— and It's Moving Faster Than Most Merchants Realize

Two-thirds of EU card payments run on American networks. Europe has decided that is a strategic problem — and the infrastructure to address it is now live, funded, and growing faster than the policy discussions that preceded it.

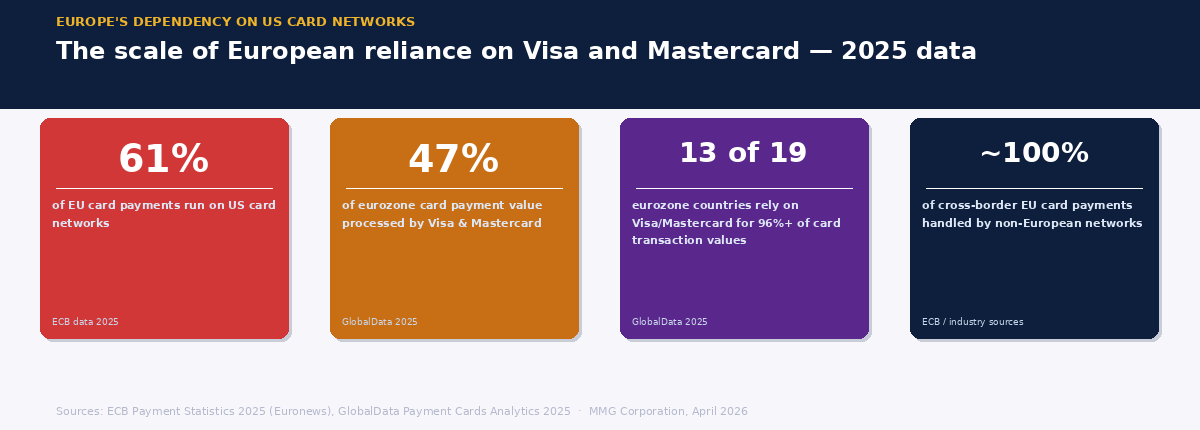

The numbers are striking when laid out plainly. According to ECB data for 2025, Visa and Mastercard account for 61% of card payments across the EU. In the eurozone specifically, the two US networks processed 47% of total card payment value in 2025 — and in 13 out of 19 eurozone countries, their combined share of card transaction values exceeds 96%. For everyday cross-border card payments, the dependency is even more pronounced: the American networks handle nearly all of it.

European policymakers have been uncomfortable with this concentration for years. What changed in 2025 and early 2026 is that the discomfort became urgency — and the urgency produced action. Europe now has live payment infrastructure, real user adoption, and a coordinated institutional push that goes well beyond previous attempts. For merchants operating across EU markets, understanding what is being built — and what timeline it is on — is increasingly relevant.

Why Now

The strategic case for European payment sovereignty is not new. The EU's own Instant Payments Regulation, the European Central Bank's retail payments strategy, and years of policy discussion all predate the current moment. What shifted was the broader geopolitical environment. As the EU-US relationship became more complicated across trade, technology, and economic policy, the question of who controls Europe's payment infrastructure moved from a technical discussion to a political one.

The ECB put the concern on the record in February 2026, warning formally of "strong reliance" on international card schemes and describing it as a form of "overdependence" that creates data protection, resilience, and market power risks. ECB President Christine Lagarde framed it as a sovereignty question: "If we lose control of our money, we lose control of our economic destiny." The concern is structural — not about any specific event, but about the exposure created by having critical payment infrastructure owned and governed outside the EU.

