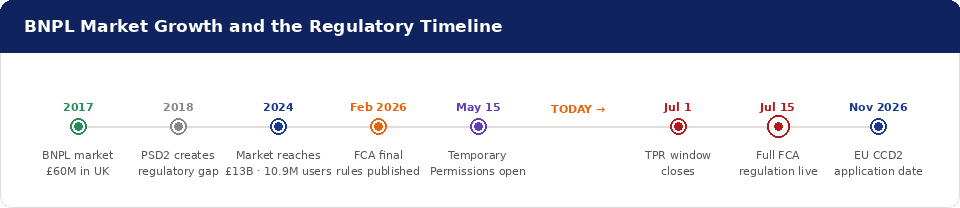

BNPL Is Getting Regulated

On July 15, 2026, Buy Now Pay Later becomes regulated consumer credit in the UK for the first time — after nearly a decade of operating in a deliberate regulatory gap. The FCA's framework is the most developed BNPL rulebook in Europe, and what it requires of lenders and merchants is already shaping how the rest of the continent thinks about what comes next.

How BNPL Got Here

Buy Now Pay Later grew by exploiting a structural gap in UK consumer credit law. The second Payment Services Directive, which came into force in 2018, focused on payment services rather than credit provision — and BNPL providers positioned their products on the credit side of that boundary, offering interest-free deferred payment without the affordability assessments or formal consumer protections required for other forms of lending.

The result was a market that scaled extremely fast. BNPL grew from £60 million in 2017 to over £13 billion in lending by 2024. According to the FCA's 2024 Financial Lives Survey, 20% of UK adults — approximately 10.9 million people — used BNPL in the 12 months to May 2024. For merchants, BNPL became a standard checkout feature: it increased basket size, improved conversion, and gave consumers a frictionless way to manage cash flow at the point of purchase. It also came with essentially no regulatory overhead.

That changes on July 15.

What the FCA Framework Actually Requires

The FCA's final rules, published on February 11, 2026, formally reclassify third-party BNPL products as Deferred Payment Credit (DPC) — a regulated consumer credit product sitting under full FCA oversight. Lenders entered a Temporary Permissions Regime on May 15, 2026, with full regulation taking effect on July 15. The notification window for the TPR closed on July 1, leaving a tight compliance window for any provider that had not already begun preparations.

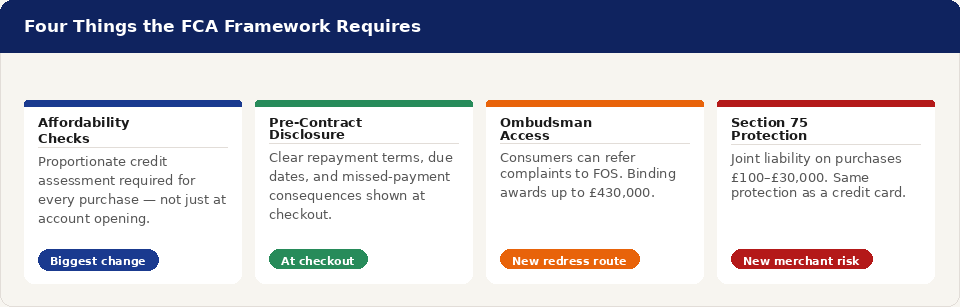

The framework places four principal obligations on BNPL lenders:

Affordability checks. Lenders must conduct proportionate creditworthiness and affordability assessments before offering DPC for every purchase — not just at account opening. This is the most significant operational change: a product that previously offered frictionless checkout now requires a credit evaluation at the point of sale.

Pre-contract disclosure. Providers must display clear, upfront information about repayment terms, due dates, amounts, and the consequences of missed payments — at checkout, before the consumer confirms the purchase. The FCA's Consumer Duty framework requires this information to be genuinely useful, not buried in terms and conditions.

Financial Ombudsman access. For BNPL agreements made on or after July 15, consumers have access to the Financial Ombudsman Service for the first time. FOS determinations are binding up to £430,000. This creates a formal complaints and redress infrastructure where none previously existed.

Section 75 protection. BNPL purchases between £100 and £30,000 from July 15 onward will carry Section 75 Consumer Credit Act protection — giving shoppers the same joint liability rights as standard credit cards. For merchants, this is material: it creates a legal pathway for consumer claims that did not previously exist for BNPL transactions.

