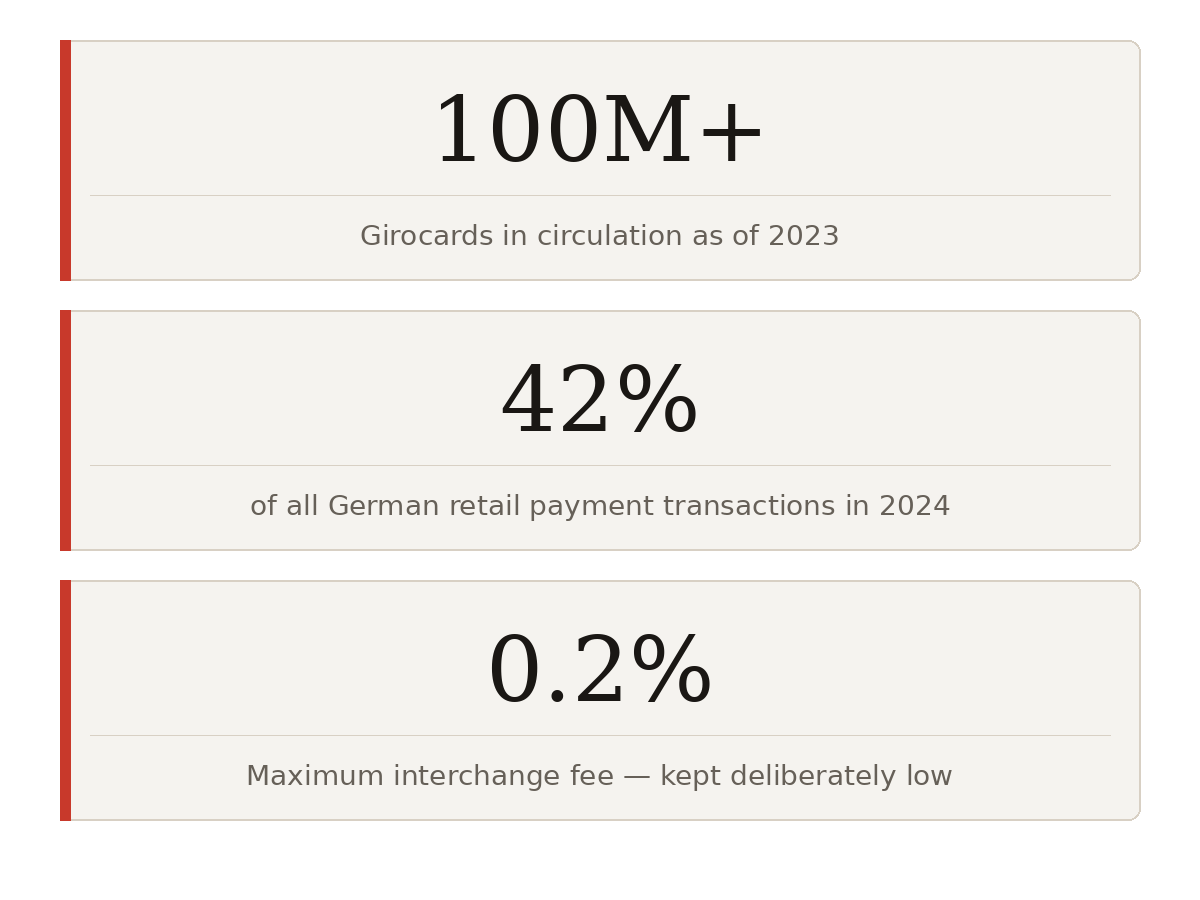

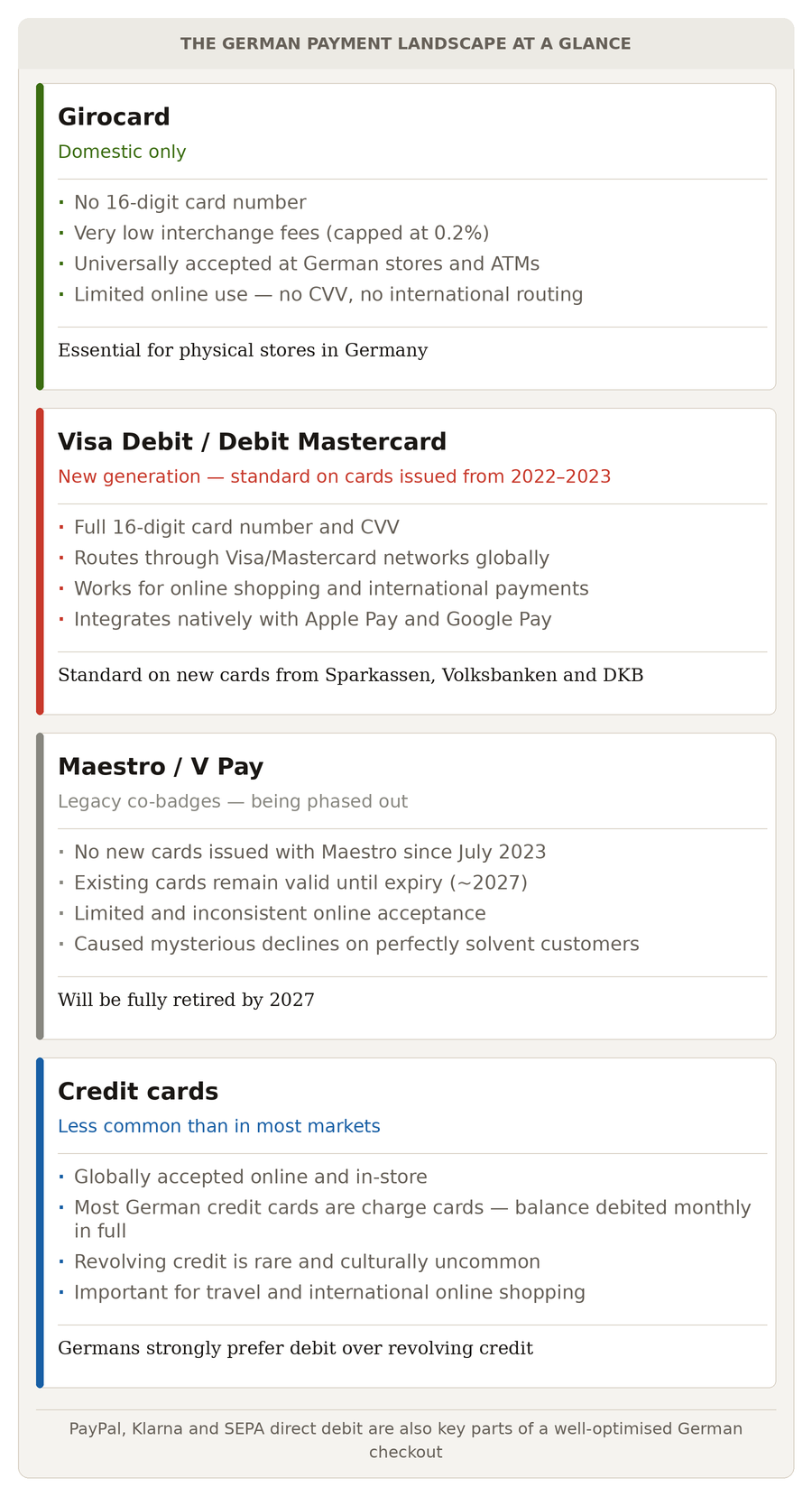

In 2007, this card was officially rebranded as the Girocard — though most Germans still call it the EC-Karte to this day, and probably always will. The rebrand changed the name; it didn't change the fundamentals. The Girocard routes transactions through a purely domestic German banking network. It has a chip, a PIN, and it works flawlessly at the 1.2 million payment terminals across Germany.

The key to the Girocard's dominance was its cost structure. Because it bypasses Visa and MasterCard entirely and routes through a domestic switch, the interchange fees are extraordinarily low — capped by regulation at just 0.2% of the transaction value. For small German merchants running on thin margins, the Girocard was genuinely the most affordable way to accept card payments. Credit cards, by contrast, were often actively avoided because they cost too much to accept.

The Problem Nobody Talked About

Here's the thing about a card that works beautifully in one country: it works beautifully in one country. That's it.

A standard Girocard carries no traditional 16-digit card number. It has no CVV security code. And because it routes through the domestic German banking switch rather than a Visa or MasterCard network, a merchant's payment gateway — whether based in Dublin, London, or Singapore — simply has no way to process it. The card is, from an international perspective, invisible.

For online commerce, this created a structural barrier. German consumers who wanted to shop at international websites had two options: use a credit card (which relatively few Germans had, and even fewer felt comfortable using for everyday spending), or rely on alternatives like PayPal or bank transfer. The card in their wallet — the card they trusted completely — couldn't help them.

A note on the co-badge workaround

For years, some Girocards carried a secondary network logo alongside the Girocard symbol — either Maestro from MasterCard, or V Pay from Visa. This helped with international ATM withdrawals and some cross-border in-store use. But Maestro and V Pay are not the same as a proper MasterCard Debit or Visa Debit. They had limited online acceptance, different processing requirements, and no standard card number usable everywhere. Many payment gateways couldn't handle them correctly, leading to mysterious decline rates on perfectly solvent customers. For merchants trying to understand why German conversion rates lagged, this was often the invisible culprit.