Wero: From Pilot to Scale

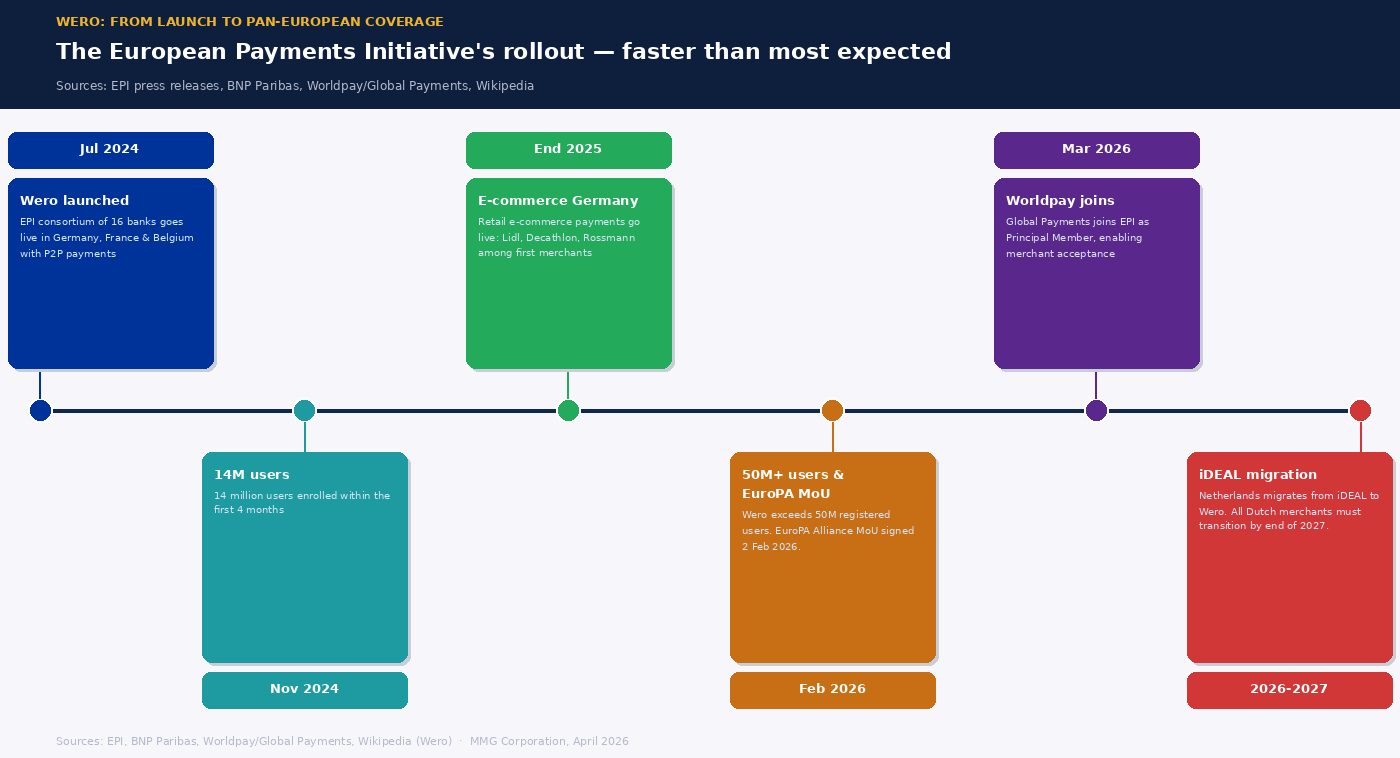

The most tangible expression of Europe's payment sovereignty push is Wero, launched in July 2024 by the European Payments Initiative — a consortium of 16 European banks and payment service providers including BNP Paribas, Deutsche Bank, and Worldline. Wero is built on SEPA Instant Credit Transfer rails: account-to-account payments that settle in real time, without routing through the card networks that currently dominate European commerce.

The growth trajectory has been faster than most observers expected. By February 2026, Wero had exceeded 50 million registered users across Belgium, France, and Germany, having processed more than €7.5 billion in transfers. In its first phase, the service focused on peer-to-peer payments — the consumer habit that builds the user base needed to make merchant acceptance viable. That phase has been broadly successful.

The more commercially significant phase is now underway. E-commerce payments went live in Germany at the end of 2025, with merchants including Lidl, Decathlon, and Rossmann among the first to accept Wero online. France and Belgium are rolling out e-commerce acceptance through 2026. In France, Air France, E.Leclerc, Orange, Veepee, and Dott have signed agreements to accept Wero payments. The French government's General Directorate of Public Finances has also announced interest in integrating Wero as a payment method for public services — a signal of institutional confidence that extends beyond the private sector.