What This Means for Merchants — Even Those Outside the UK

The FCA regulated perimeter sits around BNPL lenders, not merchants. UK merchants who offer third-party BNPL at checkout do not themselves need FCA authorization for credit broking. But "not authorized" does not mean "unaffected."

The most immediate merchant risk is checkout disruption. If a BNPL provider has not secured FCA authorization or temporary permission by July 15, the merchant may need to remove that payment option from their checkout immediately. Any provider operating without authorization after the deadline is doing so illegally. Merchants should already know whether their BNPL provider is authorized — and if they don't, finding out now is more urgent than it sounds.

The second area of exposure is financial promotions. Merchants who promote BNPL in their own marketing — on product pages, in email campaigns, in social advertising — may be running financial promotions that, under the incoming rules, need to be approved or provided by an authorized firm. Everyday retail copy describing BNPL as "spread the cost" or "buy now, pay later" can qualify. Content of this kind must be clear, fair, and not misleading — and responsibility for getting that right sits with the merchant, not just the lender.

Third, merchants will need to update their customer journeys. The new framework requires mandatory pre-contract disclosures to be displayed at checkout — information that lenders must flow down to merchants to surface in their own UX. Product pages, app flows, and in-store payment journeys may all require changes to comply with the lender's new obligations.

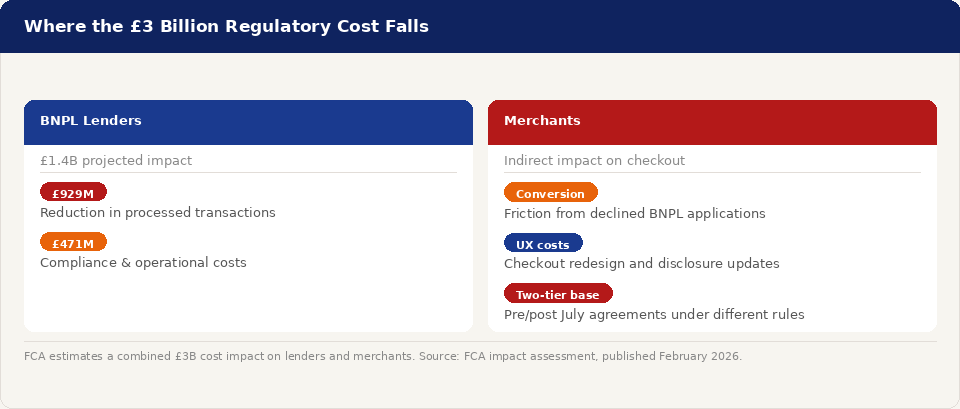

The FCA estimates that the regulatory overhaul will cost merchants and lenders a combined £3 billion. BNPL lenders are projected to absorb £1.4 billion of that, driven primarily by a £929 million reduction in total processed transactions as affordability checks decline some applications. The remaining impact falls on the merchant side — through conversion friction, checkout redesign costs, and the operational overhead of managing a two-tier customer base where pre-July agreements remain unregulated and post-July agreements are fully regulated.

What EU Merchants Should Be Watching

The FCA framework applies specifically to the UK. EU merchants operating under existing payment services regulation are not subject to the July 15 deadline — but the UK regulatory design is not happening in isolation.

The EU has been developing its own approach to BNPL regulation under the revised Consumer Credit Directive (CCD2), which entered into force in November 2023 and requires transposition into national law by member states by November 2025, with full application from November 2026. CCD2 brings most BNPL products into scope for the first time, requiring credit assessments and clear pre-contractual information across EU markets — the same structural approach the FCA has implemented, on a similar timeline.

The practical implication for EU merchants is straightforward: the compliance changes that UK merchants are navigating right now — updated checkout flows, revised financial promotion standards, affordability check friction, potential provider consolidation — are a preview of what EU merchants will be managing by the end of 2026. Markets like Germany, the Netherlands, and France, where BNPL adoption has grown rapidly, are likely to see significant changes to how BNPL products are presented and offered at checkout as CCD2 implementation reaches its final stage.

Merchants in high-risk categories who rely on BNPL as a conversion tool — particularly in travel, nutraceuticals, and subscription-based businesses where BNPL has helped manage high-ticket or recurring payment friction — should be tracking both the UK implementation and their own national CCD2 transposition dates. The window between now and November 2026 is not long.