The Timeline of Change

The shift toward real, globally-routable debit cards in Germany didn't happen overnight. It unfolded in waves.

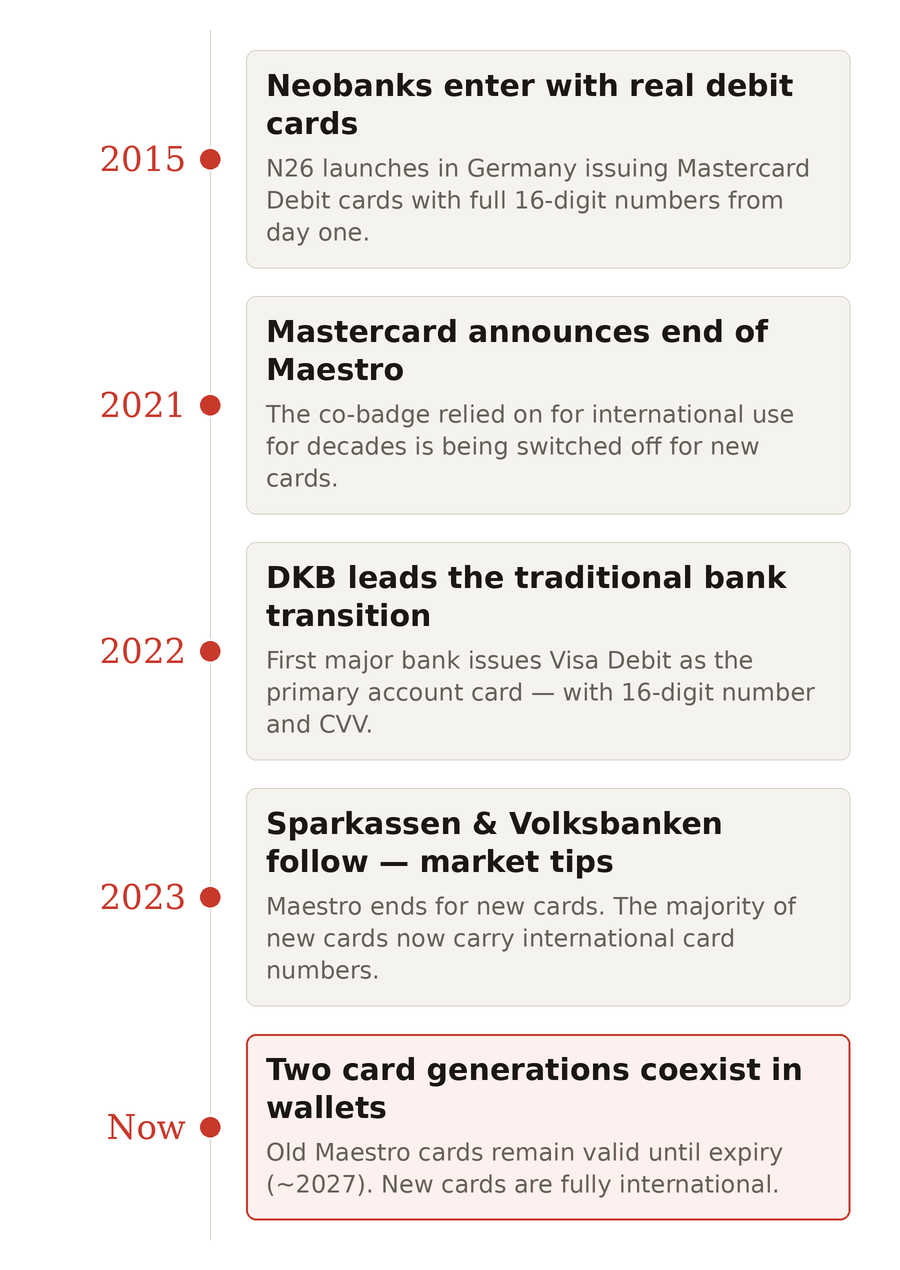

2015 — Neobanks enter with real debit cards N26 launches in Germany as Number26, issuing MasterCard Debit cards with full 16-digit numbers from day one. For the first time, German consumers can get a card that works like any MasterCard worldwide — directly linked to their bank account, no credit line needed. It's a niche fintech product at this stage, but the model is proven.

2021 — MasterCard announces the end of Maestro MasterCard announces it will phase out the Maestro network for new cards. This is the moment the tectonic plates start shifting for traditional German banks. The co-badge they had relied on for international compatibility for decades is being switched off.