Point-of-sale payments — allowing consumers to tap or scan at physical checkouts — are rolling out through 2026 and 2027. The Netherlands is undergoing a full migration from iDEAL, the country's dominant online payment system, to Wero: the transition begins in 2026 and is expected to be complete by the end of 2027. That means every Dutch merchant currently accepting iDEAL will need to transition, delivering an entire national payment market to the European system by default.

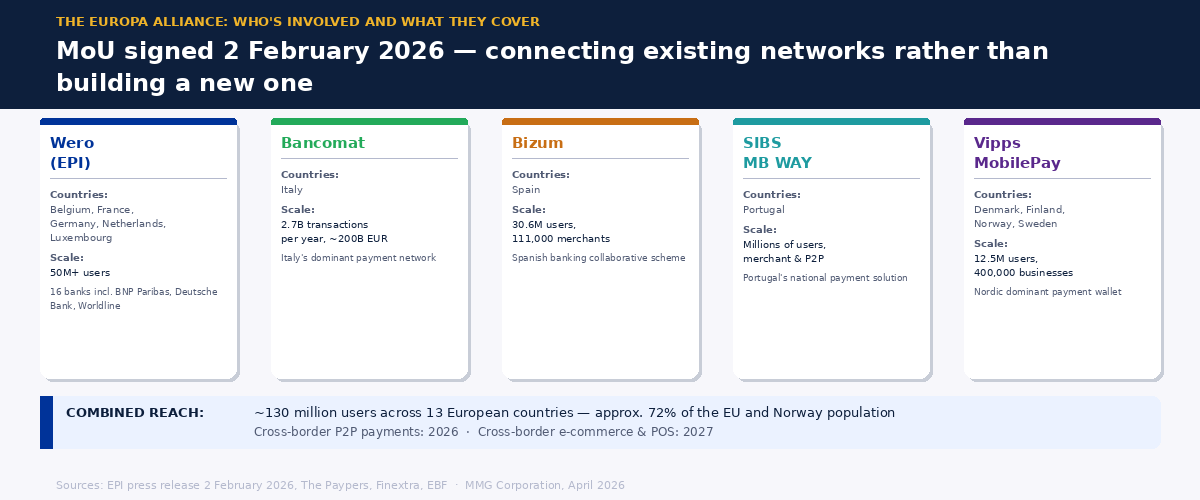

The EuroPA Alliance: Connecting What Already Exists

The most strategically significant development of early 2026 was not Wero's user growth — it was the agreement signed on 2 February 2026 between EPI and the EuroPA Alliance. The EuroPA Alliance brings together Italy's Bancomat, Spain's Bizum, Portugal's SIBS-MB WAY, and the Nordics' Vipps MobilePay. These are not new or experimental systems. They are established national payment networks with tens of millions of active users each — Bizum alone has over 30 million users and 111,000 merchants in Spain.

The Memorandum of Understanding commits the partners to building a central interoperability hub that connects these existing networks into a coherent pan-European system. Rather than replacing domestic payment brands that consumers already trust, the model connects them underneath — so a consumer in France can pay a merchant in Italy using their existing app, and the transaction settles without touching a card network.

The combined reach of the participating systems is approximately 130 million users across 13 European countries — representing roughly 72% of the EU and Norway's population. Cross-border peer-to-peer payments are targeted for 2026. Cross-border e-commerce and point-of-sale payments are targeted for 2027. A proof of concept demonstrating cross-border QR payment interoperability between Bancomat, EPI, and SIBS-MB WAY was successfully completed in April 2026 — less than three months after the MoU was signed.

Wero's institutional base has also continued to grow. Revolut joined the EPI in June 2025. N26 signed in December 2025. Worldpay, now part of Global Payments, joined as a Principal Member in March 2026, enabling its merchant clients across Europe to begin accepting Wero payments.