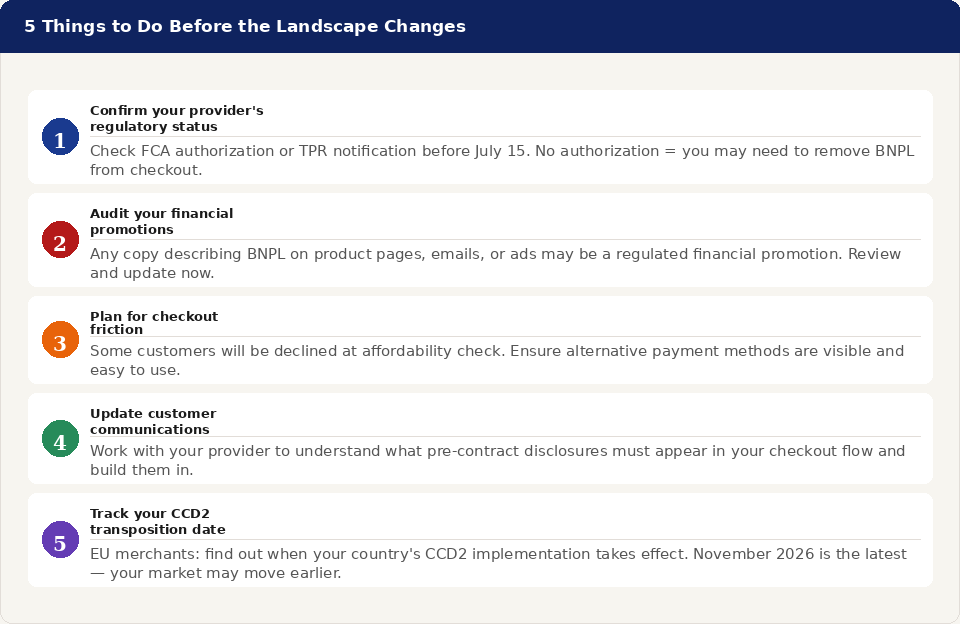

5 Things to Do Before the Landscape Changes

1. Confirm your BNPL provider's regulatory status. If you operate in the UK, verify immediately whether your provider has secured FCA authorization or TPR notification before July 15. If they have not, you may need to remove BNPL from your checkout on that date. If you operate in the EU, find out whether your provider is preparing for CCD2 and what their implementation timeline looks like.

2. Audit your financial promotions. Review all marketing copy that references BNPL — product pages, email campaigns, social ads, in-store signage. Under the new UK rules, this content must be clear, fair, and not misleading. In the EU, CCD2 imposes similar requirements on promotional material. If your copy was written before these frameworks were designed, it likely needs updating.

3. Plan for checkout friction. Affordability checks will decline some customers who would previously have been approved instantly. Plan for this: make sure alternative payment methods are visible and easy to use for customers who do not pass the check. A declined BNPL application that leads to checkout abandonment is a conversion loss that could have been a sale via card or bank transfer.

4. Update your customer communications. Your lender will flow down mandatory pre-contract disclosure requirements — you will need to surface this information in your own checkout flow. Work with your provider now to understand exactly what needs to change, and build the UX updates into your roadmap before the deadline, not after.

5. Track your national CCD2 transposition date. If you operate in EU markets, find out when your country's national transposition of CCD2 takes effect. Several member states have already transposed. Others are still in progress. The November 2026 application date is the latest point — your market may move earlier.

The Bottom Line

BNPL's decade-long regulatory exemption is ending — first in the UK on July 15, and progressively across EU markets through the CCD2 implementation cycle. The changes are not fatal to the product. Klarna and Clearpay have both publicly welcomed regulation, and consumer trust in BNPL is expected to improve as the sector demonstrates compliance. But the frictionless checkout experience that drove BNPL adoption is changing, and merchants who rely on it as a conversion tool need to plan for a different operating environment.

The merchants best positioned for this shift are the ones who understand it clearly, prepare their checkout flows in advance, and have diverse enough payment options that any one method's regulatory friction doesn't determine their conversion rate.

At MMG, we work with merchants across EU markets on payment infrastructure and payment method strategy. If you want to talk through how BNPL regulation affects your checkout mix, or what alternative payment methods should sit alongside it, we're glad to help.