2022 — DKB leads the traditional bank transition Deutsche Kreditbank (DKB) becomes the first major traditional German bank to issue a Visa Debit card as its primary account card — a single card with a proper 16-digit number and CVV. DKB is also the first German bank to process Visa Debit transactions through Visa's own Issuer Processing Service.

July 2023 — The cooperative banks follow, and the market tips Sparkassen — Germany's largest banking group by number of customers — switches all new card issuances to Debit MasterCard or Visa Debit. The Volksbanken Raiffeisenbanken announce the same. Maestro officially ends for new cards. This is the mainstream tipping point: the majority of new cards issued to German consumers now carry a proper international debit card number.

Now — Two card generations in wallets Germany has two coexisting generations of card. Older cards still valid until expiry carry Maestro or no co-badge at all. Newer cards carry Visa Debit or Debit MasterCard with full card numbers. This mixed landscape will persist until roughly 2027, when the last Maestro-co-badged cards expire.

What the New Cards Actually Change

It would be easy to underestimate how significant this shift is. From a consumer perspective, it might look like a minor logo change on the back of their card. From a payments perspective, it's a structural transformation.

Online checkout finally works natively A Visa Debit or Debit MasterCard issued by Sparkasse or DKB behaves — from your payment gateway's perspective — exactly like any other Visa or MasterCard debit card anywhere in the world. It has a 16-digit PAN, an expiry date, a CVV, and it routes through the standard international network. German customers with these new cards can now check out on any e-commerce site that accepts Visa or Mastercard, without needing PayPal as an intermediary.

3DS and SCA work as expected Under PSD2, Strong Customer Authentication applies to online card transactions in Europe. With real Visa/MasterCard Debit cards now in hand, German cardholders are entering the 3DS authentication flow for the first time en masse. Merchants should ensure their 3DS implementation handles German-issued debit cards cleanly — authentication friction that feels routine for a British or French consumer may feel unfamiliar to a German customer doing it for the first time.

Mobile wallets become genuinely useful Apple Pay and Google Pay support for the plain Girocard has always been patchy. The new Visa Debit and Debit MasterCard cards integrate natively into both wallets, unlocking contactless mobile payments for a consumer base that largely had to use physical cards. Germany's notoriously cash-heavy culture is already shifting — this accelerates it further.

The Girocard isn't going away One important nuance for merchants with physical stores in Germany: the Girocard system is not being retired. Some banks still offer it as an add-on, and many local merchants will continue to preferentially route domestic transactions through it because of the lower fees. For in-store payment setups in Germany, you still need Girocard acceptance alongside Visa and Mastercard.

What This Means If You're Selling to Germany

If Germany is — or could be — a meaningful market for you, there are several practical conclusions to draw.

German card conversion rates are improving. If you've historically seen Germany under perform versus comparable European markets in your checkout funnel, a meaningful portion of that gap is resolving itself as your German customers renew their bank cards. You don't need to do anything special — just make sure your gateway is properly configured to accept Visa Debit and Debit MasterCard, and watch the numbers improve over the next two to three years.

Alternative payment methods remain essential. PayPal, Klarna, and SEPA direct debit are deeply embedded in German consumer behavior — not just as workarounds for card limitations, but as genuine preferences. Germany's relationship with credit is culturally conservative: many consumers simply prefer knowing money leaves their account immediately. Offering local payment methods alongside card acceptance isn't a fallback — it's part of a well-calibrated German checkout.

The transition period matters for your data. Between now and 2027, you'll encounter a mix of old and new card generations from German customers. A decline from a customer with an old Maestro co-badge card is not the same signal as a decline from a newly issued international card. Understanding your German payment data at this level of granularity can surface optimization opportunities that aggregate metrics will hide.

The Bigger Picture

Germany's payment card evolution is a good reminder that payment preferences aren't just about technology — they're shaped by history, culture, regulation, and trust. The Girocard wasn't a failure of innovation. It was a deliberate, well-functioning system built to serve specific needs: low fees, instant settlement, domestic trust. It did exactly what it was designed to do, for decades, at enormous scale.

What's changing isn't that Germany is finally "catching up." It's that the boundaries between domestic and international commerce have dissolved, and a card designed purely for one country can no longer serve the full range of how people want to buy and sell. The new Visa Debit and Debit MasterCard cards don't replace the Girocard — they extend the German consumer's reach beyond it.

For anyone working in payments, understanding this kind of local nuance is the difference between a checkout that converts and one that quietly loses customers you never knew you had.

Ready to Optimist Your European Payment Stack?

At MMG, navigating exactly this kind of local complexity is what we do. From routing logic and decline analysis to checkout optimization by market, we help merchants and platforms get the most out of every European market — including Germany.

If you'd like to talk through your payment setup, we'd love to hear from you.