The Digital Euro: Slower, but Advancing

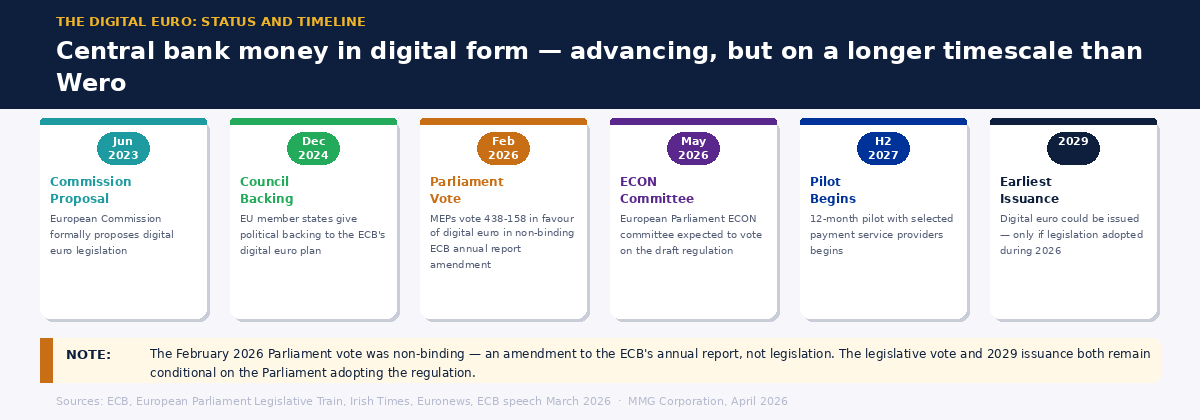

Running in parallel — at a longer timescale and with more political complexity — is the digital euro project. The digital euro is a different kind of instrument: central bank money in digital form, issued by the ECB, designed to sit alongside cash and commercial bank payment services rather than replace them.

On 10 February 2026, the European Parliament voted 438 to 158 in favour of an amendment to its annual report on the ECB expressing support for the digital euro — including both online and offline functionality. This was a non-binding political signal, not legislation, but it demonstrated where parliamentary sentiment sits and put further pressure on the formal legislative process to advance.

The ECB's own position is clear: if the legislation is adopted during 2026, the digital euro could be issued in 2029. A pilot involving selected payment service providers is planned to begin in the second half of 2027. The ECON committee of the European Parliament is expected to vote on the draft regulation in May 2026. Under the proposal, merchants would be legally required to accept the digital euro, and the ECB has committed that it would not have access to personal transaction data.

The political arithmetic in the Parliament remains uncertain — support is concentrated among centre-left and liberal groups, without a standalone majority, and the centre-right is divided. The digital euro is a 2029 story at the earliest, and only if the legislation clears. But the direction is set, and the technical preparation work is ongoing regardless of the legislative timeline.

What This Means for Merchants

The honest answer is: not much in the next twelve months, but more than most payment professionals currently factor into their planning over the next three to five years.

Visa and Mastercard are not going anywhere. Their infrastructure is too embedded, their acceptance too universal, and their reliability too proven for any realistic timeline to displace them from the EU market. The European systems being built are designed to offer an alternative — not to force a replacement. For most merchants, adding Wero acceptance where it is commercially available is an incremental decision, not a structural one.

What is changing is the direction of travel. The fact that 50 million users are already enrolled in Wero — before e-commerce functionality was widely available — shows that the consumer base can be built. The EuroPA MoU means that cross-border coverage, which has historically been the fatal weakness of European payment alternatives, is now being addressed through interoperability rather than a single centralised system. And the iDEAL migration in the Netherlands means that by 2027, there will be at least one major EU market where Wero is the default online payment method rather than an option.

For high-risk merchants in particular, the emergence of robust A2A payment infrastructure is worth tracking carefully. Account-to-account payments operate outside the card network rules that define chargeback ratios, VAMP thresholds, and the MCC-based classification systems that determine acquiring terms. They do not eliminate payment risk, but they change its shape — and for some merchant categories, that shift could be commercially significant.

Europe's push for payment sovereignty is not a policy aspiration anymore. It is infrastructure — live, funded, and expanding. Whether it reaches the scale needed to meaningfully shift the competitive landscape remains to be seen. But the trajectory in 2025 and early 2026 has been more concrete, more coordinated, and more commercially grounded than anything that preceded it. Merchants paying attention to the EU payment landscape should be tracking it.

MMGCorporation provides specialist acquiring for high-risk merchants across EU markets. If you want to talk through how shifts in the European payment landscape affect your processing setup, we're here for that conversation.